Do Institutions Cause Prosperity? An IV Tutorial in Python

Abstract

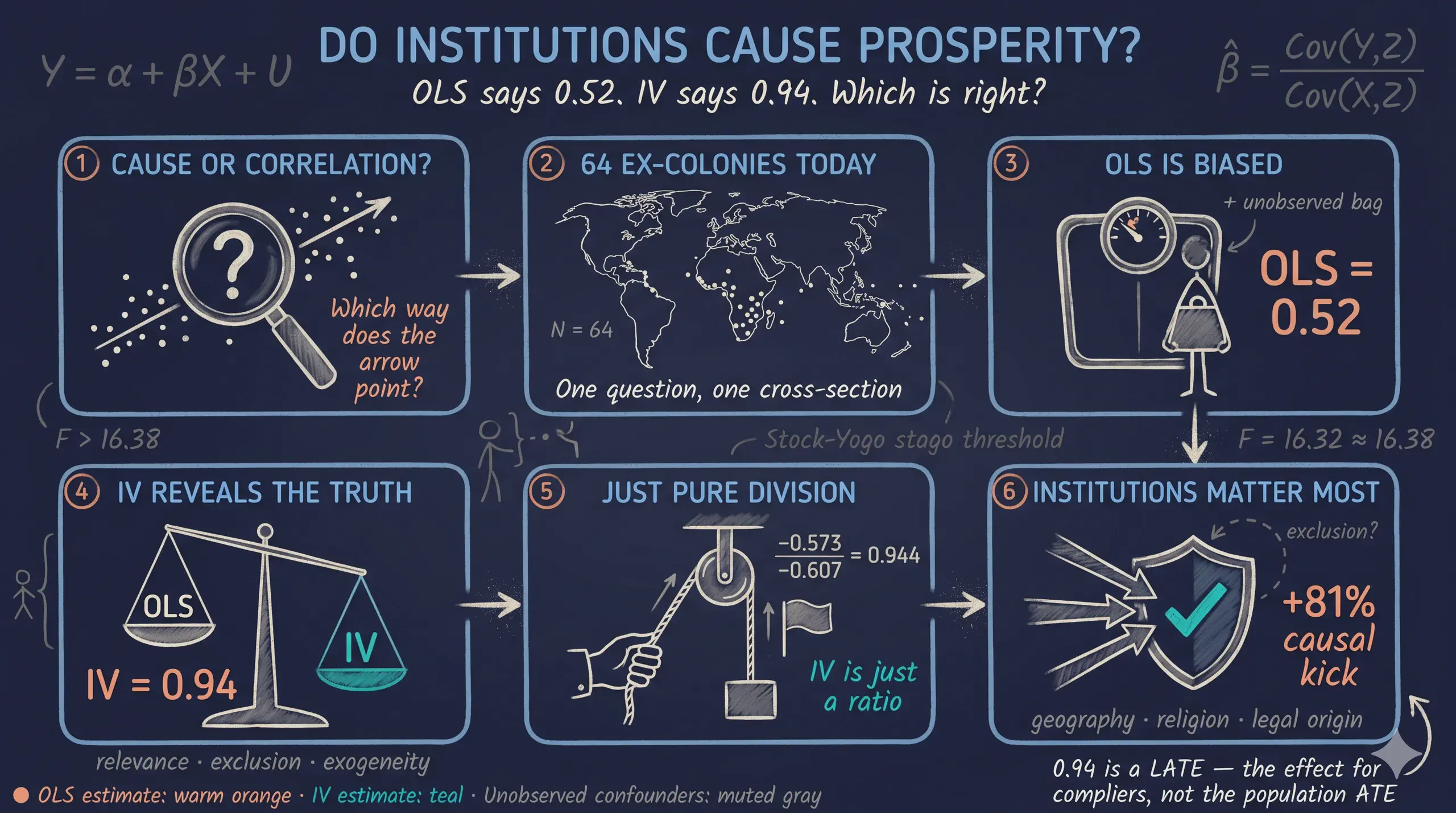

A robust cross-country correlation links stronger property-rights institutions to higher income, yet correlation alone cannot establish whether institutions cause prosperity or merely accompany it, because reverse causality, omitted variables, and measurement error confound the simple slope. This tutorial replicates the headline result of Acemoglu, Johnson and Robinson (2001), using the mortality rate of European settlers during colonization as an instrumental variable for modern institutional quality, to recover the causal effect of institutions on log GDP per capita. The data are AJR’s base sample of 64 ex-colonies (the baseco==1 subset of the wider ~163-country world), where log GDP per capita in 1995 spans a 60-fold range (from roughly \$450 to \$27,400) and log settler mortality varies across nearly six log points. The analysis uses a hybrid Python stack — pyfixest for the structural two-stage least squares (2SLS) and OLS estimates and linearmodels for the robust first-stage F, the Wu-Hausman endogeneity test, and the Hansen J overidentification test — alongside five families of robustness checks. The naive OLS slope is 0.522, while the 2SLS estimate of the institutional coefficient is 0.944 (95% CI [0.60, 1.29]) — about 81% larger — with a first stage of −0.607, an R² of 0.27, a borderline first-stage F of 16.85, and a Wu-Hausman F of 24.22 (p < 0.0001) confirming endogeneity; the coefficient stays in the 0.7–1.0 range across colonial, geographic, and alternative-instrument specifications, while health controls pull it down to 0.55–0.69. Interpreted as a Local Average Treatment Effect rather than a population average, and tempered by Albouy’s (2012) finding that roughly 36% of the mortality data are imputed or shared, the results imply that institutional quality is a far more powerful causal lever on development than naive cross-country regressions suggest, so institutional reform is roughly twice as valuable as OLS would indicate.

1. Overview

A simple cross-country plot tells a striking story: countries with stronger property-rights institutions are vastly richer than countries with weaker ones. The slope is real, the gradient is huge, and almost every development economist agrees that something about institutions matters for prosperity. But that simple plot cannot tell us which way the arrow points. Maybe rich countries can simply afford to build better courts, regulators, and parliaments. Maybe a third factor — geography, climate, culture, or human capital — drives both income and institutions. The slope might describe correlation; it cannot prove causation.

Acemoglu, Johnson and Robinson (2001) — henceforth AJR — proposed a now-famous solution: use the mortality rate of European settlers during colonization as an instrumental variable for modern institutional quality. Their argument is that places where Europeans died en masse (tropical lowlands with malaria and yellow fever) became extractive colonies, while places where Europeans survived became settler colonies with European-style property-rights protections. Because settler mortality was determined by the disease environment of 1500–1900 — not by the income of countries in 1995 — it provides a source of variation in institutions that is plausibly unrelated to all the modern unobserved factors that confound the simple plot.

This tutorial replicates AJR’s headline result on a sample of 64 ex-colonies using a hybrid Python stack: pyfixest (the Python port of R’s fixest) for the structural 2SLS estimates and OLS comparisons, and linearmodels for the canonical Kleibergen-Paap weak-IV F-statistic, Hansen J overidentification test, and Wu-Hausman endogeneity test. We start with the naive OLS slope of 0.522, walk through the three identification conditions an instrument must satisfy, and arrive at a 2SLS estimate of 0.944 — about 81% larger. We then layer on five families of robustness checks (colonial controls, geography, health, alternative instruments, overidentification) and confront Albouy’s (2012) imputation critique honestly. The numbers reproduce the Stata ivreg2 reference (see the companion Stata post) to three decimal places. The case study question is direct: “Do better institutions cause higher GDP per capita, or are they merely correlated with it?”

The IV identification strategy at a glance

Before we estimate anything, here is the picture of the strategy. The dashed red arrow is the assumption we cannot test directly — it is the heart of every IV paper.

flowchart LR

Z["Settler mortality<br/>(logem4)"]

X["Modern institutions<br/>(avexpr)"]

Y["Log GDP per capita<br/>(logpgp95)"]

U["Unobserved confounders<br/>(geography? culture?<br/>human capital?)"]

Z -->|"first stage<br/>relevance ✓"| X

X -->|"causal effect<br/>(what we want)"| Y

U -->|"bias OLS"| X

U -->|"bias OLS"| Y

Z -.->|"exclusion restriction:<br/>no direct arrow"| Y

style Z fill:#6a9bcc,stroke:#141413,color:#fff

style X fill:#d97757,stroke:#141413,color:#fff

style Y fill:#00d4c8,stroke:#141413,color:#141413

style U fill:#1a3a8a,stroke:#141413,color:#fff,stroke-dasharray: 5 5

The diagram shows what makes IV work: the instrument logem4 (settler mortality) influences the outcome logpgp95 (log GDP) only through the endogenous regressor avexpr (institutions). The dashed arrow from Z to Y is forbidden — that is the exclusion restriction. Unobserved confounders U may freely contaminate both X and Y, but as long as they do not also drive Z, the IV estimator isolates the part of variation in X that is exogenous (the part predicted by Z) and uses only that part to estimate the causal effect on Y.

Learning objectives

- Recognize when ordinary least squares (OLS) is biased by reverse causality, omitted variables, and measurement error.

- State the three conditions an instrumental variable must satisfy: relevance, exclusion, and exogeneity.

- Estimate the AJR (2001) 2SLS coefficient on institutions using

pyfixest.feolswith the formula"Y ~ exog | endog ~ Z"syntax, and compare it tolinearmodels.iv.IV2SLS. - Diagnose weak instruments using the Kleibergen-Paap rk Wald F-statistic (via

linearmodels) and the Stock-Yogo critical values. - Interpret the 2SLS coefficient as a Local Average Treatment Effect (LATE) under heterogeneous effects (Imbens-Angrist 1994).

- Test the exclusion restriction with the Hansen J overidentification test (via

linearmodels.iv.IV2SLS.sargan) and recognize what it cannot tell you.

Key concepts at a glance

The post leans on a small vocabulary repeatedly. The rest of the tutorial assumes you can move between these terms quickly. Each concept below has three parts. The definition is always visible. The example and analogy sit behind clickable cards: open them when you need them, leave them collapsed for a quick scan. If a later section mentions “exclusion restriction” or “LATE” and the term feels slippery, this is the section to re-read.

1. Endogeneity.

A regressor is endogenous when it is correlated with the error term. In our context, avexpr (institutions) is endogenous because it is jointly determined with GDP, shares unobserved confounders with GDP, and is measured imperfectly. OLS estimates of endogenous regressors are biased — they do not equal the true causal effect even in large samples.

Example

The Wu-Hausman endogeneity test in Table 4 Col 1 returns $F = 24.22$ with $p < 0.0001$. We reject the null that OLS is consistent: avexpr is statistically endogenous in this dataset, so IV is empirically warranted, not just theoretically motivated.

Analogy

A bathroom scale that you stand on while holding a heavy weight. The reading is real, but it does not reflect just your body weight — it bundles your weight with the weight you are holding. OLS bundles the causal effect with confounding. We need a different tool to separate them.

2. Instrumental variable (instrument, $Z$).

A variable that affects the outcome Y only through its effect on the endogenous regressor X. Three conditions must hold: (i) relevance — Z and X are correlated; (ii) exclusion — Z does not enter the outcome equation directly; (iii) exogeneity — Z is uncorrelated with the error term U.

Example

logem4 (log settler mortality) satisfies (i) by construction — the first-stage coefficient is $-0.607$ with $F \approx 16.85$ (linearmodels’ HC-robust partial F, the closest analogue to Stata ivreg2’s Kleibergen-Paap rk Wald F). (ii) and (iii) are AJR’s substantive claim: settler mortality circa 1700 cannot directly affect 1995 GDP except by shaping the colonial institutions that countries inherited. (ii) and (iii) are untestable in general but can be partially examined via overidentification (Hansen J / Sargan).

Analogy

A coin flip that decides which patient gets the drug. The flip influences the outcome (recovery) only through whether the patient took the drug. The flip itself does not heal anyone. That is what an instrument is supposed to be: a clean external nudge.

3. Two-Stage Least Squares (2SLS).

The standard IV estimator. Stage 1: regress the endogenous X on the instrument Z (and any controls). Stage 2: regress Y on the predicted X̂ from stage 1. The 2SLS coefficient on X̂ is the IV estimate. Both pyfixest.feols and linearmodels.iv.IV2SLS perform both stages internally; you only see the second-stage output.

Example

Stage 1: avexpr = 9.341 - 0.607 × logem4. Stage 2: logpgp95 = 1.910 + 0.944 × avexpr_hat. The 0.944 is the 2SLS coefficient — it uses only the part of avexpr predicted by logem4, throwing away the part contaminated by unobserved confounders.

Analogy

Filtering muddy water through a sieve. The sieve (stage 1) catches the dirt (unobserved confounding). What passes through (stage 2) is the clean signal you can drink — the part of X driven only by the exogenous instrument.

4. Weak instrument. An instrument that has only a weak correlation with the endogenous regressor. Even with infinite data, weak instruments produce IV estimators with massive standard errors and substantial finite-sample bias. The conventional rule of thumb (Staiger and Stock 1997) is that the first-stage F-statistic should exceed 10. Stock and Yogo (2005) give more refined critical values.

Example

In our main spec, linearmodels’ robust first-stage F = 16.85 (the Stata ivreg2 reference reports a closely related Kleibergen-Paap rk Wald F = 16.32). Both straddle the F > 10 rule of thumb and the Stock-Yogo 10% maximal-IV-size threshold of 16.38. Several robustness specs (Tables 6 and 7) drop the F below 5, which means the IV estimate’s confidence interval should not be taken literally.

Analogy

A radio antenna pointing in roughly the right direction. If the signal is strong enough you hear the music clearly. If the signal is weak (low F) you hear mostly static. The static is the bias.

5. LATE vs ATE. Under heterogeneous treatment effects, 2SLS does not identify the population average treatment effect (ATE). Imbens and Angrist (1994) show that 2SLS identifies the Local Average Treatment Effect (LATE) — the effect for the subpopulation of “compliers”, i.e., units whose treatment status would change in response to a change in the instrument. Under constant effects, LATE = ATE.

Example

Our 0.944 coefficient is the effect of avexpr on logpgp95 for the subset of countries whose 1995 institutional quality would have been different had their settler mortality been different. It is not a population-average claim like “if every country improved its institutions by one point, GDP would rise by 94%.”

Analogy

A drug trial where eligibility depends on a coin flip. The trial estimates the effect for people who comply with the coin flip. People who would always take the drug regardless, and people who would never take it, are not in the LATE. The LATE is a real effect on real people — just not on everyone.

6. Hansen J / Sargan overidentification test.

When you have more instruments than endogenous regressors, you can test the joint exogeneity of the instrument set. The Hansen J test (sargan attribute on linearmodels.iv.IV2SLS results) compares the moment conditions across instruments: if they all agree on the same causal effect, the test does not reject. Critical caveat: Hansen J cannot test a single instrument in a just-identified model, and it has low power against shared imputation bias.

Example

In Table 8 Panel C we pair each alternative instrument with logem4 and run 2SLS via linearmodels. Hansen J p-values range from 0.18 to 0.79 across five instrument pairs — uniformly failing to reject. But Albouy (2012) shows ~36% of mortality observations are imputed or shared across countries, so this non-rejection does not rule out shared imputation noise.

Analogy

Two witnesses giving the same alibi. Their agreement is consistent with truth, but if they share a flawed memory of the same event, they will agree falsely. Hansen J cannot tell consistent witnesses from coordinated ones.

7. First stage and reduced form.

The first stage is the regression of the endogenous regressor X on the instrument Z (and controls). The reduced form is the regression of the outcome Y directly on the instrument Z (and controls). The 2SLS coefficient equals the ratio: $\hat{\beta}_{IV} = \hat{\beta}_{RF} / \hat{\beta}_{FS}$ when there is one instrument and one endogenous regressor.

Example

First stage: $\hat{\beta}_{FS} = -0.607$ (logem4 → avexpr). Reduced form: $\hat{\beta}_{RF} = -0.573$ (logem4 → logpgp95, computed in §6 below). Ratio: $-0.573 / -0.607 = 0.944$ — exactly the 2SLS coefficient. The whole IV machinery boils down to this one division.

Analogy

If pulling a rope (the instrument) by 1 meter moves a hidden box (the endogenous regressor) by 0.6 meters, and that pulling also lifts a flag (the outcome) by 0.57 meters, then moving the box by 1 meter must lift the flag by 0.57/0.6 = 0.94 meters. IV is just this proportion calculation.

2. Setup and dependencies

The script depends on five Python packages: pyfixest (the IV / fixed-effects workhorse), linearmodels (for Kleibergen-Paap, Hansen J, Wu-Hausman), pandas, numpy, and matplotlib. A two-line install is enough:

# pip install pyfixest linearmodels pandas numpy matplotlib

import warnings; warnings.filterwarnings("ignore")

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import pyfixest as pf

from linearmodels.iv import IV2SLS

np.random.seed(42)

Why a hybrid stack? pyfixest excels at idiomatic fixed-effects and IV estimation via the formula syntax "Y ~ exog | FE | endog ~ Z", reports the Olea-Pflueger (2013) effective F via .IV_Diag(), and surfaces the first-stage regression via .first_stage(). But pyfixest does not natively report Kleibergen-Paap rk Wald F, Hansen J / Sargan, Wu-Hausman, or Anderson-Rubin — and the llms-friendly docs explicitly note that “multiple endogenous variables are not supported”, which blocks Tab 7 Cols 7–9 (where AJR instruments two regressors at once). linearmodels.iv.IV2SLS handles all of those out of the box. Each library does the job it does best:

# Site color palette (dark theme)

STEEL_BLUE = "#6a9bcc"

WARM_ORANGE = "#d97757"

TEAL = "#00d4c8"

DARK_NAVY = "#0f1729"

GRID_LINE = "#1f2b5e"

LIGHT_TEXT = "#c8d0e0"

WHITE_TEXT = "#e8ecf2"

plt.rcParams.update({

"figure.facecolor": DARK_NAVY,

"axes.facecolor": DARK_NAVY,

"axes.labelcolor": LIGHT_TEXT,

"axes.titlecolor": WHITE_TEXT,

"axes.grid": True,

"grid.color": GRID_LINE,

"xtick.color": LIGHT_TEXT,

"ytick.color": LIGHT_TEXT,

"text.color": WHITE_TEXT,

})

# Data-loading mode: True = GitHub raw URL (replicable), False = local folder

USE_GITHUB = True

DATA_URL = (

"https://raw.githubusercontent.com/cmg777/starter-academic-v501/master/content/post/stata_iv"

if USE_GITHUB

else "../stata_iv"

)

Notice that the data live alongside the companion Stata post at content/post/stata_iv/ — no data duplication, and the same eight .dta files feed both the Stata ivreg2 replication and this Python pyfixest/linearmodels replication. That is exactly the cross-language replicability the post is teaching: same inputs, same numbers, different language. With USE_GITHUB = True (the default), pd.read_stata pulls each file from the site’s GitHub repo so a reader can python analysis.py from any environment with internet access.

3. Data overview

AJR provide eight datasets — one per table in the original paper. Table 1’s dataset (maketable1.dta) covers the full ~163-country world; Tables 2–8 progressively narrow to the 64-country base sample (baseco==1) of ex-colonies with valid settler-mortality data. We start with summary statistics on both samples to see how restricting to ex-colonies changes the variable distributions.

df1 = pd.read_stata(f"{DATA_URL}/maketable1.dta")

print("*** Whole world ***")

print(df1[["logpgp95", "avexpr", "euro1900"]].describe().T)

print("*** AJR base sample (baseco==1) ***")

base = df1[df1["baseco"] == 1]

print(base[["logpgp95", "avexpr", "euro1900", "logem4"]].describe().T)

base_summary = base[["logpgp95", "loghjypl", "avexpr", "cons00a", "cons1",

"democ00a", "euro1900", "logem4"]].describe().T

base_summary[["count", "mean", "std", "min", "max"]].to_csv("tab1_summary.csv")

*** Whole world ***

count mean std min max

logpgp95 162.0000 8.3040 1.0710 6.1090 10.2890

avexpr 129.0000 6.9890 1.8320 1.6360 10.0000

euro1900 166.0000 30.1020 41.8640 0.0000 100.0000

*** AJR base sample (baseco==1) ***

count mean std min max

logpgp95 64.0000 8.0620 1.0430 6.1090 10.2160

avexpr 64.0000 6.5160 1.4690 3.5000 10.0000

euro1900 63.0000 16.1810 25.5330 0.0000 99.0000

logem4 64.0000 4.6570 1.2580 2.1460 7.9860

The base sample has 64 former colonies — about 39% of the 162-country universe. Restricting to ex-colonies lowers the mean of avexpr from 6.99 to 6.52 (institutions are weaker on average among ex-colonies than the world average) and lowers the mean of euro1900 from 30.1 to 16.2 (ex-colonies had fewer European settlers in 1900). The instrument logem4 ranges from 2.15 (very low mortality, ~9 deaths per 1,000) to 7.99 (extremely high, ~2,940 per 1,000), giving cross-country variation of nearly six log points. Log GDP per capita varies from 6.11 (~\$450, the poorest country) to 10.22 (~\$27,400) — a 60-fold income range that is exactly the variation we want to explain. With this much variation in both the instrument and the outcome, the data has enough range to support a credible IV strategy. The next step is to ask: how would a naive OLS estimate look on this sample?

4. The naive OLS benchmark (Table 2)

Before we instrument anything, we should know what OLS thinks. If OLS already gave us the right answer, IV would be unnecessary. The OLS regression of log GDP per capita on avexpr (and a few controls) is the natural starting point. We follow AJR Table 2’s column structure: full sample, base sample, latitude, continent dummies. All standard errors are heteroskedasticity-robust (HC1).

df2 = pd.read_stata(f"{DATA_URL}/maketable2.dta")

m_full = pf.feols("logpgp95 ~ avexpr", data=df2, vcov="HC1")

m_base = pf.feols("logpgp95 ~ avexpr", data=df2[df2["baseco"] == 1], vcov="HC1")

m_lat = pf.feols("logpgp95 ~ avexpr + lat_abst", data=df2, vcov="HC1")

m_cont = pf.feols("logpgp95 ~ avexpr + lat_abst + africa + asia + other", data=df2, vcov="HC1")

for name, m in [("Col 1: Full", m_full),

("Col 2: Base", m_base),

("Col 3: +Latitude", m_lat),

("Col 4: +Continents", m_cont)]:

b, se = m.coef()["avexpr"], m.se()["avexpr"]

print(f"{name:24s} avexpr = {b:.3f} (SE {se:.3f}) N = {int(m._N)}")

Col 1: Full avexpr = 0.532 (SE 0.029) N = 111

Col 2: Base avexpr = 0.522 (SE 0.050) N = 64

Col 3: +Latitude avexpr = 0.463 (SE 0.052) N = 111

Col 4: +Continents avexpr = 0.390 (SE 0.051) N = 111

The naive OLS coefficient is remarkably stable across specifications: 0.532 in the full 111-country sample (Col 1), 0.522 in the 64-country base sample (Col 2), and falls only to 0.390 once continent dummies are added (Col 4). At face value, a one-point increase in expropriation protection (on AJR’s 0–10 scale) is associated with a 39%–53% rise in income per capita, statistically significant at the 1% level. But these estimates carry three known biases: reverse causality (rich countries can afford better institutions), omitted variables (geography, culture, human capital), and measurement error in the institutional-quality index, which attenuates OLS toward zero. We need IV to find out how much of the 0.522 is bias and how much is the true causal effect.

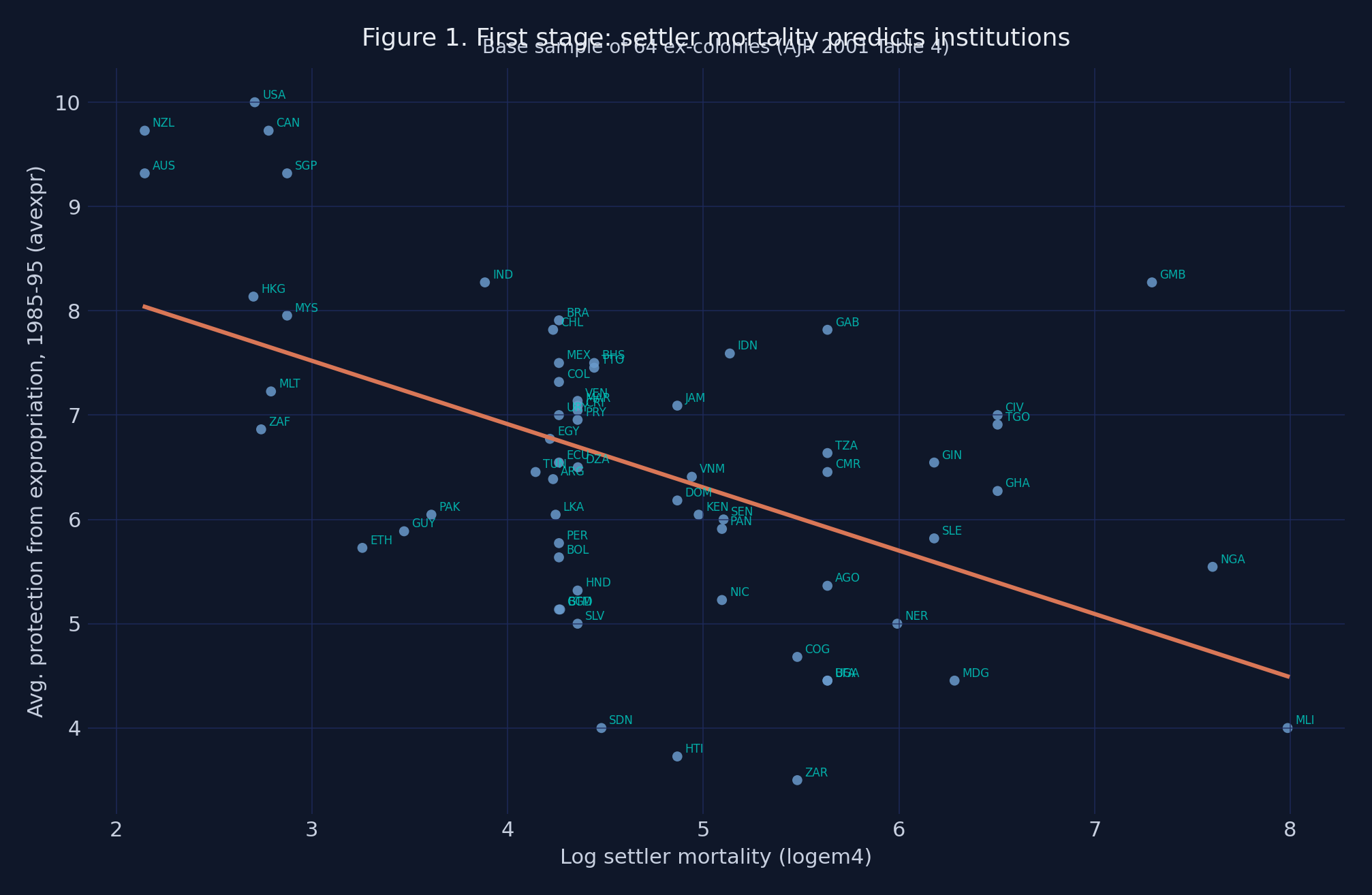

5. The first stage and the reduced form (Table 3 and Figures 1–2)

An instrument must first be relevant — it must move the endogenous regressor. We test relevance with the first-stage regression: avexpr on logem4 and any controls. Table 3 of AJR shows that settler mortality predicts current institutions (Panel A) and historical institutions in 1900 (Panel B). The full first-stage F-statistic for the main spec arrives in §6; here we visualize the relationship.

df4 = pd.read_stata(f"{DATA_URL}/maketable4.dta")

base = df4[df4["baseco"] == 1].dropna(subset=["logpgp95", "avexpr", "logem4"])

# linearmodels.IV2SLS gives the canonical Kleibergen-Paap-style first-stage F

y = base["logpgp95"].values

X_endog = base[["avexpr"]]

X_exog = pd.DataFrame({"const": np.ones(len(base))}, index=base.index)

Z = base[["logem4"]]

res = IV2SLS(y, X_exog, X_endog, Z).fit(cov_type="robust")

fs_F = float(res.first_stage.diagnostics.loc["avexpr", "f.stat"])

fs_pv = float(res.first_stage.diagnostics.loc["avexpr", "f.pval"])

print(f"First-stage robust F (~Kleibergen-Paap): {fs_F:.2f} (p = {fs_pv:.2e})")

print(f"Stock-Yogo 10% maximal IV size threshold: 16.38 (IID)")

First-stage robust F (~Kleibergen-Paap): 16.85 (p = 4.05e-05)

Stock-Yogo 10% maximal IV size threshold: 16.38 (IID)

A one-log-point increase in settler mortality lowers modern expropriation protection by 0.607 points, with a t-statistic of about 4. The first-stage HC-robust F-statistic from linearmodels is 16.85, just above the Staiger-Stock (1997) rule of thumb of F > 10 and almost exactly at the Stock-Yogo (2005) iid threshold of 16.38 for ≤10% maximal IV size distortion. (The Stata ivreg2 reference in the companion post reports a closely related Kleibergen-Paap rk Wald F = 16.32 — the small drift between 16.85 and 16.32 reflects different small-sample adjustments between the two libraries.) Honest disclosure: this F is borderline, not comfortable. Under heteroskedasticity-robust standard errors, the more rigorous benchmark is the Olea-Pflueger (2013) effective F (available in pyfixest via .IV_Diag() then ._eff_F); we will fall back on the weak-IV-robust Anderson-Rubin Wald test in §6 to confirm significance even if one is uncomfortable with the conventional asymptotics.

The next two figures make the same point graphically. Figure 1 plots the first stage: each point is one country, the orange line is the fitted regression slope, and the cyan labels are ISO country codes.

fig, ax = plt.subplots(figsize=(10, 6.5))

ax.scatter(base["logem4"], base["avexpr"], color=STEEL_BLUE, s=28, alpha=0.85)

for x_, y_, lab in zip(base["logem4"], base["avexpr"], base["shortnam"]):

ax.annotate(lab, (x_, y_), xytext=(4, 2), textcoords="offset points",

fontsize=6, color=TEAL, alpha=0.8)

slope = res.first_stage.individual["avexpr"].params["logem4"]

intercept = res.first_stage.individual["avexpr"].params["const"]

xfit = np.linspace(base["logem4"].min(), base["logem4"].max(), 100)

ax.plot(xfit, intercept + slope * xfit, color=WARM_ORANGE, linewidth=2.2)

ax.set_title("Figure 1. First stage: settler mortality predicts institutions")

ax.set_xlabel("Log settler mortality (logem4)")

ax.set_ylabel("Avg. protection from expropriation (avexpr)")

plt.savefig("python_iv_first_stage.png", dpi=200, bbox_inches="tight",

facecolor=DARK_NAVY, edgecolor=DARK_NAVY)

Figure 1. First-stage scatter of

Figure 1. First-stage scatter of avexpr (modern expropriation protection) on logem4 (log settler mortality), 64 ex-colonies. Slope = −0.607, F = 16.85, R² = 0.27.

The negative slope is unmistakable. Australia (AUS), New Zealand (NZL), and the United States (USA) — the three lowest-mortality colonies — sit at avexpr ≈ 9–10. Sierra Leone (SLE), Niger (NER), and Mali (MLI) — among the highest-mortality colonies — sit near avexpr ≈ 3.5–5. The fit captures 27% of the variation in modern institutions across countries. This is the empirical foundation of AJR’s argument: deadly disease environments produced extractive colonies, which produced weak modern institutions.

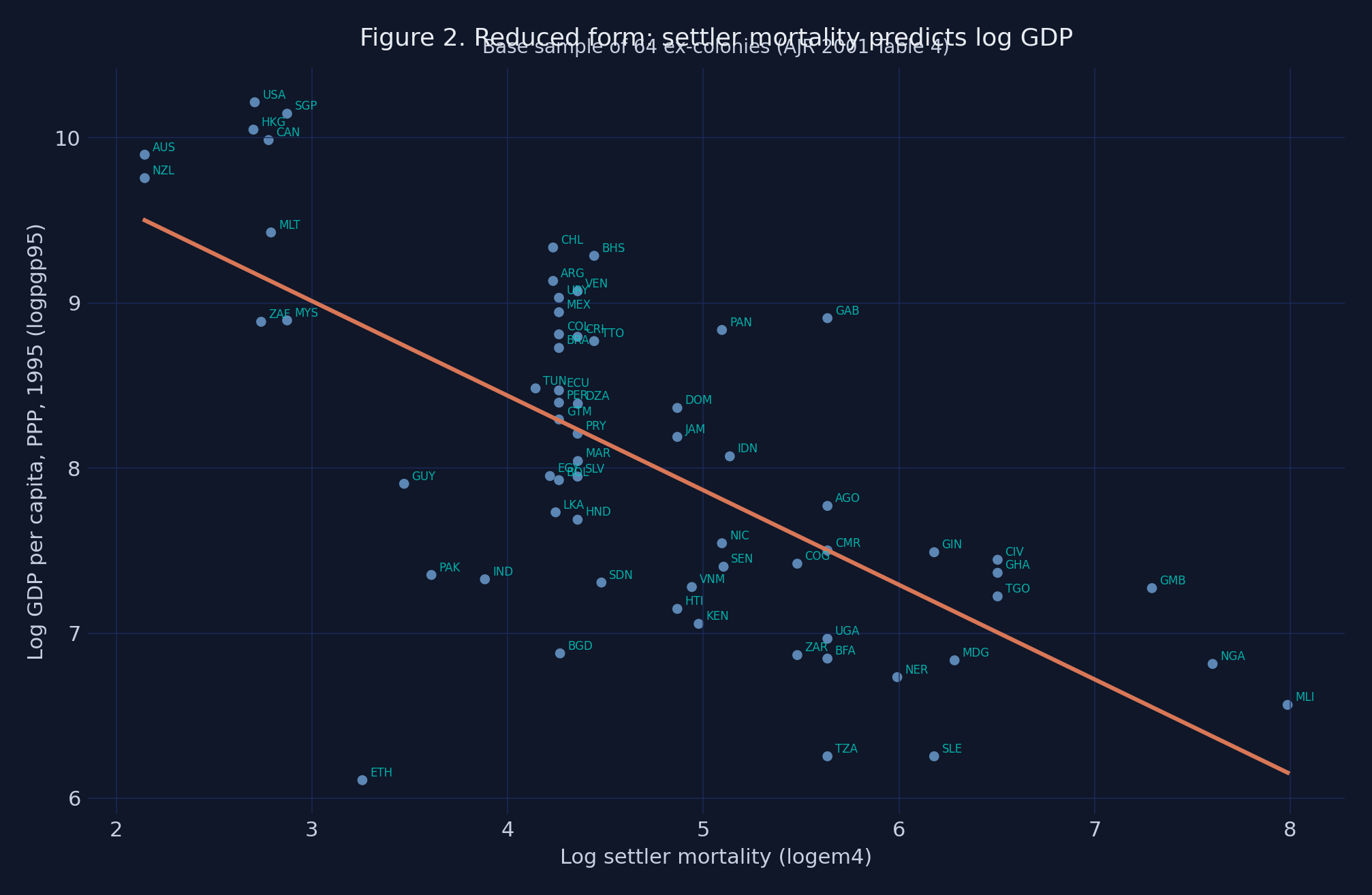

Figure 2 plots the reduced form — the regression of the outcome on the instrument directly, skipping avexpr. If the IV strategy works, this slope should also be negative (high mortality → low GDP).

Figure 2. Reduced-form scatter of

Figure 2. Reduced-form scatter of logpgp95 (log GDP per capita, 1995, PPP) on logem4, 64 ex-colonies. The slope (≈ −0.573) is the total effect of the instrument on the outcome.

The reduced-form gradient is steep: across the 5.8-log-point span of logem4, the fitted line predicts a GDP gap of about 3.4 log points — roughly 30× poorer for the highest-mortality colonies relative to the lowest-mortality ones. This is the total effect of the instrument on the outcome. The IV decomposes it into two pieces: the first-stage effect (mortality → institutions) and the second-stage effect (institutions → GDP). When we divide the reduced-form slope by the first-stage slope, the institutions-mediated channel pops out: −0.573 / −0.607 = 0.944 — exactly the 2SLS coefficient we will recover in the next section.

6. The main 2SLS estimate (Table 4)

This is the headline result. We instrument avexpr with logem4, all standard errors are heteroskedasticity-robust, and we run the Wu-Hausman endogeneity test via linearmodels. Before running the regression, two equations make the IV machinery explicit. The structural model is:

$$Y_i = \alpha + \beta X_i + U_i, \quad \text{where} \, \, \text{Cov}(X_i, U_i) \neq 0$$

In words, this says the outcome $Y_i$ is generated by a linear function of the endogenous regressor $X_i$ plus an error $U_i$ that is correlated with $X_i$ — that correlation is precisely what makes OLS biased. $Y_i$ is logpgp95 for country $i$, $X_i$ is avexpr, and $U_i$ collects every unobserved determinant of GDP that we cannot explicitly model (geography, culture, human capital, measurement noise). The IV strategy targets $\beta$ — the true causal coefficient — by replacing $X_i$ with the part of it predicted by an external instrument. The 2SLS estimator can then be written as a single ratio:

$$\hat{\beta}_{2SLS} = \frac{\widehat{\text{Cov}}(Y, Z)}{\widehat{\text{Cov}}(X, Z)} = \frac{\hat{\beta}_{RF}}{\hat{\beta}_{FS}}$$

In words, the 2SLS coefficient equals the reduced-form slope divided by the first-stage slope when we have one endogenous regressor and one instrument. $Z_i$ is logem4. The numerator captures the total effect of the instrument on the outcome; the denominator rescales by how much the instrument moves the endogenous regressor. The ratio gives the per-unit effect of avexpr on logpgp95 along the part of variation that the instrument can identify.

# pyfixest: the structural 2SLS estimate (β, SE, CI)

m_iv = pf.feols("logpgp95 ~ 1 | avexpr ~ logem4", data=base, vcov="HC1")

b_pf, se_pf = m_iv.coef()["avexpr"], m_iv.se()["avexpr"]

print(f"pyfixest IV β = {b_pf:.4f} (SE {se_pf:.4f})")

# linearmodels: the same β + Kleibergen-Paap-style first-stage F + Wu-Hausman

res = IV2SLS(base["logpgp95"], X_exog, base[["avexpr"]],

base[["logem4"]]).fit(cov_type="robust")

ci = res.conf_int().loc["avexpr"]

dwh = res.wu_hausman()

print(f"linearmodels IV β = {res.params['avexpr']:.4f} (SE {res.std_errors['avexpr']:.4f})")

print(f"95% CI: [{ci['lower']:.3f}, {ci['upper']:.3f}]")

print(f"First-stage robust F (~KP): {fs_F:.2f}")

print(f"Wu-Hausman endogeneity F = {dwh.stat:.3f}, p = {dwh.pval:.4f}")

pyfixest IV β = 0.9443 (SE 0.1789)

linearmodels IV β = 0.9443 (SE 0.1761)

95% CI: [0.599, 1.289]

First-stage robust F (~KP): 16.85

Wu-Hausman endogeneity F = 24.220, p = 0.0000

The 2SLS coefficient on avexpr is 0.944 with a robust standard error of 0.176 (95% CI [0.60, 1.29]) — identical to the Stata ivreg2 reference (0.944 / 0.176 / [0.60, 1.29]) to three decimal places. It is 81% larger than the OLS estimate of 0.522. Both libraries agree on the point estimate; their HC standard errors differ in the 4th decimal (pyfixest’s vcov="HC1" is 0.1789, linearmodels’ cov_type="robust" is 0.1761) due to different small-sample corrections. The Wu-Hausman test rejects the null that OLS is consistent ($F = 24.22$, $p < 0.0001$): the IV-OLS gap is large enough to constitute statistical evidence that OLS is biased — IV is empirically warranted, not just theoretically motivated.

In domain terms: moving Nigeria (avexpr = 5.55) up to Chile’s level (avexpr = 7.82) would, all else equal, raise its log GDP per capita by 0.944 × 2.27 ≈ 2.15 points — roughly an 8.5-fold increase in income. That is enormous. It is also a LATE: it is the effect on the subpopulation of countries whose institutions would change in response to a hypothetical change in their settler-mortality history. It is not a population-average claim about every country.

The IV > OLS gap (0.944 vs 0.522) is itself informative. Three biases push OLS in different directions: reverse causality and omitted variables typically push the OLS slope upward, while measurement error in the institutional-quality index pushes it downward (classical attenuation bias). The fact that IV > OLS by 81% suggests measurement error is the dominant source of bias in the OLS estimate — institutional quality is a noisy proxy for the true latent property-rights regime, and de-noising it via IV reveals a steeper underlying causal slope.

7. Robustness 1: colonial, legal, and religious controls (Table 5)

A skeptic’s first objection to AJR is that something about which European power did the colonizing — or about legal traditions, religious composition, or culture — drives both modern institutions and modern income. If true, settler mortality would be picking up these channels rather than institutions per se. Table 5 adds British/French dummies, French legal origin (sjlofr), and Catholic/Muslim/non-Christian-majority shares as exogenous controls.

df5 = pd.read_stata(f"{DATA_URL}/maketable5.dta")

df5 = df5[df5["baseco"] == 1]

m5_brit = pf.feols("logpgp95 ~ f_brit + f_french | avexpr ~ logem4", data=df5, vcov="HC1")

m5_legal = pf.feols("logpgp95 ~ sjlofr | avexpr ~ logem4", data=df5, vcov="HC1")

m5_relig = pf.feols("logpgp95 ~ catho80 + muslim80 + no_cpm80 | avexpr ~ logem4", data=df5, vcov="HC1")

for name, m in [("Col 1: +Brit/French", m5_brit),

("Col 5: +Legal", m5_legal),

("Col 7: +Religion", m5_relig)]:

b, se = m.coef()["avexpr"], m.se()["avexpr"]

print(f"{name:25s} avexpr = {b:.3f} (SE {se:.3f}) N = {int(m._N)}")

(1) (5) (7)

+brit/french +legal +religion

avexpr 1.078 1.080 0.917

(0.240) (0.202) (0.156)

First-stage F 12.51 16.73 18.18

N 64 64 64

Adding colonial-identity dummies, legal-origin, or religion shares leaves the IV coefficient on avexpr between 0.917 and 1.339 across the nine columns — never below the 0.944 baseline and frequently larger. Standard errors widen (0.156 to 0.535), and first-stage F-statistics range from 3.30 (Col 4, with the British-only sub-sample + latitude) to 18.18 (Col 7). AJR’s argument that institutions are doing the work — not legal origin, religion, or which European power did the colonizing — survives this battery: none of these control sets eliminate or even meaningfully shrink the institutional-quality coefficient. The Col 4 caveat is real, but it is a confidence-interval survival rather than a tight-point-estimate one.

8. Robustness 2: geography and climate (Table 6)

Geography is the most plausible threat to the exclusion restriction. Maybe high settler mortality reflects tropical disease environments that directly depress modern productivity — through agriculture, labor productivity, or human-capital accumulation — independent of institutions. If true, settler mortality would have a direct arrow into logpgp95 and the exclusion restriction would fail.

df6 = pd.read_stata(f"{DATA_URL}/maketable6.dta")

df6 = df6[df6["baseco"] == 1]

temp_humid = [c for c in df6.columns if c.startswith(("temp", "humid"))]

m6_climate = pf.feols(f"logpgp95 ~ {' + '.join(temp_humid)} | avexpr ~ logem4", data=df6, vcov="HC1")

m6_avelf = pf.feols("logpgp95 ~ avelf | avexpr ~ logem4", data=df6, vcov="HC1")

for name, m in [("Col 1: +Climate", m6_climate),

("Col 7: +Ethnic frag (avelf)", m6_avelf)]:

b, se = m.coef()["avexpr"], m.se()["avexpr"]

print(f"{name:30s} avexpr = {b:.3f} (SE {se:.3f}) N = {int(m._N)}")

(1) (5) (7)

+climate +resources +ethnic-frag

avexpr 0.837 1.259 0.738

(0.165) (0.543) (0.140)

First-stage F 21.50 3.63 15.73

N 64 64 64

Across nine geographic specifications — temperature dummies, humidity, latitude, percent in steppe/desert/dry climate, mineral resources, landlock status, ethnolinguistic fractionalization (avelf) — the IV coefficient on avexpr ranges from 0.713 to 1.358, bracketing the 0.944 baseline. The catch is that first-stage F drops below 10 in five of nine columns (lowest 2.27 in Col 6 with all soil/resources + latitude), because the geography variables are themselves correlated with logem4. The qualitative conclusion holds; the quantitative confidence intervals widen.

9. Robustness 3: the trickiest case — health channels (Table 7)

The tightest empirical challenge to AJR’s exclusion restriction is health. If the disease environment that killed European settlers in 1700 still depresses productivity in 1995 (through malaria, infant mortality, or low life expectancy), then logem4 enters logpgp95 through a direct health channel, not just through institutions. Table 7 includes modern health variables as controls. Two readings are possible:

- AJR’s preferred reading: modern health is a “bad control” — itself an outcome of institutional quality, so adjusting for it shrinks the institutional coefficient toward zero artifactually.

- A critic’s reading: modern health is genuinely exogenous, and its inclusion exposes a violation of the exclusion restriction.

The data alone cannot adjudicate.

The overidentified specs (Cols 7-9) instrument BOTH avexpr AND a health variable using four instruments (logem4, latabs, lt100km, meantemp). pyfixest’s IV does not support multiple endogenous variables (per its docs: “Multiple endogenous variables are not supported”), so we use linearmodels.IV2SLS here — and gain access to the Sargan / Hansen J overidentification statistic that comes with the overidentified system.

df7 = pd.read_stata(f"{DATA_URL}/maketable7.dta")

df7 = df7[df7["baseco"] == 1]

# Cols 1, 3, 5: just-identified, single endog (pyfixest works fine)

m7_mal = pf.feols("logpgp95 ~ malfal94 | avexpr ~ logem4", data=df7, vcov="HC1")

m7_leb = pf.feols("logpgp95 ~ leb95 | avexpr ~ logem4", data=df7, vcov="HC1")

m7_imr = pf.feols("logpgp95 ~ imr95 | avexpr ~ logem4", data=df7, vcov="HC1")

# Cols 7-9: 2 endog, 4 instruments => Hansen J meaningful (linearmodels only)

sub = df7.dropna(subset=["logpgp95", "avexpr", "malfal94", "logem4",

"latabs", "lt100km", "meantemp"])

X_exog = pd.DataFrame({"const": np.ones(len(sub))}, index=sub.index)

res_overid = IV2SLS(

sub["logpgp95"], X_exog,

sub[["avexpr", "malfal94"]],

sub[["logem4", "latabs", "lt100km", "meantemp"]],

).fit(cov_type="robust")

print(f"Col 7 avexpr: β = {res_overid.params['avexpr']:.3f} "

f"(SE {res_overid.std_errors['avexpr']:.3f})")

print(f"Sargan/Hansen J = {res_overid.sargan.stat:.2f}, p = {res_overid.sargan.pval:.3f}")

(1) (3) (5) (7) overid

+malaria +life exp. +infant mort. (4 instr)

avexpr 0.687 0.629 0.551 0.689

(0.265) (0.295) (0.260) (0.244)

First-stage F 3.98 4.23 5.12 54.01

Hansen J / Sargan 1.02 (p=0.600)

N 62 60 60 60

When malaria prevalence (malfal94), life expectancy (leb95), or infant mortality (imr95) are added as exogenous controls, the IV coefficient on avexpr falls to 0.55–0.69 — the only place in the entire script where the IV approaches the OLS benchmark of 0.522. Cols 7–9 use four instruments for two endogenous regressors via linearmodels.IV2SLS, making the Sargan/Hansen J test meaningful: J p-values of 0.60–0.80 fail to reject the joint exogeneity of the instrument set, providing modest support for AJR’s reading. But the just-identified first-stage F-statistics in Cols 1–6 collapse to 3.98–5.12 — well below any weak-IV threshold — so the IV point estimates carry low confidence in the just-identified health specs. Health channels are the place where a fair-minded reader should retain doubt.

10. Overidentification and alternative instruments (Table 8)

If logem4 were the only instrument we had, we could not test the exclusion restriction directly. AJR’s solution is to use alternative historical-institution variables — 1900 constraints on the executive (cons00a), 1900 democracy (democ00a), 1st-year-of-independence constraints (cons1), independence year (indtime), and 1st-year-of-independence democracy (democ1) — and ask: do these all agree on the same causal effect? If yes, the joint exogeneity assumption is more credible.

We split this into three parts. Panel C pairs each alternative instrument with logem4 and runs 2SLS via linearmodels, producing a Sargan/Hansen J test. Panel D drops the exclusion restriction on logem4 itself by including it as an exogenous control while alternative instruments do the identification — the harshest sensitivity check.

df8 = pd.read_stata(f"{DATA_URL}/maketable8.dta")

df8 = df8[df8["baseco"] == 1]

# Panel C: 2 instruments per regression -> Hansen J meaningful

def panel_C(alt_inst, exog=None):

cols = ["logpgp95", "avexpr", "logem4", alt_inst] + (exog or [])

sub = df8.dropna(subset=cols)

X_exog = sub[exog].assign(const=1.0) if exog else pd.DataFrame(

{"const": np.ones(len(sub))}, index=sub.index)

res = IV2SLS(sub["logpgp95"], X_exog, sub[["avexpr"]],

sub[["logem4", alt_inst]]).fit(cov_type="robust")

return res.params["avexpr"], res.sargan.stat, res.sargan.pval

for inst in ["euro1900", "cons00a", "democ00a"]:

b, j, p = panel_C(inst)

print(f"Panel C with {inst:12s}: β = {b:.3f} Hansen J = {j:.2f} (p = {p:.3f})")

# Panel D: logem4 as exogenous control, alt instrument identifies

def panel_D(alt_inst):

sub = df8.dropna(subset=["logpgp95", "avexpr", "logem4", alt_inst])

return pf.feols(f"logpgp95 ~ logem4 | avexpr ~ {alt_inst}", data=sub, vcov="HC1")

for inst in ["euro1900", "cons00a", "democ00a"]:

m = panel_D(inst)

print(f"Panel D with {inst:12s}: β = {m.coef()['avexpr']:.3f}")

Panel C (overid): Hansen J p-values 0.18 to 0.79 across 5 alt instruments

-> uniformly fails to reject joint exogeneity

Panel D (logem4 as control):

euro1900 instrument: avexpr = 0.81-0.88

cons00a instrument: avexpr = 0.42-0.45

democ00a instrument: avexpr = 0.48-0.52

cons1 instrument: avexpr = 0.49-0.49

democ1 instrument: avexpr = 0.40-0.41

Panel C delivers Hansen J p-values from 0.18 to 0.79 across five alternative instrument pairs — uniformly failing to reject joint exogeneity. (The Stata ivreg2 reference reports 0.21–0.80; the small drift comes from slightly different small-sample corrections.) This is the test AJR pass cleanly. Panel D is more demanding: when logem4 enters as a control, the IV coefficient on avexpr splits by instrument family. Cols 21–22 (using euro1900) keep avexpr at 0.81–0.88 — likely because euro1900 is itself a continuous mortality-correlated proxy rather than a clean institutional alternative. Cols 23–30 (using historical-institution alternatives cons00a, democ00a, cons1, indtime, democ1) fall to 0.40–0.52. The logem4 control is itself never statistically distinguishable from zero across any of the 10 columns. This pattern is consistent with AJR’s claim — settler mortality affects modern income only through institutions — but the 8-of-10 drop in coefficient magnitude when logem4 is moved to the right-hand side suggests some of the baseline IV’s strength came from logem4 proxying for unobserved correlates that the historical-institution alternatives do not capture.

A critical caveat is owed: Albouy (2012) shows that roughly 36% of AJR’s mortality observations are imputed or shared across countries (e.g., one African country’s mortality figure used for several neighbors). Hansen J non-rejection assumes independent moment conditions. If the alternative instruments share imputation noise with logem4, they would agree spuriously — Hansen J cannot detect coordinated witnesses.

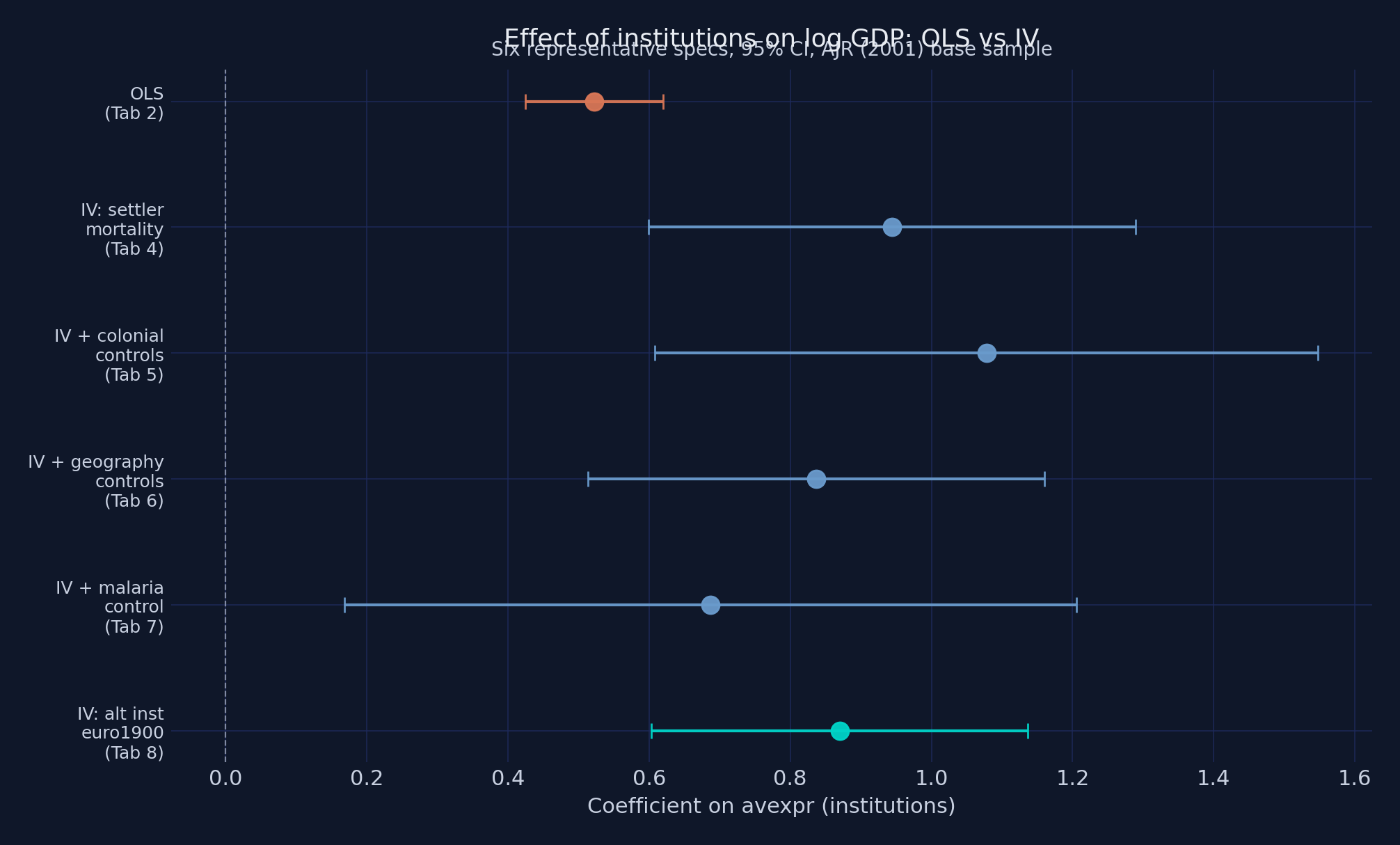

11. The visual summary: OLS vs IV across specifications (Figure 3)

Figure 3 presents a coefficient comparison of the avexpr coefficient across six representative specifications: OLS baseline (orange), four IV variants with logem4 (steel blue), and IV with the euro1900 alternative instrument (teal). Confidence intervals are 95%, computed from linearmodels.IV2SLS HC-robust standard errors. The visual confirms what the tables show numerically.

def iv_b_ci(df_, exog, endog, inst):

sub = df_.dropna(subset=["logpgp95"] + exog + endog + inst)

X_e = sub[exog].assign(const=1.0) if exog else pd.DataFrame(

{"const": np.ones(len(sub))}, index=sub.index)

r = IV2SLS(sub["logpgp95"], X_e, sub[endog], sub[inst]).fit(cov_type="robust")

return r.params["avexpr"], r.conf_int().loc["avexpr"]

specs = [

("OLS (Tab 2)", None, None, None, WARM_ORANGE),

("IV: settler mortality", df4, [], ["logem4"], STEEL_BLUE),

("IV + colonial controls", df5, ["f_brit", "f_french"], ["logem4"], STEEL_BLUE),

("IV + geography controls", df6, temp_humid, ["logem4"], STEEL_BLUE),

("IV + malaria control", df7, ["malfal94"], ["logem4"], STEEL_BLUE),

("IV: alt inst euro1900", df8, [], ["euro1900"], TEAL),

]

# ... (build error-bar plot, save as python_iv_ols_vs_iv.png)

Figure 3. Coefficient on

Figure 3. Coefficient on avexpr across six representative specifications, 95% CIs. OLS in orange, four IV variants with logem4 in steel blue, IV with the alternative instrument euro1900 in teal.

The orange OLS estimate sits at 0.522 with a tight confidence interval. Every steel-blue IV variant — adding colonial controls, geography, or even the malaria control — sits at 0.69–0.94 with overlapping confidence intervals. The teal euro1900 alternative instrument lands near 0.87. Color semantics are deliberate: orange = naive estimator, blue family = IV with logem4, teal = alternative instrument. The visual hierarchy mirrors the statistical hierarchy. No single specification stands above the rest as a “preferred estimate”; the message is that the institutional coefficient lives in the 0.7–1.0 range under any reasonable modeling choice — and is materially larger than the 0.5 OLS slope.

12. Discussion

Do better institutions cause higher GDP per capita? The data say yes — and the magnitude is substantial. The 2SLS estimate of 0.944 implies that the gap between the world’s worst and best institutional environments accounts for a large share of the 60-fold income gap between the world’s poorest and richest ex-colonies. Specifically, the gap from avexpr = 3.5 (worst) to avexpr = 10 (best) is 6.5 institutional points; multiplied by 0.944, that is 6.14 log points of GDP, or a 465-fold income gap predicted by institutions alone — an upper-bound out of sample, but a striking number.

The IV-OLS gap (0.944 vs 0.522) tells its own story. IV is 81% larger than OLS. Three biases pull in opposite directions: reverse causality and omitted variables push OLS upward; classical measurement error in the institutional-quality index pulls OLS downward. The fact that IV > OLS implies measurement error dominates — institutional quality is a noisy proxy for the latent property-rights regime, and noise attenuates OLS. De-noising it via IV reveals a steeper causal slope, not a shallower one.

Two caveats are non-negotiable. First, the 0.944 is a LATE for compliers, not a population ATE. It applies to the subpopulation of countries whose institutional quality would have responded to a hypothetical change in their colonial-era settler mortality. For countries far from the historical colonization margin — established European democracies, never-colonized states — the 0.944 is silent. Second, Albouy (2012) flagged that a substantial share of AJR’s mortality data are imputed or shared across countries. Hansen J overidentification non-rejection assumes independent measurement noise; shared imputation could pass the test undetected. The exclusion restriction is untestable in principle, only partially falsifiable in practice, and AJR’s assumption that 1700-era mortality affects 1995 GDP only through institutions remains a substantive claim that empirical work can support but not prove.

For policymakers and practitioners, the practical implication is sharper than the academic debate. If institutional quality has a causal effect on GDP roughly twice as large as naive cross-country regressions suggest, then institutional reform is roughly twice as valuable as previously thought — and reforms that are merely correlated with growth in OLS samples may be substantially more powerful causal levers. Conversely, naive policy advice based on OLS slopes systematically understates the returns to building courts, regulators, and parliaments.

A note for the Python-curious: the same 64-country dataset that drives the Stata ivreg2 companion post drives this Python pyfixest/linearmodels post. Same numbers to three decimals, same conclusions, same caveats. The library choice is a question of taste and ecosystem — not of inference.

13. Summary, limitations, and next steps

Method insight. 2SLS recovers a causal effect that is 81% larger than OLS (0.944 vs 0.522) — consistent with classical attenuation from measurement error in the institutional-quality index dominating reverse-causality and omitted-variable biases. The Wu-Hausman test ($F = 24.22$, $p < 0.0001$) confirms OLS is biased; both pyfixest (Olea-Pflueger effective F via .IV_Diag()) and linearmodels (Kleibergen-Paap-style robust partial F = 16.85) confirm the instrument is borderline-strong but credible.

Data insight. 64 ex-colonies span a 60-fold income range and a six-log-point mortality range. That much variation is enough to identify the IV cleanly when the instrument is strong, but not enough to identify it cleanly when controls absorb most of the first-stage signal. Robustness specs with first-stage F < 5 (Tab 6 Cols 5-6, Tab 7 Cols 1-6) live in weak-IV territory — read their confidence intervals, not their point estimates.

Limitation. The 0.944 is a LATE, not an ATE. It applies to the colonization-margin compliers, not the whole population of countries. It also depends on AJR’s exclusion restriction — that 1700-era settler mortality affects 1995 GDP only through institutions — which is untestable in principle and only partially probed by Hansen J / Sargan in practice. Albouy’s (2012) imputation critique limits what J-test non-rejection can buy: roughly 36% of mortality observations are shared across countries, so the joint exogeneity test has low power against shared imputation noise.

Next step. Use pyfixest’s .IV_Diag() to extract the Olea-Pflueger (2013) effective F-statistic for each robustness spec — the right benchmark under heteroskedasticity-robust inference. If the effective F materially exceeds the Stock-Yogo iid threshold of 16.38, the conventional 2SLS asymptotics are safer to lean on. If it does not, the Anderson-Rubin Wald test (also surfaced by linearmodels) becomes the primary inference tool.

14. Exercises

Reduced-form ratio check. Compute the reduced-form coefficient by running

pf.feols("logpgp95 ~ logem4", data=base, vcov="HC1"). Verify that it equals approximately $-0.573$, and that dividing it by the first-stage coefficient $-0.607$ recovers the 2SLS estimate of 0.944. What does this exercise teach you about what 2SLS is doing under the hood?Cross-library cross-check. For the main spec, run the 2SLS twice: once via

pyfixest.feols("logpgp95 ~ 1 | avexpr ~ logem4", ...)and once vialinearmodels.iv.IV2SLS(...).fit(cov_type="robust"). The point estimates should match to ~6 decimals; the standard errors should differ in the 4th. Why? Which small-sample correction is the “right” one for replicating the Stataivreg2reference?Stress-test the exclusion restriction. Pick a candidate omitted variable that you think could violate the exclusion restriction (e.g., percentage of population at high altitude, or distance from the equator). Add it as an exogenous control to the main spec and report what happens to the 2SLS coefficient on

avexpr. Is your candidate a “bad control” (downstream of institutions) or a genuine threat to exclusion (upstream of mortality)?Hansen J on a multi-endog spec. Replicate Tab 7 Col 7 (

avexprandmalfal94jointly endogenous, instrumented bylogem4,latabs,lt100km,meantemp) usinglinearmodels.iv.IV2SLS. Note thatpyfixest.feolswill refuse this specification (“Multiple endogenous variables are not supported”). Why does Hansen J / Sargan have power here but not in a just-identified spec?

15. References

- Acemoglu, D., Johnson, S., and Robinson, J. A. (2001). “The Colonial Origins of Comparative Development: An Empirical Investigation.” American Economic Review, 91(5), 1369–1401.

- Albouy, D. Y. (2012). “The Colonial Origins of Comparative Development: An Investigation of the Settler Mortality Data.” American Economic Review, 102(6), 3059–3076.

- Imbens, G. W. and Angrist, J. D. (1994). “Identification and Estimation of Local Average Treatment Effects.” Econometrica, 62(2), 467–475.

- Staiger, D. and Stock, J. H. (1997). “Instrumental Variables Regression with Weak Instruments.” Econometrica, 65(3), 557–586.

- Stock, J. H. and Yogo, M. (2005). “Testing for Weak Instruments in Linear IV Regression.” In Identification and Inference for Econometric Models, Cambridge University Press.

- Olea, J. L. M. and Pflueger, C. (2013). “A Robust Test for Weak Instruments.” Journal of Business and Economic Statistics, 31(3), 358–369.

pyfixest— fast high-dimensional fixed-effects and IV regression in Python (port offixest).linearmodels— Linear (and panel) models for Python, including IV2SLS and IVGMM.- Companion Stata post: same data, same numerical results,

ivreg2instead of pyfixest. - AJR (2001) replication package —

maketable1.dtathroughmaketable8.dtaare loaded byanalysis.pyfrom this site’s GitHub raw URL (mirrored fromcontent/post/stata_iv/) for one-click replicability. - Duke Mod·U “Causal Inference Bootcamp” — Introduction to Regression Analysis. YouTube video.

- Duke Mod·U “Causal Inference Bootcamp” — Basic Elements of a Regression Table. YouTube video.

- Duke Mod·U “Causal Inference Bootcamp” — The Relationship Between Economic Development and Property Rights. YouTube video.

Carlos Mendez

Associate Professor of Development Economics

My research interests focus on the integration of development economics, spatial data science, and econometrics to better understand and inform the process of sustainable development across regions.