The lab: 100 firms × 10 years, with a known true effect of 0.5

Outcome \(y\) — firm performance (1,000 rows, 2010–2019)Treatment \(x\) — R&D intensity, correlated with unobserved firm abilityErrors — within-firm AR(1) serial correlation, \(\rho = 0.5\)

Because ability drives both \(x\) and \(y\) , pooled OLS is biased by design — and AR(1) errors make SE choice critical.

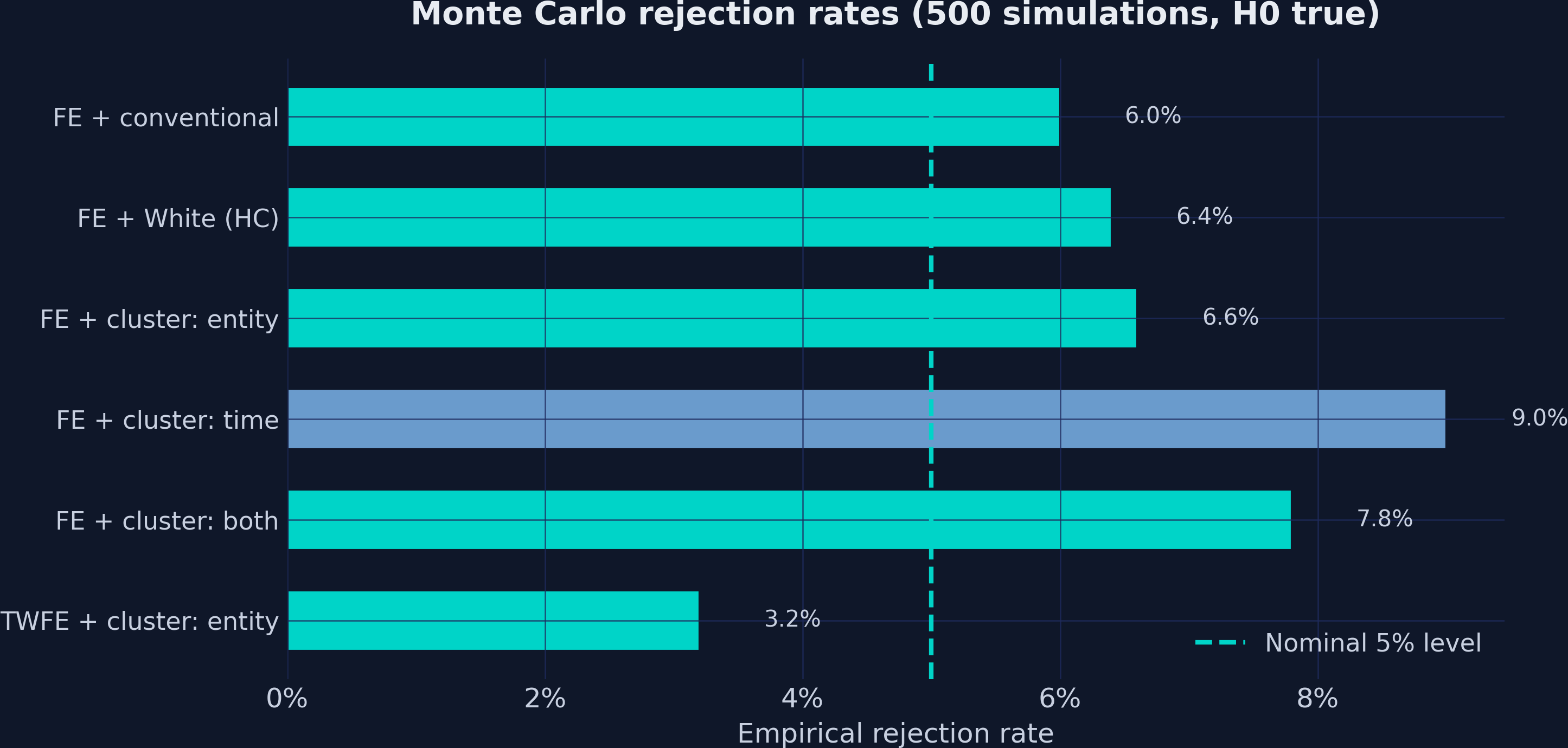

Simulated data has a decisive advantage: we know the answer. If the true effect is exactly 0.5, we can check whether each SE estimator’s 95% CI covers 0.5 about 95% of the time. The DGP: y = 2.0 + 0.5·x + mu_i + lambda_t + eps_it, with mu_i correlated with x.

The true model bakes ability and serial correlation into the data

\[y_{it} = 2.0 + 0.5\,x_{it} + \mu_i + \lambda_t + \varepsilon_{it}\]

\(\mu_i\) — firm ability, correlated with \(x_{it}\) \(\Rightarrow\) omitted-variable bias\(\lambda_t\) — weak year effects, \(\lambda_t \sim N(0, 0.5)\) \(\varepsilon_{it}\) — AR(1) within firm, \(\rho = 0.5\) \(\Rightarrow\) within-cluster correlation

This is the generative truth. The firm effect mu_i is the confounder — capable firms invest more in R&D AND perform better. The AR(1) structure on the errors is what makes conventional SEs understate uncertainty.

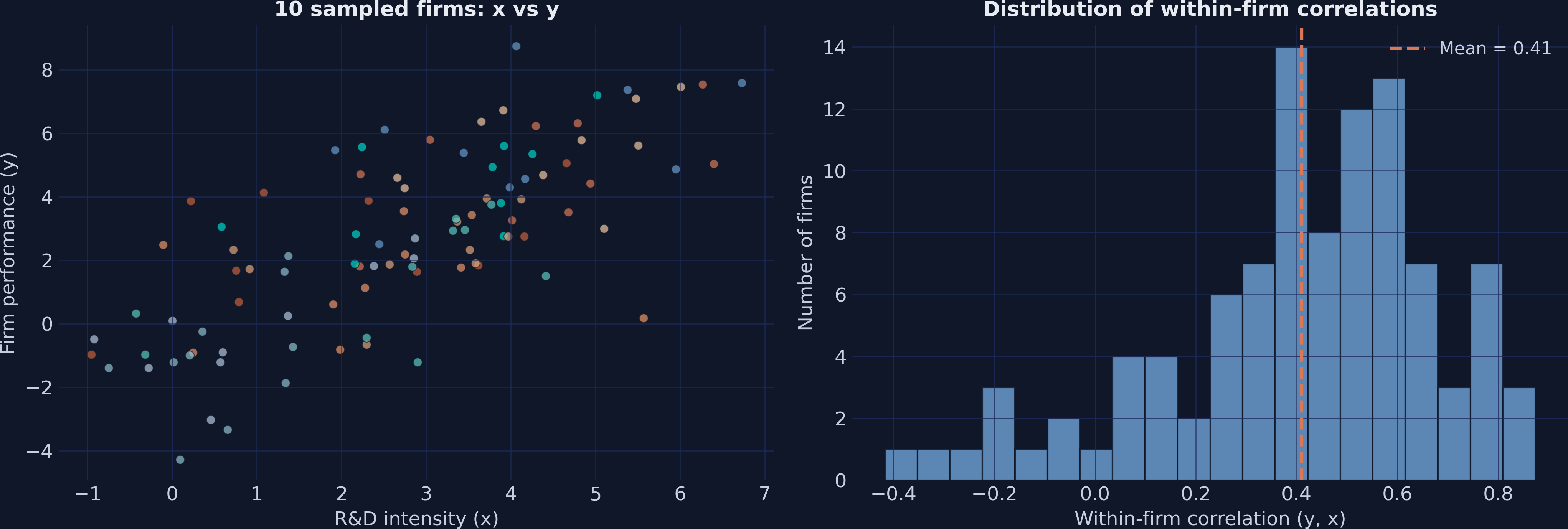

Persistent firm differences dominate — exactly what fixed effects absorb

10 sampled firms cluster in distinct regions (left); within-firm \(y\) –\(x\) correlations center on 0.41 (right).

Left panel: each firm occupies a different region of x–y space — that’s between-firm variation, the confounded part fixed effects remove. Right: most firms show positive within-firm correlation around 0.41, less than 0.5 because AR(1) errors add noise. Between-firm std of y (2.46) exceeds within-firm std (1.67) — fixed effects will matter a lot.

Pooled OLS reports 1.03 — more than double the true 0.5

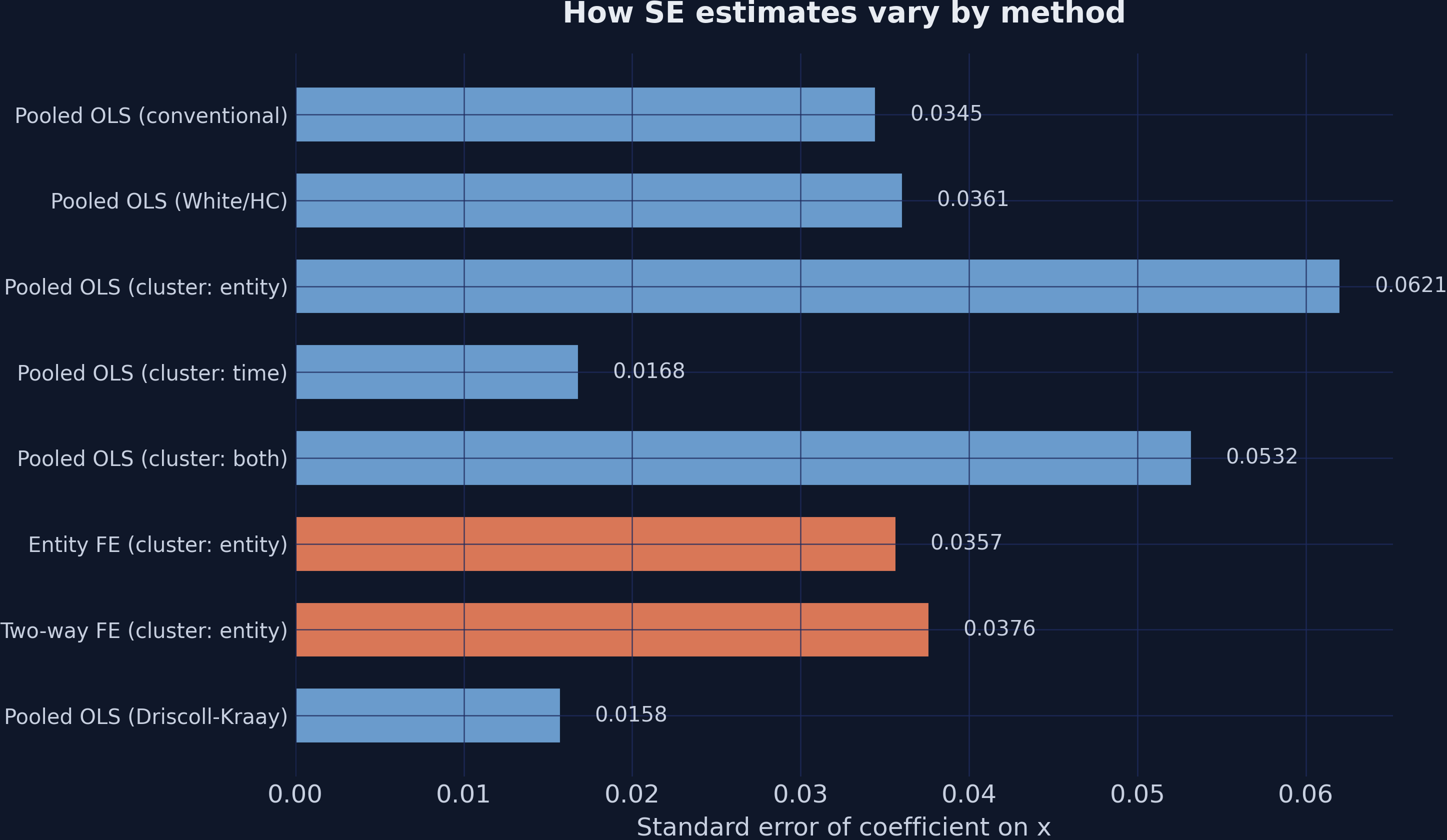

Pooled OLS (conventional)

1.0318 0.0345

29.9

The estimate is wrong , and the tiny SE makes us wrongly confident in the wrong number.

Omitted-variable bias in action: high-ability firms invest more in R&D and perform better, so the regression credits R&D for what ability does. The conventional SE of 0.0345 yields a t of 29.9 — doubly misleading: biased point estimate AND a too-small SE that ignores within-firm correlation. First lesson: a biased estimator with small SEs is worse than a noisy unbiased one.

White SEs barely move the needle — correlation, not heteroskedasticity, is the problem

\[\hat{\Sigma}_{\text{White}} = (X'X)^{-1}\left(\sum_{i=1}^{N} X_i'\,\hat{e}_i^{\,2}\,X_i\right)(X'X)^{-1}\]

White SE = 0.0361 vs conventional 0.0345 — the \(t\) slips only from 29.9 to 28.6.

The White estimator allows each observation its own variance, but still treats observations as independent. It cannot see that firm 1’s 2015 error correlates with its 2016 error. For panel data the binding problem is within-cluster correlation, so White helps almost nothing.

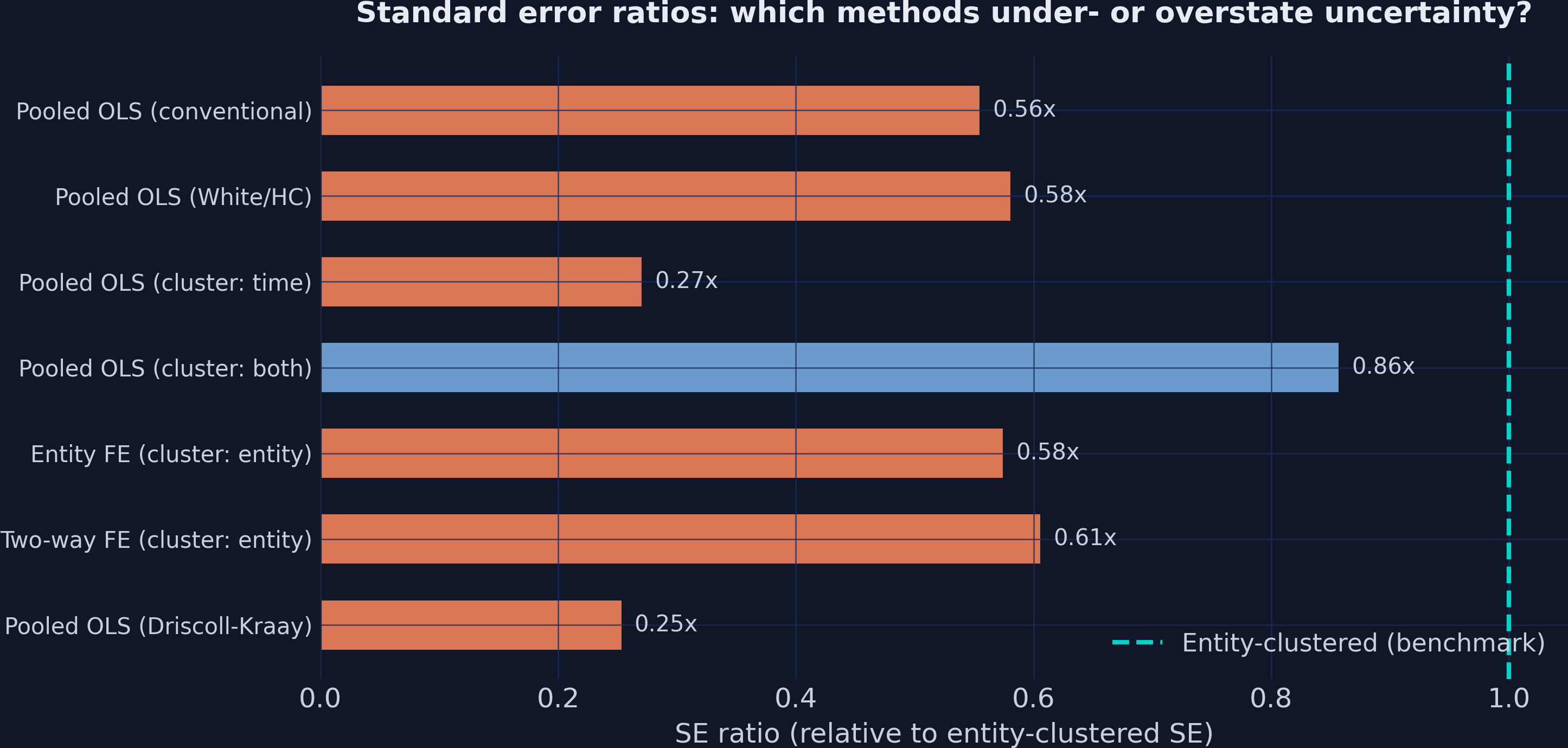

Clustering on firms inflates the SE by 80% — the honest correction

Conventional

1.0318

0.0345

29.9

White (HC)

1.0318

0.0361

28.6

Cluster: entity

1.0318

0.0621 16.6

Ten observations from one firm carry far less than ten independent observations’ worth of information.

Entity clustering allows arbitrary correlation within a firm. The SE jumps to 0.0621 — 80% above conventional, nearly double White. The t falls from 29.9 to 16.6. Analogy: surveying 100 students across 10 classrooms gives you closer to 10 independent data points than 100. In a weaker-effect setting this correction could flip “significant” to “insignificant.”

Time clustering looks precise but lies: only 10 clusters break the asymptotics

Cluster: entity (100 groups)

1.0318

0.0621

16.6

Cluster: time (10 groups)

1.0318

0.0168 61.3

Cluster: both

1.0318

0.0532

19.4

Cluster on the dimension with \(\ge 40\) –\(50\) groups. Here that is firms (100), not years (10).

Time-clustered SEs are SMALLER than conventional, and t leaps to 61 — a trap. Clustered SEs rely on large-cluster asymptotics; 10 year-clusters is far too few. Two-way clustering (0.0532) sits between entity-only and time-only because the weak time dimension drags it down.

Fixed effects subtract each firm’s average — and the bias vanishes

from linearmodels.panel import PanelOLS= PanelOLS.from_formula("y ~ 1 + x + EntityEffects" ,= df_panel)= mod_fe.fit(cov_type= "clustered" , cluster_entity= True )print (res.params["x" ]) # 0.4829 — recovers the true 0.5 print (res.std_errors["x" ]) # 0.0357

EntityEffects demeans within each firm, so the time-invariant ability mu_i drops out — beta is now estimated from within-firm variation only. The cov_type=“clustered” with cluster_entity=True handles the remaining AR(1) within-firm correlation. The post-FE clustered SE (0.0357) is actually smaller than the pooled clustered SE (0.0621) because FE removed the between-firm variation inflating residuals.

Fixed effects recover 0.48 — the bias was the model, not the SE

0.48

Entity FE \(\hat\beta\) (true \(\beta = 0.5\) ); SE 0.0357 · pooled OLS gave 1.03

The single most important number transition: 1.03 (pooled, biased) to 0.48 (FE, ~unbiased). The residual gap of 0.017 is sampling noise, not systematic bias. No standard error correction could have done this — only changing the estimator. Adding TimeEffects barely moves it (0.4796), because the DGP’s time effects are weak.

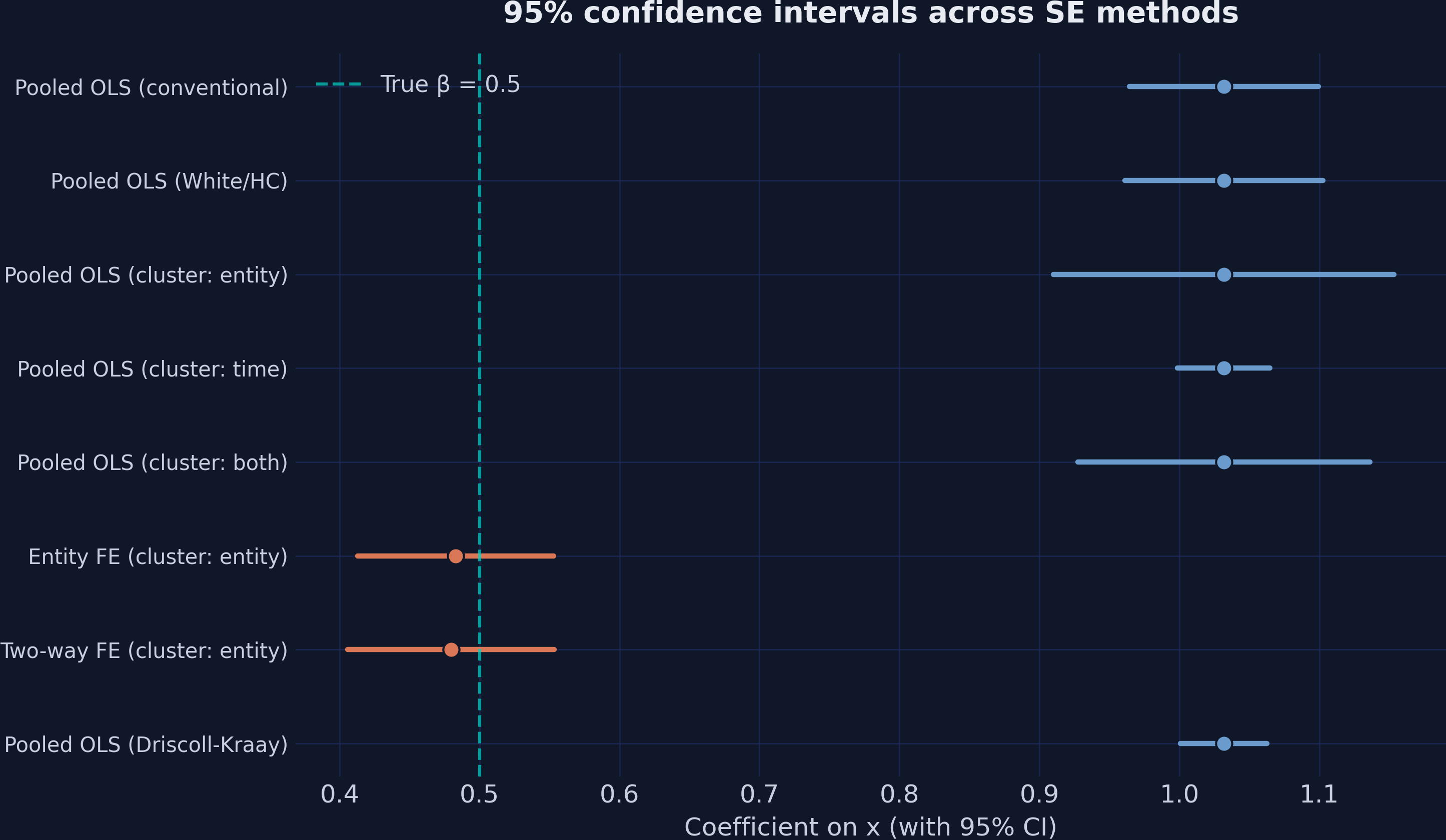

One picture: no SE rescues a biased estimate; FE intervals cover the truth

95% CIs across all eight methods. Teal dashed line = true \(\beta = 0.5\) . Pooled intervals (right) miss it; FE intervals (orange) cover it.

The core visual message. All five pooled OLS intervals sit far to the right of 0.5 — none cover the truth, no matter the SE. The two FE intervals are centered near 0.5 and cover it easily. Standard errors set the WIDTH of the interval; the estimator sets its LOCATION.

Driscoll-Kraay targets cross-sectional shocks — weak here, vital elsewhere

Pooled (Driscoll-Kraay, BW=3)

1.0318

0.0158 65.4

Smallest SE in the deck — because firms are independent given their fixed effects in this DGP .

Driscoll-Kraay uses a Newey-West time kernel on cross-sectional averages — robust to spatial/cross-sectional dependence and serial correlation. Here cross-sectional dependence is weak, so DK is tiny. With strong common shocks (e.g. banks in a recession) and a long T, DK becomes the macro-panel standard. cov_type=“kernel”, kernel=“bartlett”, bandwidth=3.