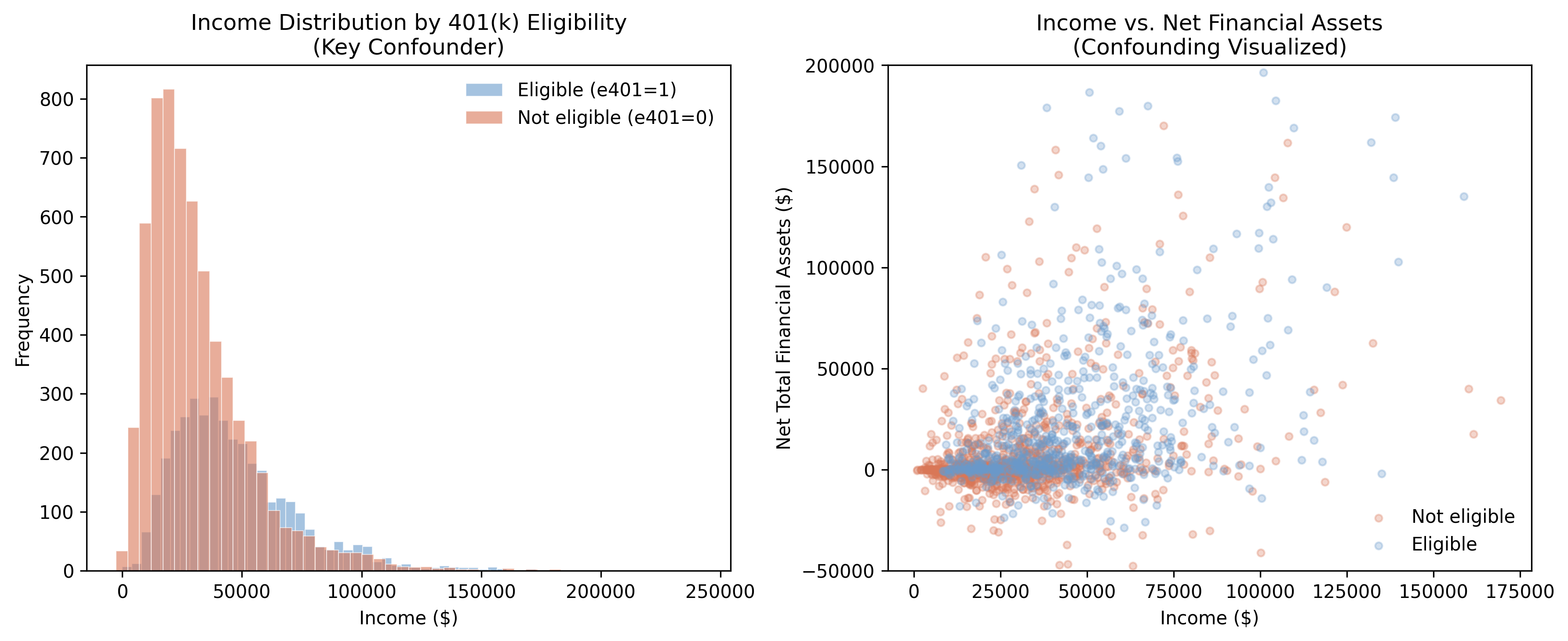

The naive $19,559 is not wrong arithmetic — it is the right gap answering the wrong question. DML’s whole job is to subtract the second term.

DML strips the confounding with two nuisance functions

\[Y = \theta_0 D + g_0(X) + \varepsilon, \qquad D = m_0(X) + V\]

\(g_0(X) = E[Y\mid X]\)

Predict savings from covariates. Residual \(\tilde Y = Y - \hat g_0(X)\) is the unexplained savings.

\(m_0(X) = E[D\mid X]\)

Predict eligibility from covariates. Residual \(\tilde D = D - \hat m_0(X)\) is the surprise eligibility.

Regress \(\tilde Y\) on \(\tilde D\): the slope is \(\hat\theta_0\). Both residuals are cleaned of confounding, so only the causal channel remains.

Two safeguards make ML-based nuisance estimation harmless

Neyman-orthogonal score

The estimating equation’s derivative w.r.t. small nuisance errors is zero at the truth. Sloppy \(\hat g_0, \hat m_0\) barely move \(\hat\theta_0\).

Cross-fitting (K-fold)

Fit \(\hat g_0, \hat m_0\) on \(K-1\) folds, predict on the held-out fold, rotate. No row is ever scored by a model that saw it.

Orthogonality kills regularization bias; cross-fitting kills overfitting bias. Together they let Lasso, forests, or XGBoost serve as nuisance learners with no harm to inference.

The doubly-robust (AIPW) score: an outcome model corrected by inverse-propensity weighting. Consistent if either\(g_0\) or \(m_0\) is right — a safety net.

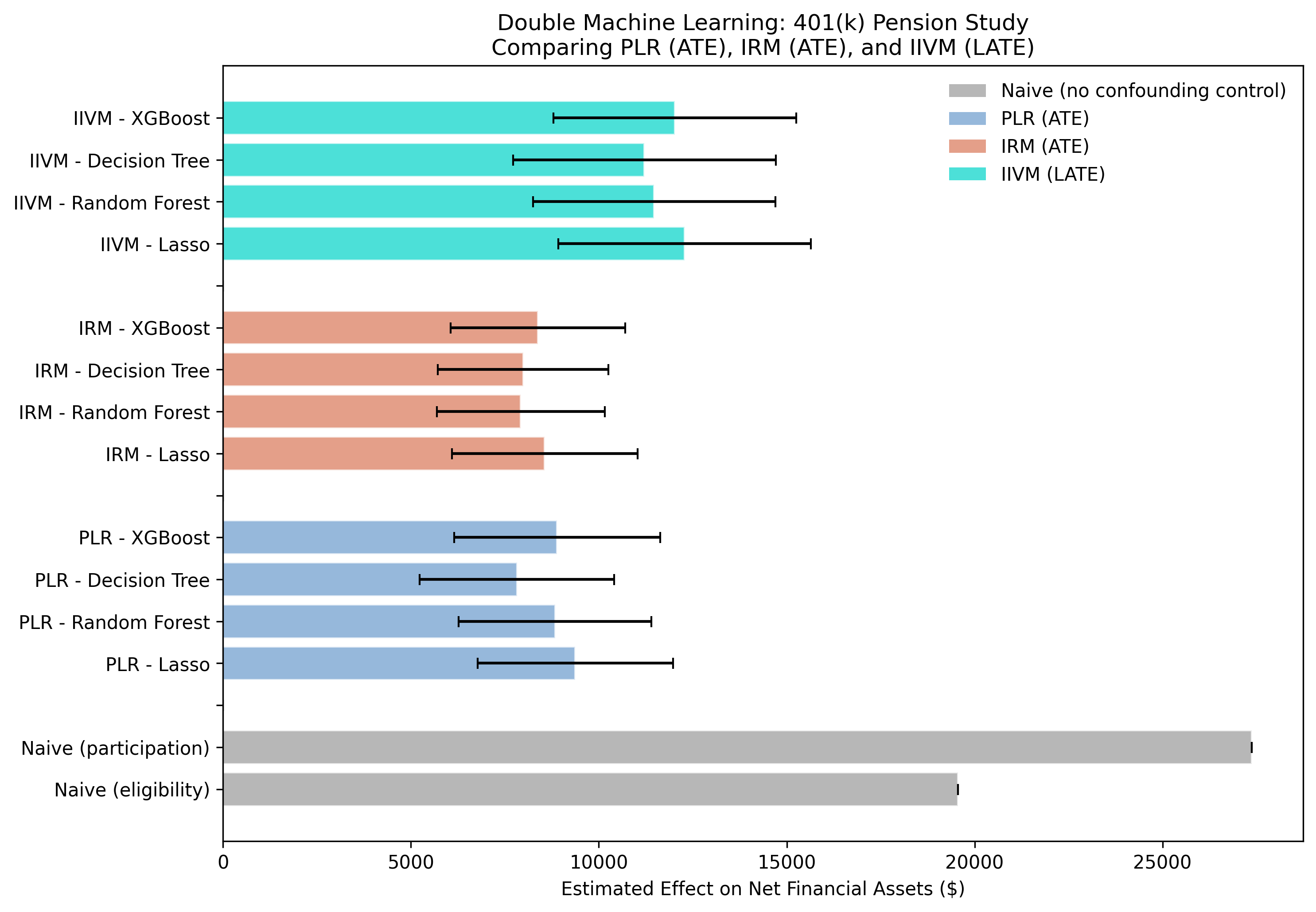

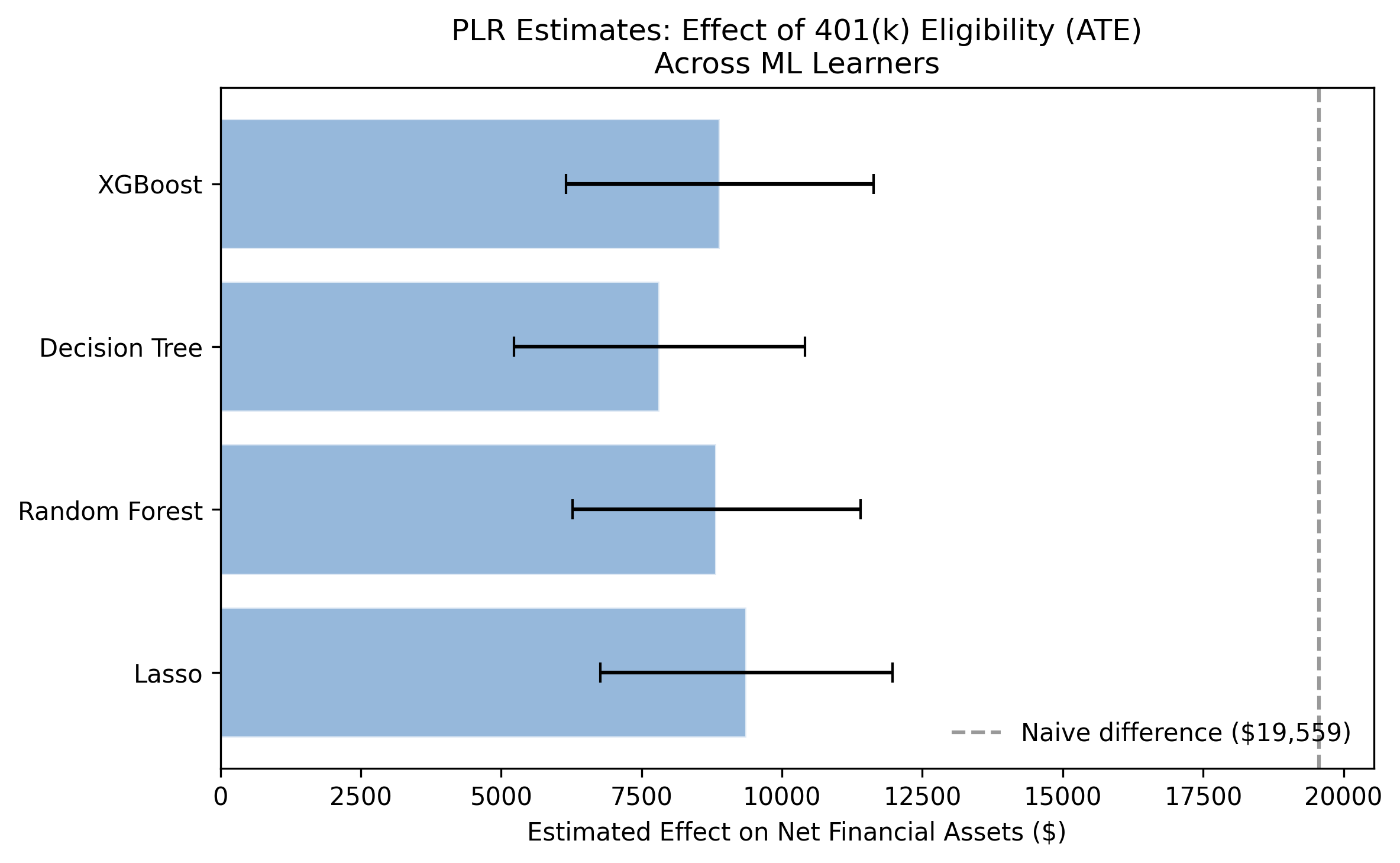

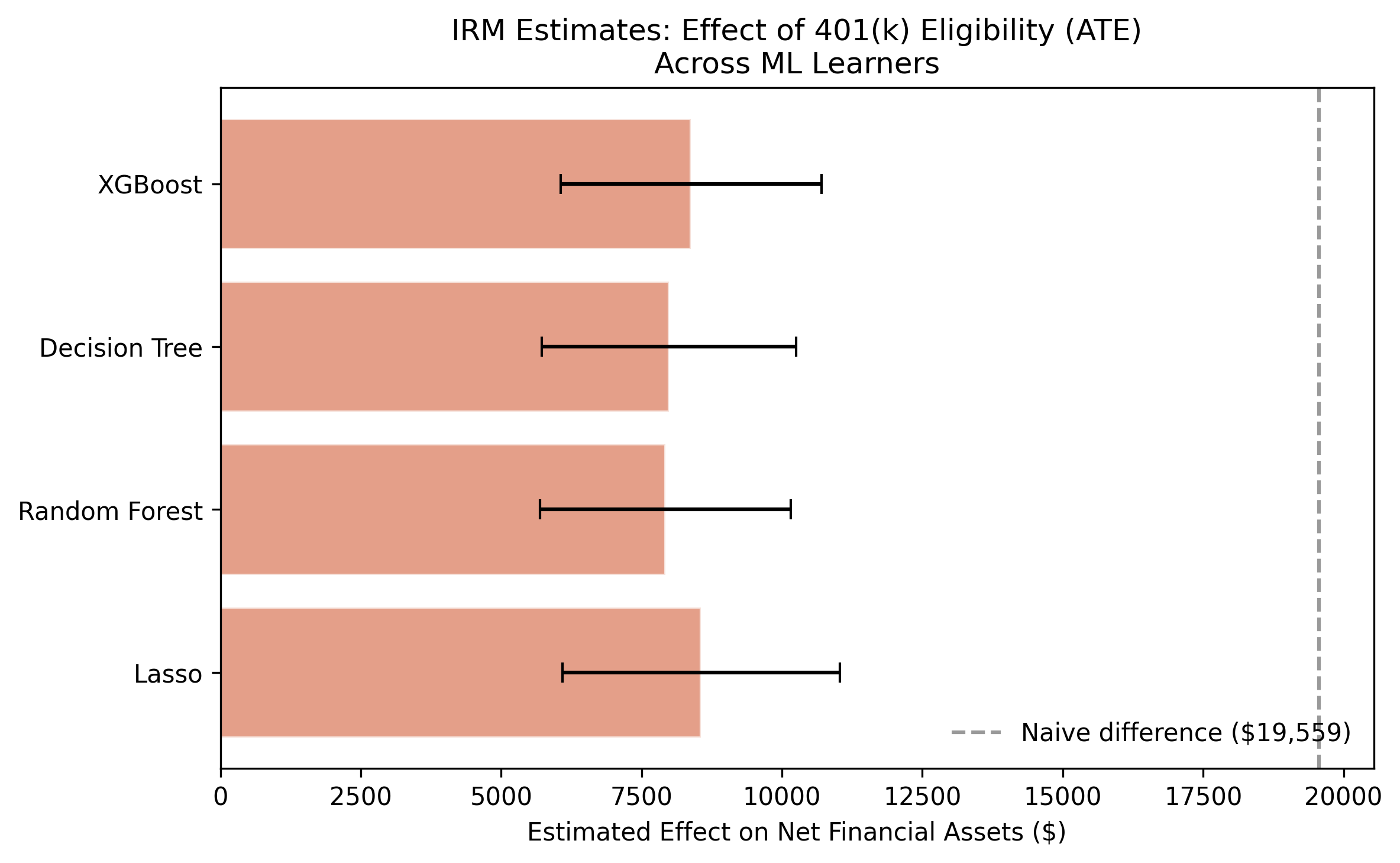

Two different recipes, same answer: PLR and IRM agree within $517

IRM estimates across four learners ($7,924–$8,559) are even tighter than PLR, with smaller standard errors.

Participation is a choice — so we instrument it with eligibility

Participation \(D\) is endogenous (financial discipline is unobserved). Eligibility \(Z\) is a nudge: it opens the door without forcing anyone through.

A Wald-type ratio: the instrument’s effect on savings, divided by its effect on participation.

The instrument only moves the compliers — so the LATE is their effect

Type

Behavior

In the LATE?

Always-takers

Participate regardless of eligibility

no

Never-takers

Never participate, even if eligible

no

Compliers

Participate because eligible

yes

Defiers

Assumed not to exist (monotonicity)

—

The LATE is the effect of participation on the marginal households a policy actually moves.

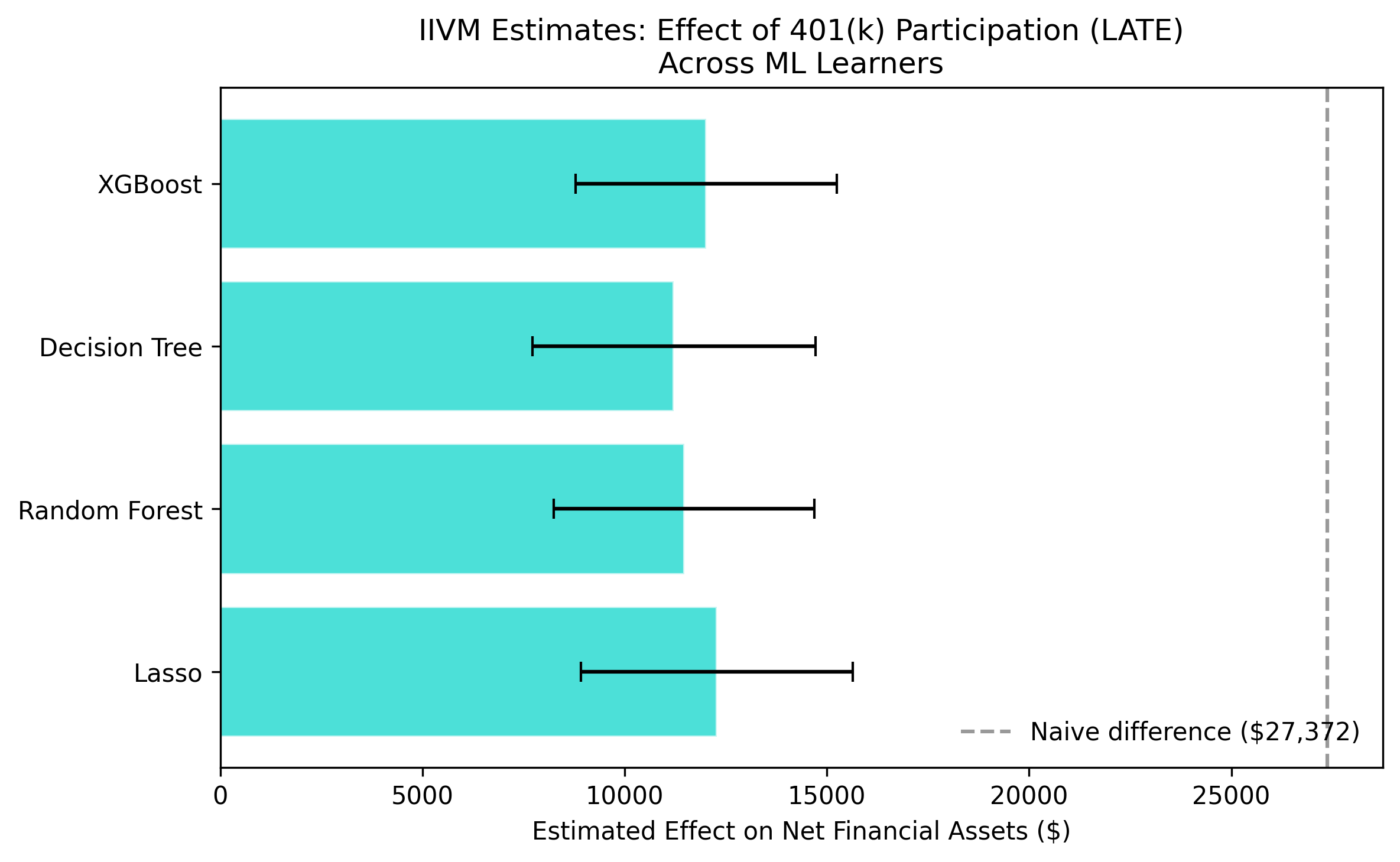

The IIVM LATE is $11,746 — larger than the ATE, by design

IIVM LATE estimates across four learners ($11,215–$12,281) sit well above the ATE band, as expected for compliers.

Estimates barely move across four learners — orthogonality at work

Whole-picture comparison: naive (gray), PLR (steel), IRM (orange), IIVM (teal). Within each model the four learners cluster tightly.

The Resolution

Act III

55% of the naive eligibility gap was pure confounding bias

55%

of the $19,559 naive gap (≈ $10,829) was income-driven bias, not causal effect — the ATE is $8,730

Eligibility genuinely raises savings — about $8,500 per household

$8,730

PLR mean ATE (IRM: $8,213); every 95% CI across two models and four learners excludes zero

For the households a policy actually moves, the effect is $12,000

$11,746

IIVM LATE on compliers — the marginal participants an eligibility expansion targets

Does DML make this causal? No — two assumptions still carry the weight

Objection. Letting an ML model pick the controls can’t manufacture identification.

Response. Correct. DML disciplines estimation, not identification.

The ATE needs conditional exogeneity; the LATE adds instrument validity and monotonicity.

Separate “is the effect real?” from “for whom?” — and let cross-fitting do the rest.