Causal Machine Learning and the Resource Curse with Python EconML

Abstract

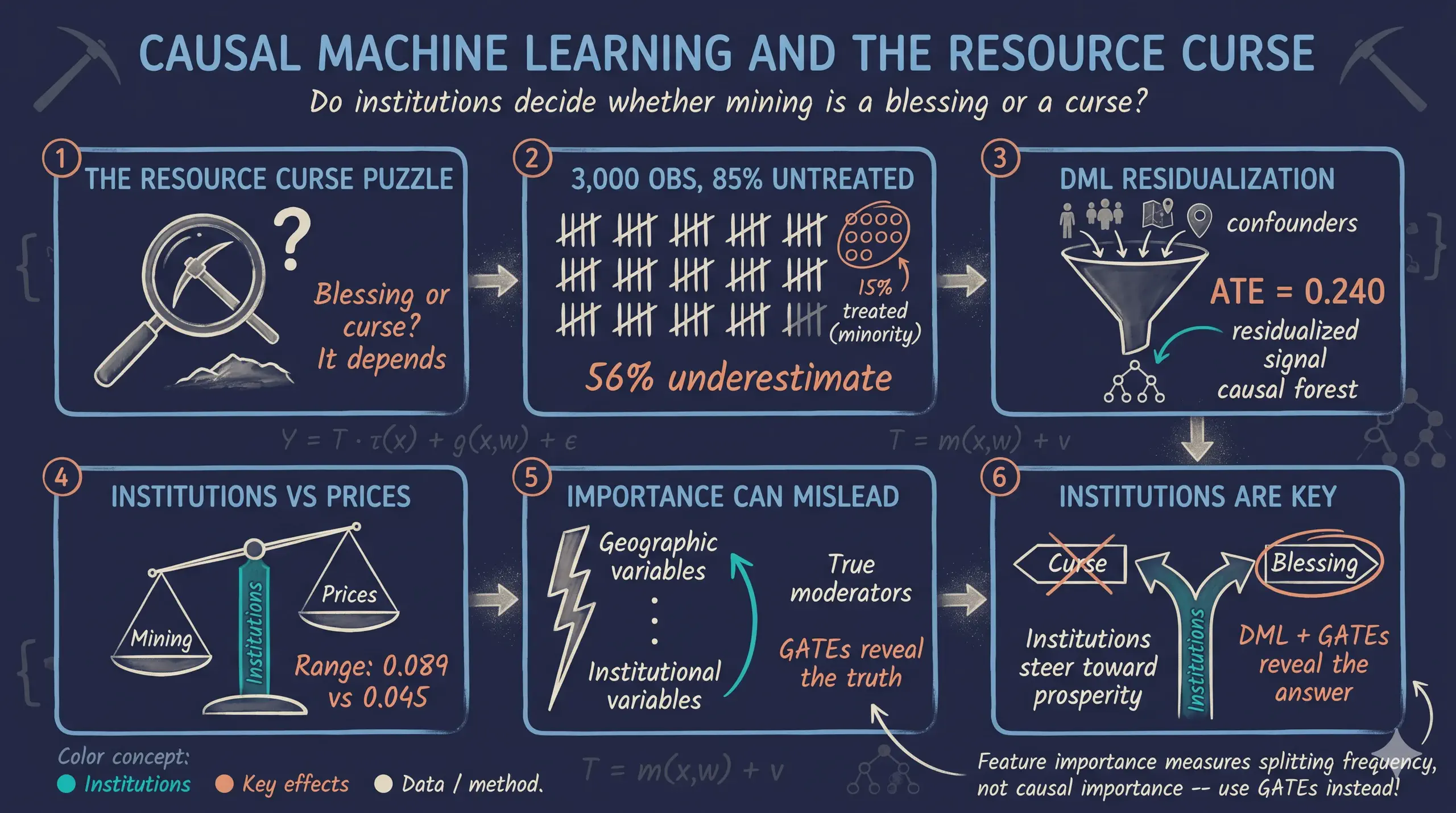

The resource curse hypothesis asks whether natural resource wealth helps or harms economic development, and a growing literature argues that the answer depends on local institutional quality. This tutorial estimates heterogeneous causal effects of mining and mineral prices on development and tests whether institutions moderate the mining margin and the price margin differently. It uses simulated panel data with known ground-truth parameters — 3,000 district-year observations covering 300 districts across 8 countries over 2003–2012 — whose structure mirrors Hodler, Lechner and Raschky (2023); treatment has four levels (no mining, and mining at low, medium, and high prices) and is heavily imbalanced at 85%/5%/5%/5%, with log nighttime lights as the outcome. The method is EconML’s CausalForestDML, a Double Machine Learning causal forest with Gradient Boosting nuisance models, honest trees, 5-fold cross-fitting via GroupKFold on districts, and Bootstrap-of-Little-Bags inference, complemented by GATE estimation and a SingleTreeCateInterpreter. The forest recovers an ATE of 0.240 for the basic mining effect (90% CI [0.124, 0.355]), within sampling error of the true 0.250 and removing nearly all of the 0.141 bias in the naive estimate of 0.109; the price gradient is non-linear (2-1 = 0.029, not significant; 3-1 = 0.220, significant at 5%), and GATEs reveal that institutions moderate the mining effect (range 0.089 across executive-constraint levels) but not the price effect (range 0.045). The exercise demonstrates that causal forests can discover institutional moderation and non-linear shape without parametric pre-specification, while remaining only as credible as the conditional independence assumption.

Overview

Can natural resource wealth be both a blessing and a curse? And can local institutions determine which way it goes? In this tutorial, we use EconML’s CausalForestDML to estimate heterogeneous causal effects of mining and mineral prices on economic development — and test whether institutional quality moderates those effects differently for mining versus price shocks.

We use simulated data with known ground-truth parameters so we can verify that the method recovers the correct answers. The simulated dataset mirrors the structure of Hodler, Lechner & Raschky (2023), who studied 3,800 Sub-Saharan African districts using a Modified Causal Forest. This tutorial focuses on the DML methodology: how the Double Machine Learning framework separates nuisance estimation from causal effect estimation to produce valid, efficient heterogeneous treatment effect estimates.

For the economic narrative and a companion implementation in Stata 19, see Causal Machine Learning and the Resource Curse with Stata 19.

Learning objectives

By the end of this tutorial, you will be able to:

- Understand the Double Machine Learning (DML) framework and the residualization argument that makes it work

- Distinguish heterogeneity features (X) from nuisance controls (W) in

CausalForestDML - Configure

CausalForestDMLfor discrete multi-valued treatments with panel data - Estimate Average Treatment Effects (ATEs) and Group Average Treatment Effects (GATEs), and read the Bootstrap-of-Little-Bags standard errors EconML reports

- Interpret GATE patterns to identify which variables moderate treatment effects

- Use EconML-specific tools like

SingleTreeCateInterpreterfor data-driven subgroup discovery - Evaluate estimated effects against known ground-truth parameters and explain any remaining gap

Key concepts at a glance

The post leans on a small vocabulary repeatedly. The rest of the tutorial assumes you can move between these terms quickly. Each concept below has three parts. The definition is always visible. The example and analogy sit behind clickable cards: open them when you need them, leave them collapsed for a quick scan. If a later section mentions “honest splitting” or “Neyman orthogonality” and the term feels slippery, this is the section to re-read.

1. Potential outcomes $Y_i(t)$. The outcome unit $i$ would take under treatment value $t$. Each unit has one potential outcome per treatment level. We observe only one of them: the one matching the treatment actually received. The rest are counterfactual. They live in worlds we never see.

Example

Take district 47 in 2008. Four potential NTL outcomes exist for it: $Y_{47,2008}(0)$, $Y_{47,2008}(1)$, $Y_{47,2008}(2)$, and $Y_{47,2008}(3)$. They correspond to no mining, low prices, medium prices, and high prices. Only one is in the dataset. It is the one matching whatever treatment that district-year actually had. The other three are forever invisible.

Analogy

Every life decision is a fork in the road. You took one fork. The parallel-universe versions of yourself took the other forks. Their lives are real conceptual objects. You just cannot directly observe them. Causal inference reconstructs those parallel universes. It does so by looking at people who did take the other forks.

2. CATE — Conditional Average Treatment Effect, $\tau(\mathbf{x})$. The average treatment effect for units with covariate profile $\mathbf{x}$. The CATE is a function of $\mathbf{x}$, not a single number. Where the CATE bends with $\mathbf{x}$, the treatment helps some units more than others.

Example

Take a well-governed district profile in our data: exec_constraints = 6, quality_of_govt = 0.7, and so on. For that $\mathbf{x}$ the CATE is $\tau(\mathbf{x}) \approx 0.26$. Mining lifts log-NTL by about 0.26 for that profile. Now move to the weakest-institutions case: exec_constraints = 1. The same function gives only $\tau(\mathbf{x}) \approx 0.18$. The CATE is what makes this comparison possible.

Analogy

A drug’s “average effect” might be a 5-point reduction in blood pressure. But a doctor cares about a specific patient. Maybe a 65-year-old male with diabetes. The CATE is that personalized effect. It takes a patient profile in. It returns the expected effect for someone like them.

3. GATE — Group Average Treatment Effect. The CATE averaged over a pre-specified subgroup. The subgroup is defined by some variable $Z$. GATEs test targeted moderation hypotheses. A typical question: “does institutional quality moderate the effect of mining?”

Example

Sort districts by exec_constraints (1–6). Average the per-observation CATEs inside each level. At level 1 we get $\widehat{\mathrm{GATE}} \approx 0.18$. The number climbs to $\approx 0.26$ at level 6. That climb is the moderation pattern Finding 3 reports. It is exactly what the GATE plots in this post visualize.

Analogy

A nationwide marketing campaign might lift sales by 5% on average. Before scaling it up, the company asks a simple question: did it work better in cities than in rural towns? The GATE answers exactly that. It reports the campaign’s effect inside each store type. It surfaces heterogeneity that the headline ATE hides.

4. ATE — Average Treatment Effect. The CATE averaged over the entire sample, $E[\tau(\mathbf{X})]$. The headline policy number. It answers a single question: if we turned the treatment on for everyone, what average effect would we see?

Example

Take our 3,000 district-years. The estimated ATE for the 1-vs-0 contrast (mining at low prices vs. no mining) is $\widehat{\mathrm{ATE}} = 0.240$. On average, mining-at-low-prices raises log-NTL by 0.24. In unlogged NTL, that is about a 27% bump.

Analogy

“This drug lowers cholesterol by 12 points on average.” That is an ATE statement. A single number, suitable for a press release. It says nothing about whether the drug works better in some patients than others. That question belongs to GATEs and CATEs.

5. Nuisance functions $g_0, m_0$. These are two conditional means: $g_0(\mathbf{x}, \mathbf{w}) = E[Y \mid \mathbf{X}, \mathbf{W}]$ and $m_0(\mathbf{x}, \mathbf{w}) = E[T \mid \mathbf{X}, \mathbf{W}]$. We call them nuisance because we do not care about their values. We estimate them for one reason only. That reason is to strip out the part of $Y$ and $T$ that is predictable from $(\mathbf{X}, \mathbf{W})$. What remains is the variation that identifies the causal effect.

Example

$\hat g_0$ is a Gradient Boosting regressor. It predicts a district’s log-NTL from elevation, ruggedness, ethnic fractionalization, country, year, and so on. It ignores mining status. $\hat m_0$ is a Gradient Boosting classifier. It predicts the probability of each treatment level from the same covariates. Both predictions matter only as inputs to the residualization step.

Analogy

Astronomers photograph faint galaxies in two steps. First, they take a “dark frame” with the lens cap on. The dark frame records sensor noise. Then they subtract it from the real exposure. Nobody hangs the dark frame on their wall. It exists only to be subtracted. $g_0$ and $m_0$ are dark frames for confounding. Their job is to be subtracted out. That is what lets the real causal signal show through.

6. Cross-fitting (sometimes “sample-splitting” or “out-of-fold prediction”). Estimate the nuisance functions on one fold of the data. Apply them to a held-out fold. Rotate so that every observation is residualized using nuisance models that did not see it. Without this rotation, in-sample residuals come out systematically too small. That bias propagates straight into the second stage.

Example

Setting cv=5 in CausalForestDML splits the 3,000 observations into five folds of 600. The forest fits $\hat g_0$ and $\hat m_0$ on folds 1–4. It then residualizes fold 5 using those fitted models. The procedure rotates four more times. The end result: each district-year is residualized by nuisance models trained on a strictly disjoint sample.

Analogy

Suppose you give a class the same problems for practice and for the final exam. Students who memorized the practice will ace the final. The score reflects memorization, not learning. Hiding the final-exam questions until grading time fixes the problem. Cross-fitting does the same trick. It hides each observation from the very nuisance model that will eventually residualize it.

7. Honest splitting (a property of an honest causal forest). A causal tree uses one random subsample to choose its split structure: which variable, which threshold. It uses a separate random subsample to estimate the treatment-effect value in each leaf. The split-chooser and the leaf-estimator never share data. This separation is what licenses valid confidence intervals from the forest.

Example

Consider a single tree inside the forest. With honest=True, half of its bootstrap sample picks the splits. Maybe the choice is “split first on distance_capital, then on exec_constraints”. The other half computes the average CATE in each resulting leaf. Those leaf-level numbers are unbiased. The reason: the splits were chosen without seeing them.

Analogy

A jury that hears the evidence should not also write the verdict template. If the same people pick the conclusion language and hear the case, the verdict reflects their pre-baked preferences. It would not reflect the evidence alone. Splitting the two roles is a basic guard against motivated reasoning. Honesty does the same job inside one tree. Split-choosers and leaf-estimators are different “people”. The leaf values cannot be tailored to the splits that produced them.

8. Neyman orthogonality. A property of the DML estimating equation $\psi(W; \tau, \eta)$. Here $\eta = (g_0, m_0)$ collects the nuisance functions. The property is $\left.\partial_\eta E[\psi]\right|_{\eta=\eta_0} = 0$. In words: at the truth, the expected estimating equation is flat in the nuisance functions. Small errors in $\hat g_0$ and $\hat m_0$ enter the second-stage estimator only at second order.

Example

Suppose $\hat g_0$ misses the true $g_0$ by 10% on average. A naive plug-in two-stage procedure inherits roughly that 10% error in the causal estimate. With Neyman orthogonality, the picture changes. The same 10% nuisance error contributes only on the order of $(0.10)^2 = 0.01$ to the causal estimate. That is one percentage point — orders of magnitude less than the input. This is why a Gradient Boosting first stage works. It converges at a slower-than-parametric rate. Even so, the second-stage estimate of $\tau$ remains $\sqrt{n}$-consistent and asymptotically normal.

Analogy

Picture a self-righting boat. You can lean over the rail. You can slosh the cargo. You can even slip on the deck. The hull pulls itself upright every time. Stability is built into its geometry, not into never being disturbed. Neyman orthogonality is the hull design. It lets DML stay upright when the nuisance estimates wobble.

The DML Causal Forest

Potential outcomes and the CATE

Causal inference rests on the potential-outcomes framework (Rubin, 1974; Imbens & Rubin, 2015). For each unit $i$ and each treatment value $t$, we imagine an outcome $Y_i(t)$ that would be realized if $i$ received treatment $t$. The catch is the fundamental problem of causal inference: only the potential outcome corresponding to the treatment unit $i$ actually receives is observable. All other potential outcomes for that unit are counterfactual — they live in a world we never see. Causal inference is therefore an exercise in imputation: using the observed outcomes of comparable units to stand in for the missing counterfactuals.

The Conditional Average Treatment Effect (CATE) for a unit with covariates $\mathbf{x}$ is

$$\tau(\mathbf{x}) = E\{Y_i(1) - Y_i(0) \mid \mathbf{X}_i = \mathbf{x}\}.$$

In words: among units who look like $\mathbf{x}$, what is the average gap between the treated and untreated potential outcomes? When the function $\tau(\cdot)$ is constant across $\mathbf{x}$, every type of unit responds the same way and a single ATE summarizes everything. When $\tau(\cdot)$ bends with $\mathbf{x}$, we have treatment effect heterogeneity — mining might raise nighttime lights in well-governed districts and barely move them elsewhere. Estimating that bend, not just its average, is the whole point of a causal forest.

The partially linear model with heterogeneous effects

EconML’s CausalForestDML works inside the partially linear model of Robinson (1988), extended by Chernozhukov et al. (2018) to allow heterogeneous effects:

$$Y_i = \tau(\mathbf{X}_i)\, T_i + g_0(\mathbf{X}_i, \mathbf{W}_i) + \varepsilon_i, \qquad E[\varepsilon_i \mid \mathbf{X}_i, \mathbf{W}_i] = 0.$$

$$T_i = m_0(\mathbf{X}_i, \mathbf{W}_i) + v_i, \qquad E[v_i \mid \mathbf{X}_i, \mathbf{W}_i] = 0.$$

The outcome equation says that $Y_i$ depends on the treatment $T_i$ multiplied by a unit-specific effect $\tau(\mathbf{X}_i)$, plus an arbitrary, possibly nonlinear function $g_0$ of the controls, plus mean-zero noise. The “partially linear” name comes from $T$ entering linearly (multiplied by $\tau$) while $g_0$ is allowed to be any flexible function.

The treatment equation writes $T_i$ as the conditional-mean treatment $m_0(\mathbf{X}_i, \mathbf{W}_i)$ plus a residual $v_i$. For a continuous treatment, $m_0$ is a regression. For our four-level treatment, $m_0$ is a multi-class classifier — specifically, a GradientBoostingClassifier — and “$T - m_0$” is shorthand for the residual of treatment around its conditional probabilities.

The functions $g_0$ and $m_0$ are called nuisance functions because we do not care about their values. We estimate them only to remove the part of $Y$ and $T$ that is predictable from $(\mathbf{X}, \mathbf{W})$, leaving behind the variation that identifies the causal effect.

Why two stages? The residualization argument

Subtract $E[Y_i \mid \mathbf{X}, \mathbf{W}] = \tau(\mathbf{X}_i) \, m_0(\mathbf{X}_i, \mathbf{W}_i) + g_0(\mathbf{X}_i, \mathbf{W}_i)$ from the outcome equation. The $g_0$ terms cancel, and after a line of algebra. Define the residualized outcome and treatment as

$$\tilde Y_i = Y_i - E[Y_i \mid \mathbf{X}, \mathbf{W}], \qquad \tilde T_i = T_i - m_0(\mathbf{X}_i, \mathbf{W}_i).$$

Plugging these residuals into the partial linear model yields:

$$\tilde Y_i = \tau(\mathbf{X}_i) \cdot \tilde T_i + \varepsilon_i.$$

So if we (a) estimate $g_0$ and $m_0$ in a first stage with any flexible learner, (b) residualize both $Y$ and $T$, and (c) regress $\tilde Y$ on $\tilde T$ with covariate-dependent slope, that slope at point $\mathbf{x}$ recovers $\tau(\mathbf{x})$. This is exactly the Frisch–Waugh–Lovell logic — if you have not seen FWL before, the tutorial on the Frisch–Waugh–Lovell theorem walks through the linear case in detail.

The causal forest is the second-stage learner that estimates this covariate-dependent slope from $(\tilde T, \tilde Y, \mathbf{X})$, splitting on $\mathbf{X}$ to find regions where the local slope is approximately constant.

Neyman orthogonality: why first-stage errors barely matter

Think of residualization like noise-canceling headphones: the first stage removes the “background noise” of confounders from both the outcome and the treatment, so the causal forest only hears the “signal” of the treatment effect.

The formal version of that intuition is Neyman orthogonality. The DML estimating equation $\psi(W; \tau, \eta)$ — where $\eta = (g_0, m_0)$ collects the nuisance functions — satisfies

$$\left.\frac{\partial}{\partial \eta} E[\psi(W; \tau, \eta)] \right|_{\eta = \eta_0} = 0.$$

In words: at the truth, the expected estimating equation is flat in the nuisance functions. Small errors in $\hat g_0$ and $\hat m_0$ enter the second-stage estimator only through second-order terms. The practical consequence is striking: even if Gradient Boosting estimates $g_0$ and $m_0$ at the slow rate $O(n^{-1/4})$, much slower than the parametric $\sqrt{n}$ rate, the resulting estimate of $\tau$ is still $\sqrt{n}$-consistent and asymptotically normal (Chernozhukov et al., 2018, §2.2). A naive plug-in two-stage procedure — one that does not use the orthogonal moment — inherits the slower nuisance rate and loses valid inference.

Three levels of effects

The causal forest produces per-observation CATE estimates, which aggregate to three levels with different uses:

| Level | Notation | What it measures | When to report |

|---|---|---|---|

| CATE | $\tau(\mathbf{x})$ | Effect for a unit with covariates $\mathbf{x}$ | Exploratory: feed into a decision tree or partial-dependence plot to see how effects vary. |

| GATE | $E[\tau(\mathbf{X}) \mid Z = z]$ | Average CATE in a pre-specified subgroup defined by a variable $Z$ | Theory-driven: testing whether a named covariate (e.g., institutional quality) moderates the effect. |

| ATE | $E[\tau(\mathbf{X})]$ | Overall average across all units | Policy: the headline number for “what happens on average if we turn the treatment on?” |

DML pipeline

flowchart LR

A["<b>Panel Data</b><br/>3,000 obs"]:::data

B["<b>First Stage</b><br/>GBM nuisance<br/>models"]:::first

C["<b>Residualize</b><br/>Y - E[Y | X,W]<br/>T - E[T | X,W]"]:::resid

D["<b>Causal Forest</b><br/>500 honest trees"]:::forest

E["<b>CATEs</b><br/>Per-observation<br/>effects"]:::cate

A --> B --> C --> D --> E

classDef data fill:#6a9bcc,stroke:#141413,color:#fff

classDef first fill:#d97757,stroke:#141413,color:#fff

classDef resid fill:#00d4c8,stroke:#141413,color:#141413

classDef forest fill:#141413,stroke:#d97757,color:#fff

classDef cate fill:#6a9bcc,stroke:#141413,color:#fff

Setup and configuration

We use CausalForestDML from EconML with Gradient Boosting nuisance models. The ground-truth parameters are defined inline so the tutorial is fully self-contained.

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from econml.dml import CausalForestDML

from sklearn.ensemble import (GradientBoostingRegressor,

GradientBoostingClassifier)

# Ground-truth ATEs from the data-generating process

TRUE_ATES = {

'1-0': 0.250, # Mining effect

'2-0': 0.300, # Mining + medium price

'3-0': 0.550, # Mining + high price

'2-1': 0.050, # Medium price premium (small)

'3-1': 0.300, # High price premium (large)

'3-2': 0.250, # High vs medium step

}

Load the simulated data

The dataset simulates 300 districts across 8 countries observed over 10 years (2003–2012), following the structure of Hodler, Lechner & Raschky (2023). Treatment has four levels: no mining (0), mining at low prices (1), medium prices (2), and high prices (3).

DATA_URL = ("https://github.com/cmg777/starter-academic-v501"

"/raw/master/content/post/python_EconML/sim_resource_curse.csv")

df = pd.read_csv(DATA_URL)

print(f"Dataset: {len(df):,} observations")

print(f"Districts: {df['district_id'].nunique()}, "

f"Countries: {df['country_id'].nunique()}")

Dataset: 3,000 observations

Districts: 300, Countries: 8

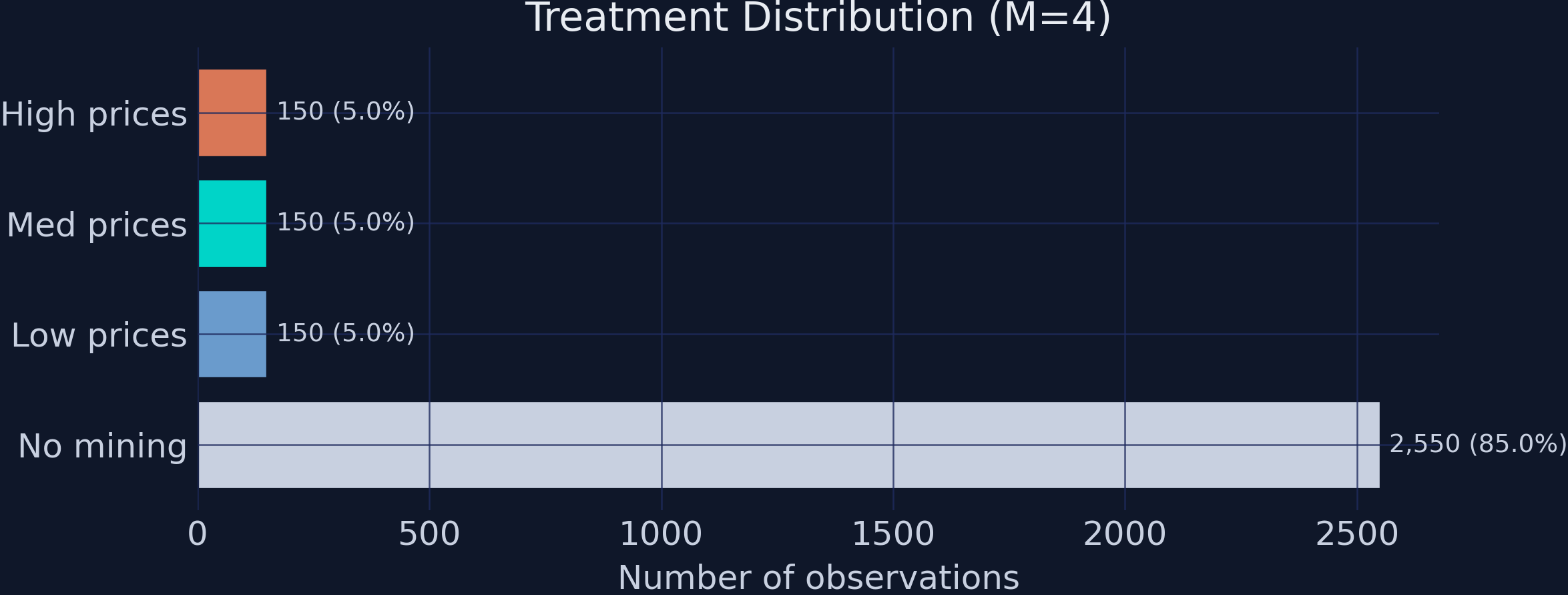

The dataset contains 3,000 district-year observations with a heavily imbalanced treatment: 85% of observations are untreated (no mining), while each of the three mining groups comprises only 5% of the data. This imbalance makes causal inference challenging — the causal forest must learn from relatively few treated observations.

Descriptive statistics

Treatment distribution

labels = {0: 'No mining', 1: 'Low prices',

2: 'Med prices', 3: 'High prices'}

for t, n in df['treatment'].value_counts().sort_index().items():

print(f" {t} ({labels[t]}): {n:,} ({n/len(df):.1%})")

0 (No mining): 2,550 (85.0%)

1 (Low prices): 150 (5.0%)

2 (Med prices): 150 (5.0%)

3 (High prices): 150 (5.0%)

Treatment distribution across the four groups. The 85/5/5/5 imbalance makes causal inference challenging.

Treatment distribution across the four groups. The 85/5/5/5 imbalance makes causal inference challenging.

The 85/5/5/5 split means the causal forest has 2,550 control observations but only 150 per treatment level. For within-mining comparisons (e.g., 3-1), only 300 observations contribute, making standard errors larger for price-effect estimates.

Outcomes by treatment group

for t in sorted(df['treatment'].unique()):

mask = df['treatment'] == t

m_ntl = df.loc[mask, 'ntl_log'].mean()

m_conf = df.loc[mask, 'conflict'].mean()

print(f" {t} ({labels[t]}): NTL={m_ntl:.3f} Conflict={m_conf:.1%}")

0 (No mining): NTL=-1.137 Conflict=10.7%

1 (Low prices): NTL=-1.028 Conflict=18.0%

2 (Med prices): NTL=-0.930 Conflict=18.0%

3 (High prices): NTL=-0.615 Conflict=28.0%

The raw means show a clear gradient: higher treatment levels are associated with higher NTL and higher conflict rates. But these raw comparisons are biased because mining districts differ systematically from non-mining districts in geography, institutions, and economic development.

Naive comparison: why we need causal ML

for comp in ['1-0', '2-1', '3-1']:

a, b = int(comp[0]), int(comp[2])

naive = df.loc[df['treatment']==a, 'ntl_log'].mean() - \

df.loc[df['treatment']==b, 'ntl_log'].mean()

truth = TRUE_ATES[comp]

print(f" {comp}: Naive={naive:.3f} Truth={truth:.3f} Bias={naive-truth:+.3f}")

1-0: Naive=0.109 Truth=0.250 Bias=-0.141

2-1: Naive=0.098 Truth=0.050 Bias=+0.048

3-1: Naive=0.413 Truth=0.300 Bias=+0.113

The naive 1-0 estimate of 0.109 is severely biased downward from the true effect of 0.250 — a 56% underestimate. This happens because mining districts tend to have worse geographic and institutional characteristics that independently reduce development. The DML Causal Forest removes this selection bias by residualizing both the outcome and the treatment against observed confounders before estimating the causal effect.

EconML estimation

Configuration

We separate covariates into two groups with distinct roles in the DML framework:

- X features (10 variables): Enter the causal forest and can drive treatment effect heterogeneity. These include

exec_constraints,quality_of_govt,gdp_pc,elevation,temperature,ruggedness,distance_capital,agri_suitability,population, andethnic_frac. - W controls (2 variables): Used only in the first-stage nuisance models (

country_id,year). These absorb country and time fixed effects but do not enter the causal forest.

X_COLS = ['exec_constraints', 'quality_of_govt', 'gdp_pc',

'elevation', 'temperature', 'ruggedness',

'distance_capital', 'agri_suitability', 'population',

'ethnic_frac']

W_COLS = ['country_id', 'year']

Fitting the model

Y = df['ntl_log'].values

T = df['treatment'].values

X = df[X_COLS].values

W = df[W_COLS].values

est_ntl = CausalForestDML(

model_y=GradientBoostingRegressor(n_estimators=200, max_depth=4,

random_state=42),

model_t=GradientBoostingClassifier(n_estimators=200, max_depth=4,

random_state=42),

discrete_treatment=True,

categories=[0, 1, 2, 3],

n_estimators=500,

min_samples_leaf=10,

honest=True, # Separate split/estimation samples

inference=True, # BLB confidence intervals

cv=5, # 5-fold cross-fitting

n_jobs=1,

random_state=42,

)

est_ntl.fit(Y, T, X=X, W=W, groups=df['district_id'].values)

NTL: fitted in ~25s

Several configuration choices deserve explanation.

Honest trees (honest=True) split the data inside each tree into two halves. One half is used to choose the splits — which variable, which threshold — and the other half is used to estimate the leaf means. A standard regression tree uses the same observations for both jobs, which lets the tree pick splits that artificially separate noisy observations and then quote the resulting separation back as if it were signal. The “exam writer / exam taker” analogy: honesty stops the tree from setting questions it has already memorized the answers to. Operationally, honesty is what licenses asymptotically valid confidence intervals — without it, the leaf estimates are tighter than they should be and inference=True’s reported standard errors would be misleadingly small. Wager & Athey (2018) formalize the result and prove $\sqrt{n}$-asymptotic normality for honest causal forests.

Cross-fitting (cv=5) addresses a different overfitting risk. When the same data are used to estimate the nuisance functions $\hat g_0, \hat m_0$ and to apply them as residualizers, in-sample residuals are too small on average and bias the second stage. Cross-fitting splits the data into 5 folds, fits the nuisance models on 4 of them, applies the fitted models to the held-out fold, and rotates. Each observation is residualized using nuisance estimates that did not see it.

GroupKFold via groups=district_id. Our panel observes each district across multiple years. Plain $K$-fold would scatter rows from the same district across folds, so the nuisance models would peek at most of a district’s rows when predicting one held-out year — leakage that artificially shrinks first-stage residuals. Passing groups=df['district_id'].values to fit() triggers GroupKFold, which keeps every district inside one fold.

A common confusion: GroupKFold is not the same as clustered standard errors. It blocks within-district leakage in cross-fitting; it does not adjust the second-stage variance for within-district correlation in the residuals. The standard errors EconML reports are forest-level Bootstrap-of-Little-Bags SEs that treat observations as independent. With panel data, true clustered SEs would typically be larger. We flag this as a limitation again in the Discussion section.

Identification: the Conditional Independence Assumption

The causal forest leans on the Conditional Independence Assumption (CIA), also called unconfoundedness or selection on observables: after conditioning on the observed covariates $(X, W)$, treatment assignment is as good as random, in the sense that

$$\{Y_i(0), Y_i(1), Y_i(2), Y_i(3)\} \perp T_i \mid (\mathbf{X}_i, \mathbf{W}_i).$$

In plain English: once we know a district’s geography, institutions, demographics, country, and year, knowing whether mining is active there tells us nothing more about what its potential nighttime-lights outcomes would be. Because we built the simulated data ourselves, the CIA holds by construction — every confounder we created is in $(X, W)$.

In real data, the CIA is untestable and easy to violate. Two concrete violation channels for this application:

- Mineral surveys. Mining companies often arrive in a district because a geological survey flagged the geology as promising. The same survey may also predict future infrastructure investment unrelated to mining. If those surveys are not in $(X, W)$, both treatment and the potential outcome are correlated with an unobserved confounder.

- Political connections. Districts whose elites are aligned with the central government may both attract mining concessions and receive non-mining infrastructure (roads, electrification). An analyst without a measure of political alignment would mis-attribute the infrastructure effect to mining.

Hodler, Lechner & Raschky (2023) defend the CIA in their setting by including a rich set of geological, geographic, and institutional controls; the methodology in this tutorial is no stronger than that defense.

Average Treatment Effects

EconML’s ate_inference() returns the average causal effect for a chosen pair of treatment levels, together with a standard error and a confidence interval.

The standard error here is the SE of the forest-level ATE point estimate, not the SE of any one unit’s CATE. It comes from the Bootstrap of Little Bags (BLB), a sub-bootstrap procedure (Athey, Tibshirani & Wager, 2019, §4) tailored to forests. Rather than refit hundreds of full forests — which would cost $O(B \cdot \text{forest})$ — BLB partitions the existing forest’s trees into “bags”, computes bag-level estimates, and uses the variance across bags as an estimate of the sampling variance of the full-forest ATE. The trick exploits the conditional independence of trees grown on different sub-samples; it returns valid asymptotic confidence intervals at a fraction of the cost of the obvious resampling scheme. EconML enables BLB whenever you pass inference=True to the constructor.

We report 90% intervals (alpha=0.1) by default — the convention used in Athey, Tibshirani & Wager (2019) and Hodler, Lechner & Raschky (2023). The substantive conclusions are unchanged at 95%, but the wider intervals make the price-effect comparisons (which have low power because only 150 observations per treatment level contribute) look more uncertain than the asymmetric pattern actually warrants.

We compute all six pairwise treatment contrasts:

comparisons = [

('1-0', 0, 1), ('2-0', 0, 2), ('3-0', 0, 3),

('2-1', 1, 2), ('3-1', 1, 3), ('3-2', 2, 3),

]

for comp_label, t0, t1 in comparisons:

res = est_ntl.ate_inference(X, T0=t0, T1=t1)

lo, hi = res.conf_int_mean(alpha=0.1)

print(f" {comp_label}: ATE={res.mean_point:.4f} "

f"SE={res.stderr_mean:.4f} 90%CI=[{lo:.3f}, {hi:.3f}]")

1-0: ATE=0.2398 SE=0.0701 90%CI=[0.124, 0.355]

2-0: ATE=0.2684 SE=0.0791 90%CI=[0.138, 0.399]

3-0: ATE=0.4598 SE=0.0811 90%CI=[0.326, 0.593]

2-1: ATE=0.0286 SE=0.1008 90%CI=[-0.137, 0.194]

3-1: ATE=0.2200 SE=0.1013 90%CI=[0.053, 0.387]

3-2: ATE=0.1914 SE=0.1093 90%CI=[0.012, 0.371]

Finding 1: Mining raises economic activity, after controlling for confounding. All three mining-vs-no-mining contrasts (1-0, 2-0, 3-0) are positive, with point estimates well separated from zero relative to their standard errors. The basic mining effect 1-0 is 0.240 (SE = 0.070, 90% CI = [0.124, 0.355]) — comfortably above zero and within sampling error of the ground-truth 0.250. The naive difference-in-means for the same contrast was 0.109; the DML forest has eliminated nearly all of that confounding bias. Because the outcome is log nighttime lights, an effect of 0.24 corresponds to roughly a 27% increase in unlogged NTL ($e^{0.24} - 1 \approx 0.27$).

Finding 2: The price gradient is non-linear. Comparing medium prices to low prices (2-1) returns an ATE of 0.029 with an SE of 0.101 — the 90% interval [-0.137, 0.194] easily contains zero. Medium prices, in this DGP, add nothing detectable beyond the basic mining effect. The high-vs-low contrast (3-1), in contrast, is 0.220 (SE = 0.101) and significant at the 5% level, with a 90% interval that excludes zero. The high-vs-medium step (3-2) is 0.191 and significant at 10%. The forest has recovered the qualitative shape of the true price-response curve — flat at low-to-medium prices, jumping at high prices — without being told to look for a non-linearity. This is the kind of finding causal ML buys you: shape discovery without functional-form pre-specification.

Treatment effect heterogeneity (GATEs)

Computing GATEs from per-observation CATEs

EconML returns per-observation CATEs through effect_inference(). To form a GATE we average those CATEs within a chosen subgroup, and to form a standard error we propagate the per-observation BLB standard errors. Doing this by hand is more illuminating than a one-line API call — it makes the relationship between CATE-level heterogeneity and group-level effects visible.

def compute_gate(est, df, z_var, t0, t1):

inf = est.effect_inference(X, T0=t0, T1=t1)

ite, ite_se = inf.point_estimate, inf.stderr

for z in sorted(df[z_var].unique()):

mask = df[z_var].values == z

gate = ite[mask].mean()

# Propagate BLB standard errors (see derivation below)

gate_se = np.sqrt(np.mean(ite_se[mask]**2) / mask.sum())

For a subgroup $g$ of size $n_g$, the GATE estimator is the simple average of the per-observation CATE estimates,

$$\widehat{\mathrm{GATE}}_g = \frac{1}{n_g} \sum_{i \in g} \widehat\tau(\mathbf{X}_i).$$

If we treat the $\widehat\tau(\mathbf{X}_i)$ as approximately uncorrelated within the group — a working assumption, since EconML’s BLB does not return their full covariance matrix — the variance of their average is

$$\mathrm{Var}\left(\widehat{\mathrm{GATE}}_g\right) \approx \frac{1}{n_g^2} \sum_{i \in g} \mathrm{Var}\left(\widehat\tau(\mathbf{X}_i)\right) = \frac{1}{n_g} \cdot \overline{\mathrm{SE}_i^2}.$$

Taking the square root gives the formula in the code: sqrt(mean(se_i^2) / n_g). The CIs we report are point $\pm 1.645 \cdot \widehat{\mathrm{SE}}$ for a 90% level. Two caveats are worth flagging up front: (i) the within-group independence assumption probably understates the SE in panel data where the same district appears multiple times in the same group, and (ii) this SE captures estimation uncertainty in the CATE function only, not sampling variability of the subgroup composition. As with the ATE, the headline qualitative pattern survives at 95% intervals.

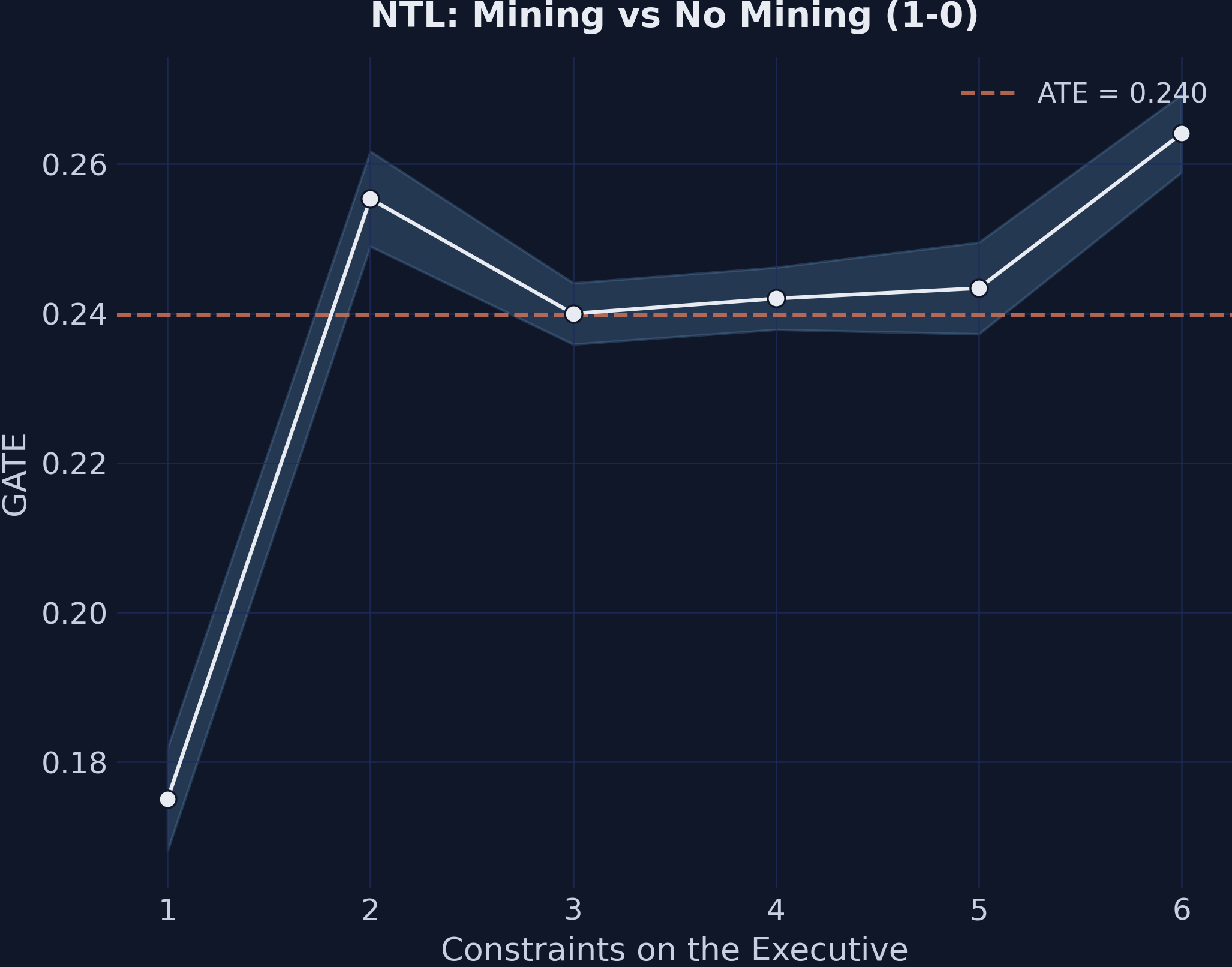

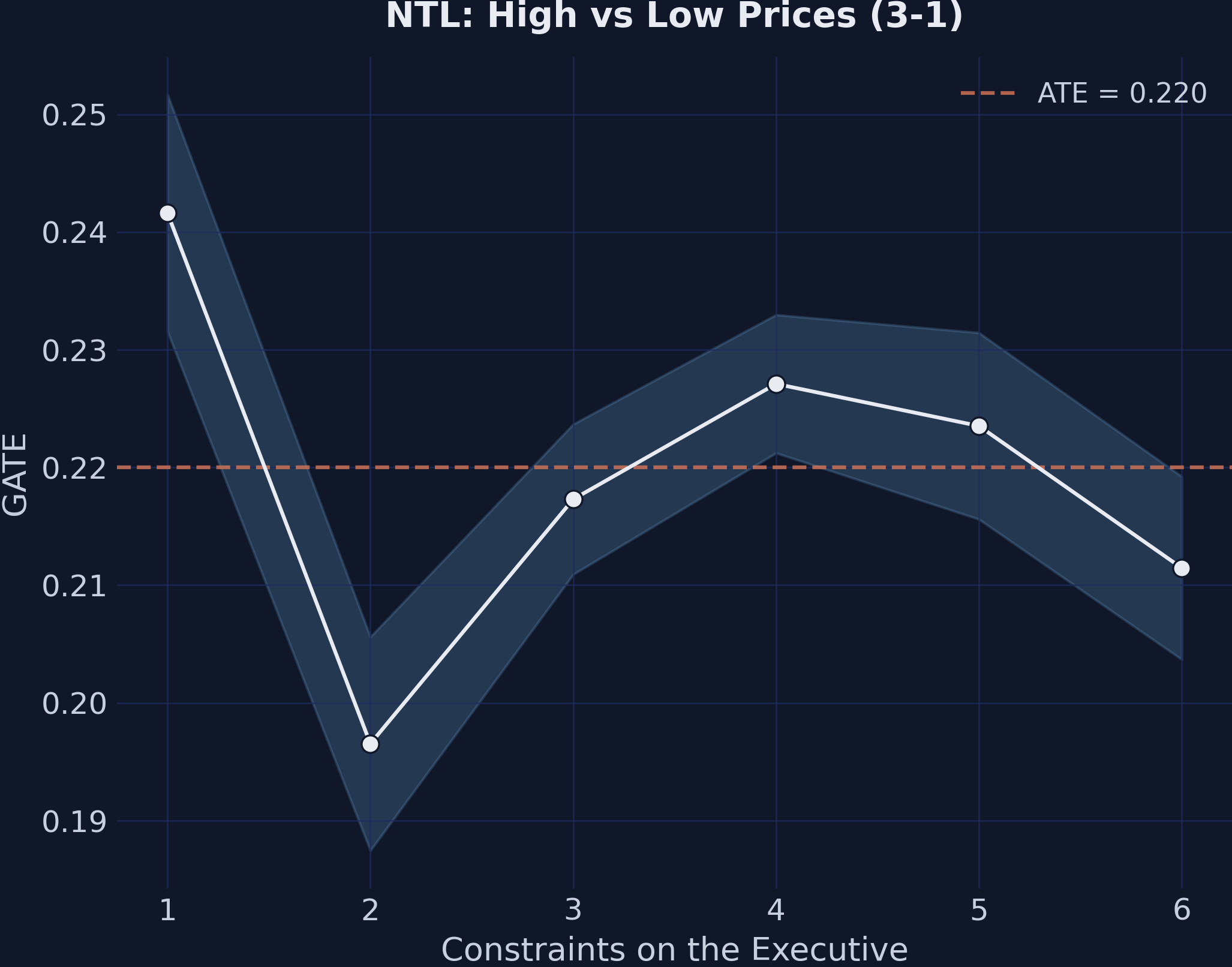

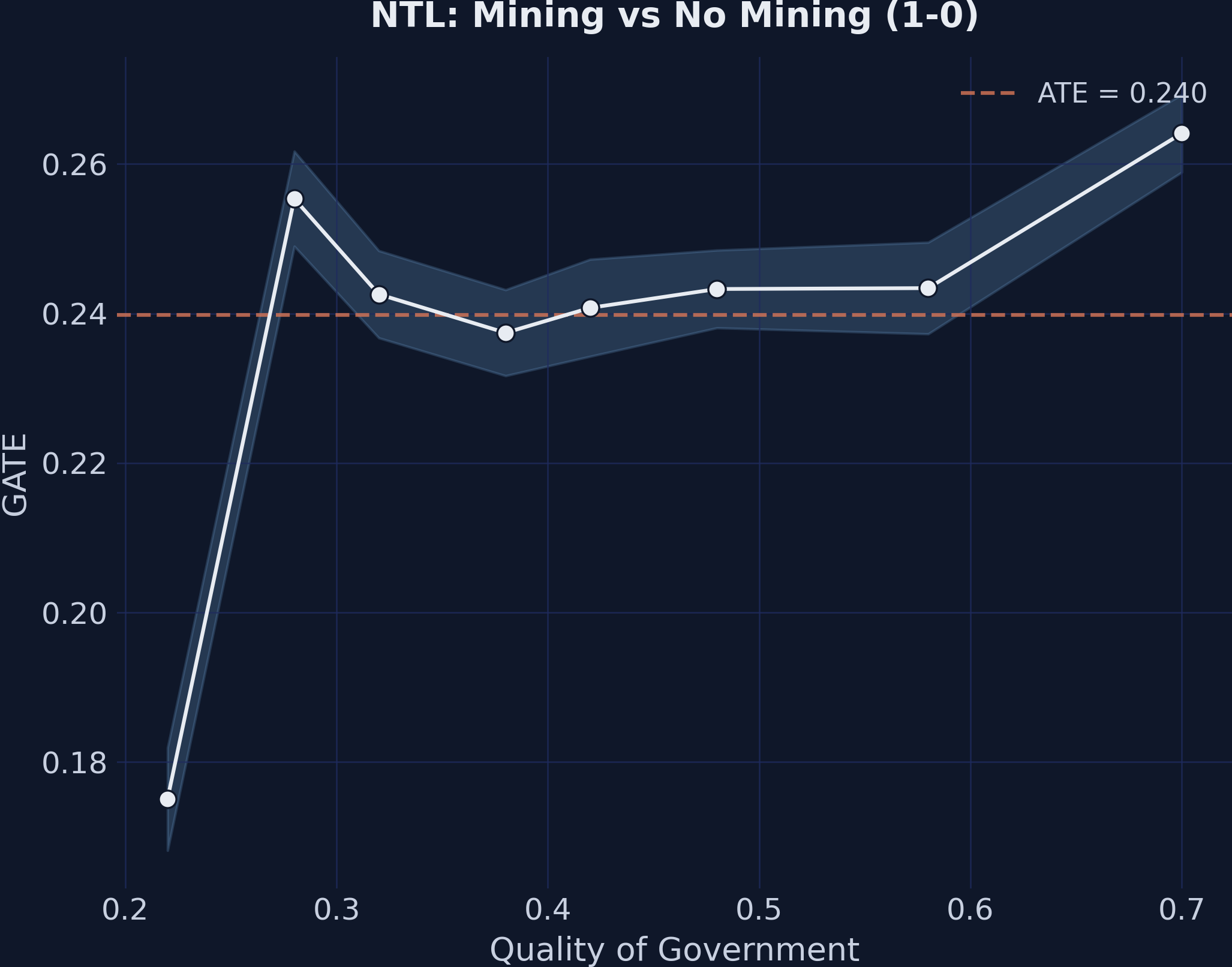

GATEs by Executive Constraints

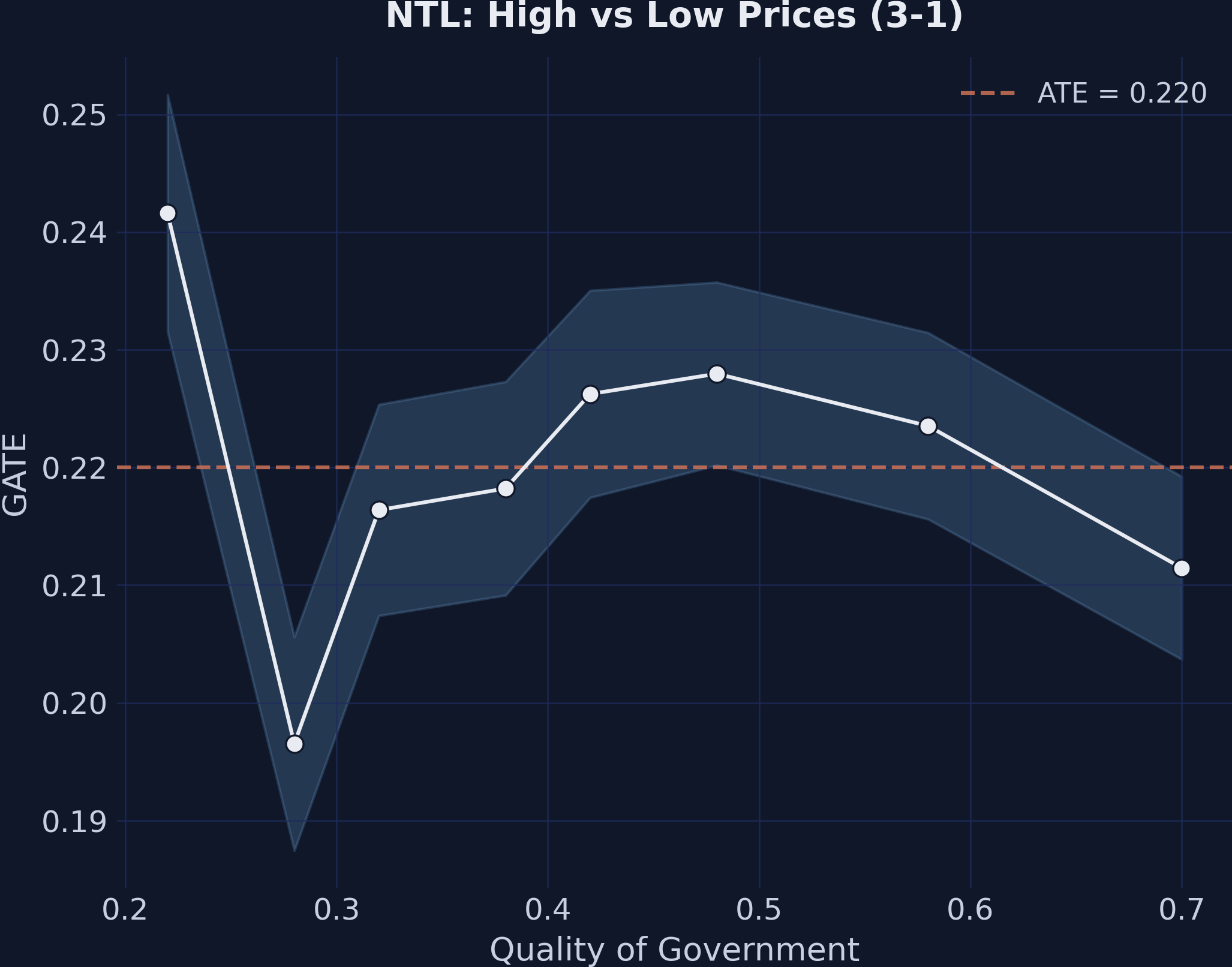

The mining effect (1-0) should vary with institutional quality, while the price effect (3-1) should be flat:

GATEs for the mining effect (1-0) by executive constraints. The upward slope shows that stronger institutions amplify the economic benefits of mining.

GATEs for the mining effect (1-0) by executive constraints. The upward slope shows that stronger institutions amplify the economic benefits of mining.

GATEs for the price effect (3-1) by executive constraints. The flat pattern confirms that institutions do not moderate price effects.

GATEs for the price effect (3-1) by executive constraints. The flat pattern confirms that institutions do not moderate price effects.

1-0 (Mining vs No Mining):

Exec. Constr. GATE 90% CI N

----------------------------------------------------

1 0.175 [0.168, 0.182] 300

2 0.255 [0.249, 0.262] 330

3 0.240 [0.236, 0.244] 720

4 0.242 [0.238, 0.246] 780

5 0.243 [0.237, 0.250] 420

6 0.264 [0.259, 0.269] 450

Range: 0.089

3-1 (High vs Low Prices):

Exec. Constr. GATE 90% CI N

----------------------------------------------------

1 0.242 [0.232, 0.252] 300

2 0.197 [0.187, 0.206] 330

3 0.217 [0.211, 0.224] 720

4 0.227 [0.221, 0.233] 780

5 0.224 [0.216, 0.231] 420

6 0.211 [0.204, 0.219] 450

Range: 0.045

Finding 3: Institutions moderate the mining margin but not the price margin. The mining-effect GATEs (1-0) span a range of 0.089 across executive-constraint levels, climbing roughly monotonically from 0.175 at the weakest institutions to 0.264 at the strongest. Read substantively: weaker institutions cut the development gain from mining roughly in half. The price-effect GATEs (3-1) span only 0.045 and show no monotone pattern — a non-finding that is itself the finding. The GATE plot effectively flat-lines because the price step is, by construction, uniform across institutional environments in the DGP.

This asymmetry — institutions shaping the mining-vs-no-mining margin but not the price margin — is the structural prediction of the institutions-and-resources literature (Mehlum, Moene & Torvik, 2006) and the empirical pattern Hodler, Lechner & Raschky (2023) document for Sub-Saharan African districts. A causal forest does not assume the asymmetry; it discovers it. That is the distinguishing payoff of letting the slope $\tau(\mathbf{x})$ be a flexible function rather than fixing it parametrically (e.g., a single $\tau \times \mathrm{exec\_constraints}$ interaction term).

GATEs by Quality of Government

The same pattern appears when we use a continuous institutional measure:

GATEs for the mining effect (1-0) by quality of government. The positive relationship cross-validates the executive constraints finding.

GATEs for the mining effect (1-0) by quality of government. The positive relationship cross-validates the executive constraints finding.

GATEs for the price effect (3-1) by quality of government. The flat pattern is consistent across institutional measures.

GATEs for the price effect (3-1) by quality of government. The flat pattern is consistent across institutional measures.

The mining effect (1-0) shows a positive relationship with quality of government, while the price effect (3-1) remains approximately flat across the institutional quality distribution. This cross-validates Finding 3 using a different institutional measure.

Variable importance

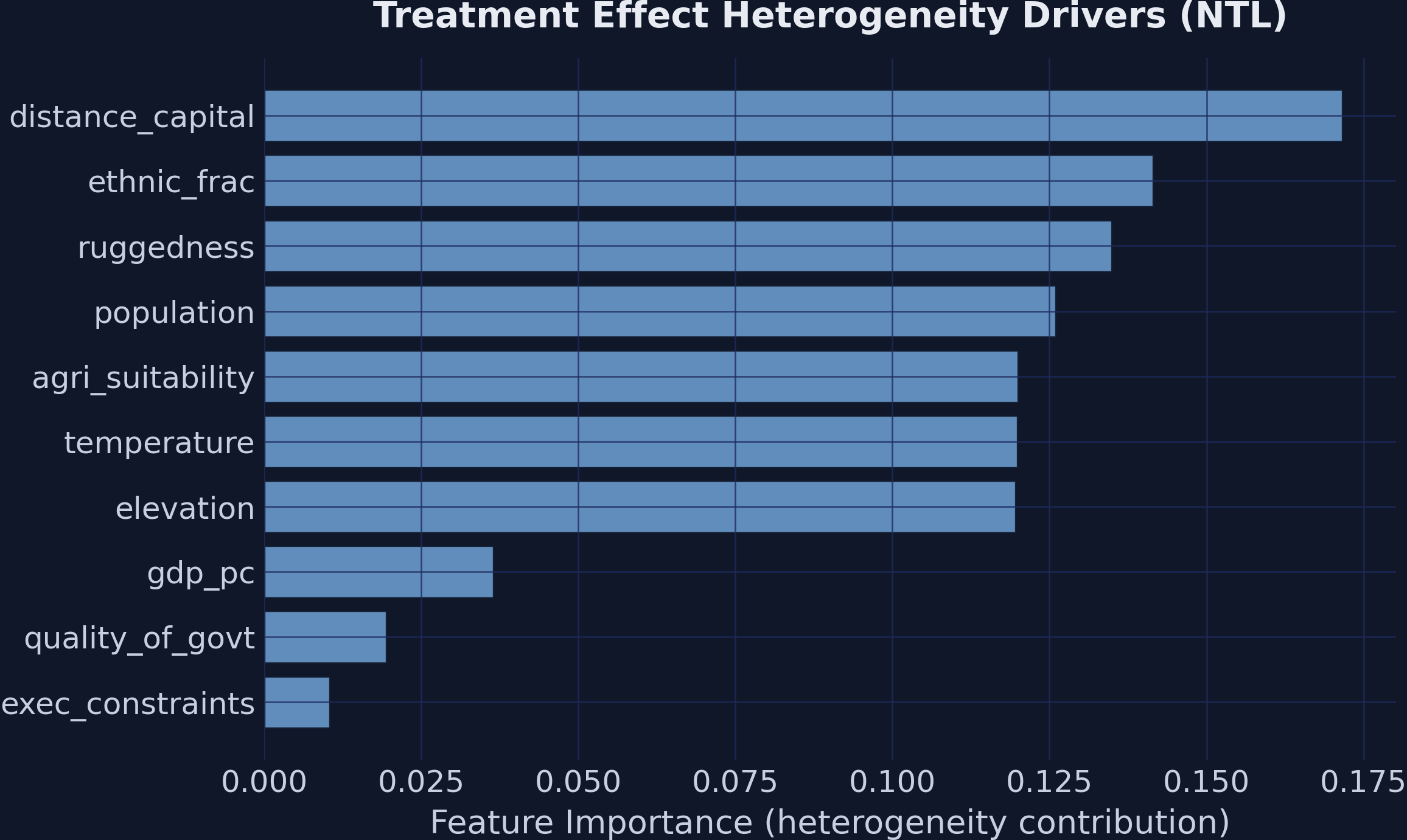

EconML reports feature_importances_ for the causal forest — the normalized contribution of each $X$-variable to treatment-effect heterogeneity across all splits in all trees:

importances = est_ntl.feature_importances_

distance_capital 0.171

ethnic_frac 0.142

ruggedness 0.135

population 0.126

agri_suitability 0.120

elevation 0.120

temperature 0.120

gdp_pc 0.034

quality_of_govt 0.018

exec_constraints 0.014

Feature importance for treatment effect heterogeneity. Geographic variables dominate splitting frequency, but the GATE plots show that institutional variables are the true moderators in the DGP.

Feature importance for treatment effect heterogeneity. Geographic variables dominate splitting frequency, but the GATE plots show that institutional variables are the true moderators in the DGP.

This ranking looks paradoxical: the GATE plots above just demonstrated that exec_constraints is what bends the mining effect, yet exec_constraints is dead last by importance. The resolution is that feature importance and moderation are different objects.

A variable $X_j$ is a moderator of the treatment effect if changing it changes the effect:

$$\frac{\partial \tau(\mathbf{x})}{\partial x_j} \neq 0.$$

A variable’s forest importance, by contrast, is the variance-reduction-weighted frequency with which it is selected as a split variable. The two diverge in a predictable way:

- Continuous variables (e.g.,

distance_capital,ethnic_frac) admit many candidate split thresholds and tend to be picked frequently for fine-grained slicing, even when each individual split contributes only a tiny amount to actual heterogeneity. - Coarse discrete variables like

exec_constraints(6 levels) have at most 5 candidate splits. Even when one of those splits captures the dominant moderation pattern, the variable accumulates a smaller total importance than a continuous neighbor that splits 50 times.

Read importances as a screening signal — a “where might heterogeneity be hiding?” first pass. Confirm or reject moderation with a hypothesis-driven GATE, a partial-dependence plot of $\tau(\mathbf{x})$, or the CATE Interpreter described next. The GATE analysis above is what nails the institutional-moderation finding; the importance ranking is what would have made you suspicious enough to draw the GATE plot in the first place.

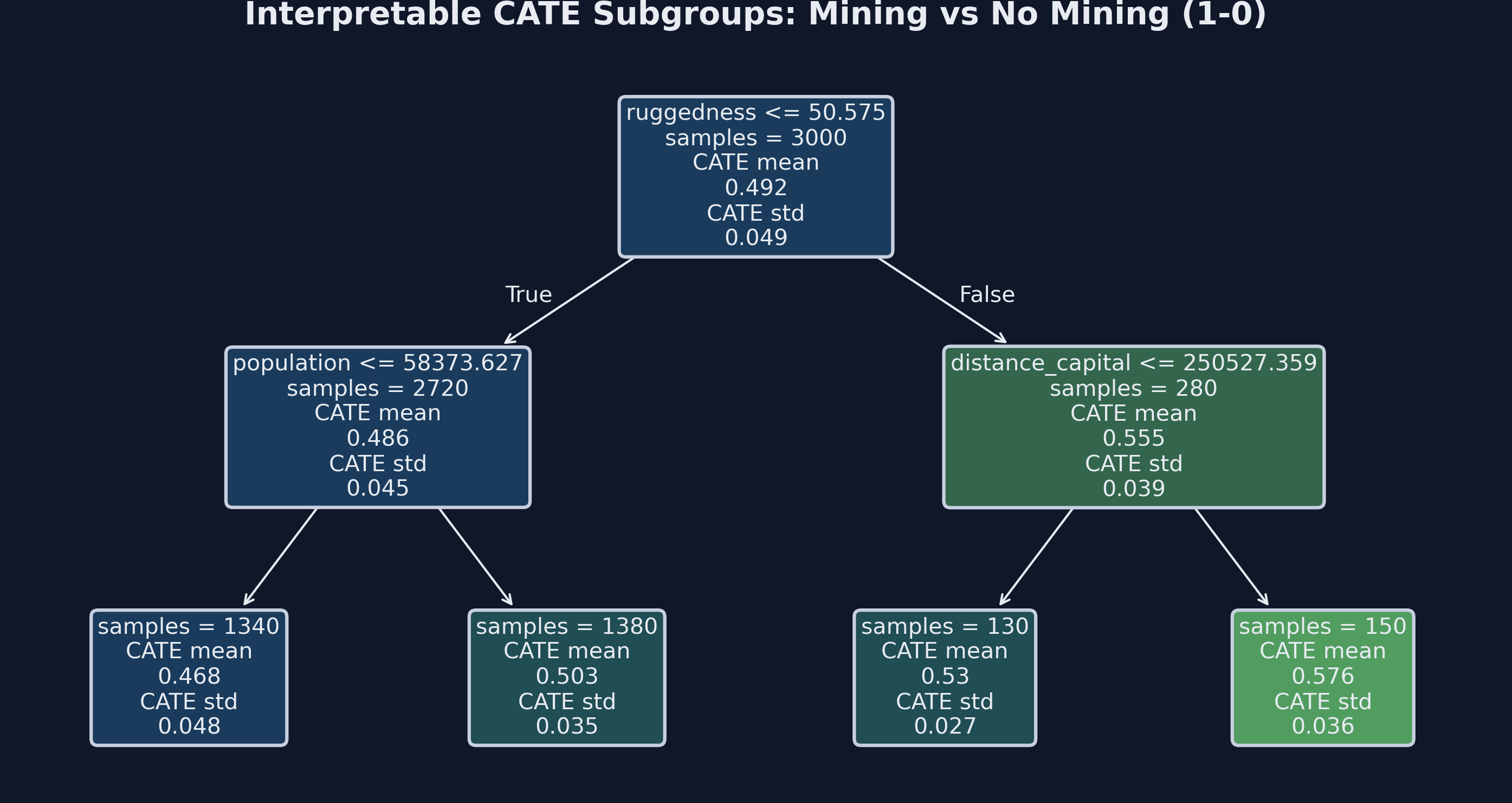

CATE Interpreter

EconML’s SingleTreeCateInterpreter fits a shallow decision tree to the estimated CATEs themselves — the tree’s outcome is the model’s prediction $\widehat\tau(\mathbf{X}_i)$, not the original $Y_i$. By splitting on $\mathbf{X}$, the tree finds the covariates and thresholds that best separate units with different treatment effects, returning a small set of subgroups summarized by their average $\widehat\tau$. It is a summary of the forest’s heterogeneity surface, not a re-estimation of treatment effects.

from econml.cate_interpreter import SingleTreeCateInterpreter

intrp = SingleTreeCateInterpreter(max_depth=2, min_samples_leaf=100)

intrp.interpret(est_ntl, X)

intrp.plot(feature_names=X_COLS)

Depth-2 decision tree summarizing CATE heterogeneity for the mining effect (1-0). Each leaf reports the mean estimated CATE for the subgroup defined by the splits above it.

Depth-2 decision tree summarizing CATE heterogeneity for the mining effect (1-0). Each leaf reports the mean estimated CATE for the subgroup defined by the splits above it.

Two design choices control how interpretable the output is. Tree depth trades off detail against communicability: depth 2 produces at most four leaves and a story you can tell out loud; depth 4 or more reveals interaction structure but rarely fits in a paper figure. Minimum leaf size (min_samples_leaf=100) prevents the tree from carving out tiny, noisy subgroups whose CATE estimates are statistically unreliable. We pull both into the named module constants CATE_TREE_DEPTH and CATE_TREE_MIN_LEAF in script.py so the choice is one place to change rather than scattered magic numbers.

The CATE Interpreter is a complement to, not a substitute for, the GATE analysis. GATEs are hypothesis-driven: you pre-specify the moderating variable (here, exec_constraints) and test how the effect varies across its values. The CATE Interpreter is exploratory: it asks “of all the covariates, which ones — at which thresholds — best separate high-effect from low-effect units?” Running both is good practice. If the tree’s top split corresponds to a pre-specified moderator, your theory is reinforced; if the tree finds a different split, you have learned something the theory did not predict and have a candidate for follow-up GATE plots.

Discussion

Limitations

- No clustered standard errors. Clustered SEs allow the residual variance to differ across clusters (here, districts) and absorb arbitrary within-cluster correlation. EconML’s

inference=Truereports forest-level Bootstrap-of-Little-Bags SEs that treat observations as independent. With panel data — the same district appearing in multiple years — the BLB SEs are likely too small. We useGroupKFoldby district to prevent first-stage data leakage, but that is a different problem from second-stage variance estimation. The companion Stata tutorial uses Stata 19’scatecommand, which supportsvce(cluster district_id)directly. - Contemporaneous outcomes. Hodler, Lechner & Raschky (2023) use treatment at time $t$ and outcome at $t+1$, which rules out reverse causality from outcome to treatment within the same year. Our simulated data uses contemporaneous treatment and outcomes; in real applications, lagging the outcome is cheap insurance.

- Simplified covariate set. The real analysis uses 60+ covariates spanning geology, geography, demography, institutions, and pre-treatment outcomes; we use 12. The simulated DGP guarantees that the CIA holds because we control for every confounder we built in. Real-world identification is only as strong as the controls support, and “we used a causal forest” does not relax the CIA.

Assumptions

The CATE estimates rely on the Conditional Independence Assumption: treatment is independent of potential outcomes given $(X, W)$. The CIA is untestable from data alone — it asserts something about the unobserved potential outcomes. In observational work, the standard defense is a combination of (i) institutional knowledge of the treatment-assignment process, (ii) a rich, theory-motivated set of covariates, and (iii) sensitivity analyses (e.g., Rosenbaum bounds, $E$-values) that ask how strong an unobserved confounder would have to be to overturn the conclusion. None of these is a substitute for randomization. In the simulated data here, we know the CIA holds because we built it that way.

Summary and next steps

EconML’s

CausalForestDMLrecovered all three ground-truth findings. The ATE for the basic mining effect (1-0 = 0.240) is within sampling error of the true value 0.250 and removes nearly all of the 0.141 confounding bias visible in the naive estimator. Price effects come out non-linear (2-1 = 0.029, n.s.; 3-1 = 0.220, significant at 5%; 3-2 = 0.191, significant at 10%) without any pre-specified non-linearity. GATE patterns reveal that institutions moderate the mining effect (range = 0.089 across executive-constraint levels) but not the price effect (range = 0.045, no monotone pattern).The DML two-stage residualization argument is what makes the causal forest valid in observational settings. Substituting the treatment equation into the outcome equation reduces causal estimation to a regression of $\tilde Y$ on $\tilde T$, where the residualizers $\hat g_0$ and $\hat m_0$ can be any flexible learner. Neyman orthogonality means errors in the residualizers enter only at second order, so $\sqrt n$-consistent estimates of $\tau$ are recoverable even with $O(n^{-1/4})$ first-stage rates.

Feature importance is a screening tool, not a moderation test. Continuous variables accumulate importance because they offer many split points, even when they do not bend the treatment effect. The GATE plot of $\tau$ against the suspected moderator is the right tool for confirming moderation; importance is the right tool for identifying candidates worth plotting.

The CATE Interpreter is the exploratory dual of GATEs. A shallow decision tree on the predicted CATEs surfaces data-driven subgroups, complementing the hypothesis-driven GATE analysis. Use both: GATEs test theory, the interpreter audits theory.

For the economic story behind these findings and a parallel implementation using Stata 19’s built-in cate command, see the companion tutorial: Causal Machine Learning and the Resource Curse with Stata 19.

Exercises

Replace the nuisance models. Swap

GradientBoostingRegressorwithRandomForestRegressor(n_estimators=200). Do the ATE and GATE estimates change? Why or why not (think about Neyman orthogonality)?Vary the number of trees. Try

n_estimators=100vsn_estimators=1000. How do the standard errors and GATE patterns change?Test the GroupKFold assumption. Remove

groups=df['district_id'].valuesfrom thefit()call. What happens to the confidence intervals?Discretize quality of government. Create quartiles of

quality_of_govtand compute GATEs on the quartiles instead of raw values. Do the patterns become clearer?Explore the CATE interpreter depth. Increase

max_depthfrom 2 to 4 inSingleTreeCateInterpreter. Do the additional splits reveal meaningful subgroups or just noise?

References

- Hodler, R., Lechner, M., & Raschky, P.A. (2023). Institutions and the resource curse: New insights from causal machine learning. PLoS ONE, 18(6), e0284968.

- Chernozhukov, V., Chetverikov, D., Demirer, M., Duflo, E., Hansen, C., Newey, W., & Robins, J. (2018). Double/Debiased Machine Learning for Treatment and Structural Parameters. The Econometrics Journal, 21(1), C1–C68.

- Athey, S., Tibshirani, J., & Wager, S. (2019). Generalized Random Forests. The Annals of Statistics, 47(2), 1148–1178.

- Wager, S. & Athey, S. (2018). Estimation and Inference of Heterogeneous Treatment Effects using Random Forests. Journal of the American Statistical Association, 113(523), 1228–1242.

- Robinson, P.M. (1988). Root-N-Consistent Semiparametric Regression. Econometrica, 56(4), 931–954.

- Rubin, D.B. (1974). Estimating causal effects of treatments in randomized and nonrandomized studies. Journal of Educational Psychology, 66(5), 688–701.

- Imbens, G.W. & Rubin, D.B. (2015). Causal Inference for Statistics, Social, and Biomedical Sciences. Cambridge University Press.

- Sachs, J.D. & Warner, A.M. (1995). Natural Resource Abundance and Economic Growth. NBER Working Paper No. 5398.

- Mehlum, H., Moene, K., & Torvik, R. (2006). Institutions and the Resource Curse. The Economic Journal, 116(508), 1–20.

- EconML Documentation — PyWhy

Carlos Mendez

Associate Professor of Development Economics

My research interests focus on the integration of development economics, spatial data science, and econometrics to better understand and inform the process of sustainable development across regions.