High-Dimensional Fixed Effects Regression: An Introduction in Python

1. Overview

Imagine you want to know whether union membership raises wages. You run a regression and find a strong positive association: union workers earn 18% more. But wait — what if the workers who join unions are also more motivated, more experienced, or work in industries that pay well regardless? That 18% could be mostly selection, not a genuine union effect. This is one of the most pervasive problems in empirical research: omitted variable bias. Any time your data is grouped — by individual, firm, country, or time period — unobserved characteristics that differ across groups can contaminate your estimates, leading to conclusions that look solid but are fundamentally misleading.

Fixed effects regression is the workhorse solution. By absorbing all time-invariant group-level heterogeneity — a worker’s innate ability, a firm’s management culture, a country’s institutional quality — fixed effects eliminate an entire class of confounders in one step. The result is striking: in the wage panel we analyze below, the apparent union premium drops from 18% to just 7% once we account for individual fixed effects, revealing that more than half the raw association was driven by who selects into unions, not what unions do. This kind of dramatic correction is routine in applied research, which is why fixed effects appear in virtually every empirical paper that uses panel data.

Modern implementations make this computationally painless. Rather than estimating thousands of dummy variables, they use a demeaning algorithm that sweeps out group means before estimation. PyFixest brings this approach to Python with a concise formula syntax inspired by R’s fixest package — the most popular fixed effects library in the R ecosystem. In this tutorial we use PyFixest to build from simple OLS through one-way and two-way fixed effects, compare inference methods, perform instrumental variable estimation, analyze a real wage panel, and run event study designs for difference-in-differences — all with a few lines of code. Along the way, we will see why fixed effects work (by manually reproducing them via demeaning), discover what they cannot do (estimate time-invariant effects like education), learn when standard TWFE breaks down in staggered treatment designs, and apply the CRE/Mundlak approach to recover the very coefficients that one-way FE absorb.

Learning objectives:

- Understand why unobserved group heterogeneity biases OLS and how fixed effects remove that bias

- Implement one-way and two-way fixed effects regressions using PyFixest’s formula syntax

- Compare multiple model specifications efficiently using PyFixest’s stepwise operators

- Assess robustness by computing standard errors under different clustering assumptions

- Decompose panel variation into between and within components to diagnose what FE can and cannot estimate

- Frame a real wage panel through the Mincer equation and its panel extensions

- Recover time-invariant coefficients (education, race) using the CRE/Mundlak approach

- Apply fixed effects to event study designs with staggered treatment adoption

Content outline. Sections 2–4 set up the environment and establish an OLS baseline. Sections 5–6 introduce fixed effects — first through PyFixest’s absorption syntax, then by reproducing the same result manually via demeaning, building intuition for what FE actually does to the data. Section 7 shows how to compare multiple specifications in a single call, and Section 8 explores how standard error choices affect inference. Section 9 extends to two-way FE, and Section 10 combines FE with instrumental variables. Section 11 is the core case study: a real wage panel framed by the Mincer equation, where we decompose within and between variation, see how one-way FE absorb time-invariant variables like education, stress-test the common trends assumption with group-specific time effects, and recover education’s coefficient through the CRE/Mundlak approach. Section 12 applies FE to event study designs, with a careful discussion of why period −1 serves as the universal baseline. Throughout, each section builds on the previous — the manual demeaning in Section 6 explains why education vanishes in Section 11, and the stepwise comparison in Section 7 foreshadows the specification table in Section 11.

2. Setup and imports

Before running the analysis, install the required packages if needed:

pip install pyfixest

The following code imports PyFixest and standard data science libraries. PyFixest provides feols() as its main estimation function, which accepts R-style formulas with a pipe | separator for fixed effects.

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import pyfixest as pf

# Reproducibility

RANDOM_SEED = 42

np.random.seed(RANDOM_SEED)

# Site color palette

STEEL_BLUE = "#6a9bcc"

WARM_ORANGE = "#d97757"

NEAR_BLACK = "#141413"

TEAL = "#00d4c8"

Dark theme figure styling (click to expand)

# Dark theme palette (consistent with site navbar/dark sections)

DARK_NAVY = "#0f1729"

GRID_LINE = "#1f2b5e"

LIGHT_TEXT = "#c8d0e0"

WHITE_TEXT = "#e8ecf2"

# Plot defaults — minimal, spine-free, dark background

plt.rcParams.update({

"figure.facecolor": DARK_NAVY,

"axes.facecolor": DARK_NAVY,

"axes.edgecolor": DARK_NAVY,

"axes.linewidth": 0,

"axes.labelcolor": LIGHT_TEXT,

"axes.titlecolor": WHITE_TEXT,

"axes.spines.top": False,

"axes.spines.right": False,

"axes.spines.left": False,

"axes.spines.bottom": False,

"axes.grid": True,

"grid.color": GRID_LINE,

"grid.linewidth": 0.6,

"grid.alpha": 0.8,

"xtick.color": LIGHT_TEXT,

"ytick.color": LIGHT_TEXT,

"xtick.major.size": 0,

"ytick.major.size": 0,

"text.color": WHITE_TEXT,

"font.size": 12,

"legend.frameon": False,

"legend.fontsize": 11,

"legend.labelcolor": LIGHT_TEXT,

"figure.edgecolor": DARK_NAVY,

"savefig.facecolor": DARK_NAVY,

"savefig.edgecolor": DARK_NAVY,

})

3. Data loading and exploration

3.1 Loading the dataset

PyFixest includes a built-in synthetic dataset designed for demonstrating fixed effects regression. We load it with pf.get_data(), which returns a DataFrame with outcome variables (Y, Y2), covariates (X1, X2), fixed effect identifiers (f1, f2, f3, group_id), instruments (Z1, Z2), and sampling weights.

data = pf.get_data()

print(f"Dataset shape: {data.shape}")

print(f"\nColumn names: {list(data.columns)}")

print(data.head())

print(data.describe().round(3))

Dataset shape: (1000, 11)

Column names: ['Y', 'Y2', 'X1', 'X2', 'f1', 'f2', 'f3', 'group_id', 'Z1', 'Z2', 'weights']

Y Y2 X1 X2 ... group_id Z1 Z2 weights

0 NaN 2.357103 0.0 0.457858 ... 9.0 -0.330607 1.054826 0.661478

1 -1.458643 5.163147 NaN -4.998406 ... 8.0 NaN -4.113690 0.772732

2 0.169132 0.751140 2.0 1.558480 ... 16.0 1.207778 0.465282 0.990929

3 3.319513 -2.656368 1.0 1.560402 ... 3.0 2.869997 0.467570 0.021123

4 0.134420 -1.866416 2.0 -3.472232 ... 14.0 0.835819 -3.115669 0.790815

Y Y2 X1 ... Z1 Z2 weights

count 999.000 1000.000 999.000 ... 999.000 1000.000 1000.000

mean -0.127 -0.309 1.043 ... 1.040 -0.113 0.495

std 2.305 5.584 0.808 ... 1.307 3.172 0.291

min -6.536 -16.974 0.000 ... -2.825 -11.576 0.000

25% -1.732 -4.029 0.000 ... 0.121 -2.252 0.248

50% -0.211 -0.459 1.000 ... 1.040 -0.064 0.469

75% 1.576 3.528 2.000 ... 1.946 2.028 0.746

max 6.907 17.156 2.000 ... 4.601 11.420 1.000

The dataset has 1,000 observations across 11 columns. The outcome Y has a mean of -0.127 and standard deviation of 2.305, while X1 takes discrete values 0, 1, and 2. A few observations have missing values (1 missing in Y, X1, f1, and Z1), which PyFixest handles automatically by dropping incomplete cases. The group_id variable identifies the group each observation belongs to, and this is the dimension we will control for with fixed effects.

3.2 Visualizing group structure

Before estimating any model, it helps to see how the relationship between X1 and Y varies across groups. If groups have different average levels of Y, standard OLS will mix within-group variation (what we care about) with between-group variation (which may reflect confounders).

fig, ax = plt.subplots(figsize=(10, 6))

groups = data["group_id"].unique()

n_groups = len(groups)

cmap = plt.cm.tab20

for i, g in enumerate(sorted(groups)):

subset = data[data["group_id"] == g]

ax.scatter(subset["X1"], subset["Y"], alpha=0.5, s=20,

color=cmap(i / n_groups),

label=f"Group {g}" if i < 5 else None)

ax.set_xlabel("X1", fontsize=13)

ax.set_ylabel("Y", fontsize=13)

ax.set_title("Outcome (Y) vs Covariate (X1) by Group", fontsize=15, fontweight="bold")

ax.legend(title="Group (first 5)", fontsize=9)

plt.savefig("pyfixest_scatter_by_group.png", dpi=300, bbox_inches="tight",

facecolor=DARK_NAVY, edgecolor=DARK_NAVY, pad_inches=0)

plt.show()

The scatter plot reveals that different groups have distinct average levels of Y — some clusters sit higher and others lower on the vertical axis. Within each group, however, Y tends to decrease as X1 increases. This visual separation between groups is exactly the kind of heterogeneity that fixed effects regression absorbs, allowing us to isolate the within-group relationship between X1 and Y.

4. Simple OLS baseline (no fixed effects)

To establish a benchmark, we first estimate a standard OLS regression of Y on X1 without any fixed effects. The model is:

$$Y_i = \beta_0 + \beta_1 X_{1i} + \epsilon_i$$

In words, we assume the outcome $Y$ is a linear function of $X_1$ plus random noise $\epsilon$. This gives us the overall association, mixing both within-group and between-group variation. We use heteroskedasticity-robust standard errors (HC1) to account for non-constant variance.

fit_ols = pf.feols("Y ~ X1", data=data, vcov="HC1")

print(fit_ols.summary())

Estimation: OLS

Dep. var.: Y, Fixed effects: 0

Inference: HC1

Observations: 998

| Coefficient | Estimate | Std. Error | t value | Pr(>|t|) | 2.5% | 97.5% |

|:--------------|-----------:|-------------:|----------:|-----------:|-------:|--------:|

| Intercept | 0.919 | 0.112 | 8.223 | 0.000 | 0.699 | 1.138 |

| X1 | -1.000 | 0.082 | -12.134 | 0.000 | -1.162 | -0.838 |

---

RMSE: 2.158 R2: 0.123

The pooled OLS estimates a coefficient of -1.000 on X1 (SE = 0.082, p < 0.001), with an R-squared of 0.123. This means that a one-unit increase in X1 is associated with a 1.0-point decrease in Y on average. However, this estimate ignores group-level differences — it could be biased if X1 correlates with unobserved group characteristics. The model explains only 12.3% of the total variation in Y, leaving substantial unexplained heterogeneity. Let us now see how fixed effects change the picture.

5. One-way fixed effects

The following diagram illustrates the core problem fixed effects solve. When an unobserved group characteristic correlates with both the covariate and the outcome, it creates a backdoor path that biases OLS. Fixed effects block this path by absorbing all group-level variation.

graph LR

A["<b>Group Characteristics</b><br/>(unobserved)"] -->|"correlates"| X["<b>X1</b><br/>(covariate)"]

A -->|"affects"| Y["<b>Y</b><br/>(outcome)"]

X -->|"causal effect β = ?"| Y

FE["<b>Fixed Effects</b><br/>(absorbs A)"] -.->|"blocks backdoor"| A

style A fill:#d97757,stroke:#141413,color:#fff

style X fill:#6a9bcc,stroke:#141413,color:#fff

style Y fill:#00d4c8,stroke:#141413,color:#fff

style FE fill:#1a3a8a,stroke:#141413,color:#fff,stroke-dasharray: 5 5

5.1 Absorbing group heterogeneity

Fixed effects regression controls for all time-invariant group characteristics by effectively adding a separate intercept for each group. In PyFixest, we specify fixed effects after a pipe | in the formula. The syntax Y ~ X1 | group_id means: regress Y on X1, absorbing group_id fixed effects. Think of this as asking: “within each group, what is the relationship between X1 and Y?”

fit_fe1 = pf.feols("Y ~ X1 | group_id", data=data, vcov="HC1")

print(fit_fe1.summary())

Estimation: OLS

Dep. var.: Y, Fixed effects: group_id

Inference: HC1

Observations: 998

| Coefficient | Estimate | Std. Error | t value | Pr(>|t|) | 2.5% | 97.5% |

|:--------------|-----------:|-------------:|----------:|-----------:|-------:|--------:|

| X1 | -1.019 | 0.083 | -12.234 | 0.000 | -1.182 | -0.856 |

---

RMSE: 2.141 R2: 0.137 R2 Within: 0.126

With group_id fixed effects absorbed, the coefficient on X1 shifts slightly to -1.019 (SE = 0.083). The within R-squared of 0.126 tells us how much of the within-group variation in Y is explained by X1 after removing group means. Compared to the pooled OLS estimate of -1.000, the fixed effects estimate is similar in this synthetic dataset, suggesting that X1 does not strongly correlate with group-level unobservables here. In real data, the shift can be dramatic — that gap is the omitted variable bias that fixed effects remove.

5.2 Equivalence with dummy variables

Under the hood, fixed effects absorption produces the same point estimates as including explicit dummy variables for each group. PyFixest’s C() operator creates these dummies. The key advantage of absorption is computational: with thousands of groups, estimating thousands of dummy coefficients is slow and memory-intensive, while demeaning is fast.

fit_dummy = pf.feols("Y ~ X1 + C(group_id)", data=data, vcov="HC1")

print(f"X1 coefficient (FE absorption): {fit_fe1.coef()['X1']:.4f}")

print(f"X1 coefficient (dummy vars): {fit_dummy.coef()['X1']:.4f}")

X1 coefficient (FE absorption): -1.0190

X1 coefficient (dummy vars): -1.0190

Both approaches yield identical coefficients of -1.0190 on X1, confirming that FE absorption and dummy variable inclusion are algebraically equivalent. The absorption approach simply avoids estimating and storing the hundreds or thousands of group intercepts that are typically not of interest — what econometricians call nuisance parameters.

6. Understanding fixed effects via manual demeaning

6.1 The within transformation

To build intuition for what fixed effects actually do, we can perform the within transformation manually. For each observation, we subtract its group mean from both Y and X1. This removes all between-group variation, leaving only the deviations from each group’s average. Regressing the demeaned Y on the demeaned X1 recovers the same coefficient as the FE estimator. It is like centering each group at the origin — the only variation left is how individuals within a group differ from their group’s typical level.

The fixed effects estimator solves:

$$\hat{\beta}_{FE} = \left(\sum_{i=1}^{N} \ddot{X}_i' \ddot{X}_i\right)^{-1} \sum_{i=1}^{N} \ddot{X}_i' \ddot{Y}_i$$

where $\ddot{X}_i = X_{it} - \bar{X}_i$ and $\ddot{Y}_i = Y_{it} - \bar{Y}_i$ are the demeaned variables. In words, this says the FE estimator uses only within-group deviations from group means, eliminating any bias from group-level confounders.

# Manual demeaning (within transformation)

data_dm = data.copy()

for col in ["Y", "X1"]:

group_means = data_dm.groupby("group_id")[col].transform("mean")

data_dm[f"{col}_dm"] = data_dm[col] - group_means

fit_demeaned = pf.feols("Y_dm ~ X1_dm", data=data_dm, vcov="HC1")

print(f"X1 coefficient (FE absorption): {fit_fe1.coef()['X1']:.4f}")

print(f"X1 coefficient (manual demean): {fit_demeaned.coef()['X1_dm']:.4f}")

print(f"X1 coefficient (OLS, no FE): {fit_ols.coef()['X1']:.4f}")

X1 coefficient (FE absorption): -1.0190

X1 coefficient (manual demean): -1.0190

X1 coefficient (OLS, no FE): -1.0001

The manual demeaning produces a coefficient of -1.0190, exactly matching the FE absorption result. The pooled OLS gave -1.0001 by comparison. This confirms that fixed effects regression is mathematically equivalent to subtracting group means from every variable before running OLS. The difference between -1.019 (FE) and -1.000 (OLS) reflects the bias introduced by between-group variation that is removed by demeaning.

6.2 Visualizing the demeaning

fig, axes = plt.subplots(1, 2, figsize=(14, 6))

# Left: Raw data

for i, g in enumerate(sorted(groups)[:5]):

subset = data[data["group_id"] == g]

axes[0].scatter(subset["X1"], subset["Y"], alpha=0.4, s=20,

color=cmap(i / n_groups))

axes[0].set_xlabel("X1 (raw)", fontsize=13)

axes[0].set_ylabel("Y (raw)", fontsize=13)

axes[0].set_title("Raw Data: Between + Within Variation", fontsize=13, fontweight="bold")

# Right: Demeaned data

axes[1].scatter(data_dm["X1_dm"], data_dm["Y_dm"], alpha=0.4, s=20, color=STEEL_BLUE)

x_range = np.linspace(data_dm["X1_dm"].min(), data_dm["X1_dm"].max(), 100)

y_pred = fit_demeaned.coef()["X1_dm"] * x_range

axes[1].plot(x_range, y_pred, color=WARM_ORANGE, linewidth=2.5,

label=f"FE slope = {fit_demeaned.coef()['X1_dm']:.3f}")

axes[1].set_xlabel("X1 (demeaned)", fontsize=13)

axes[1].set_ylabel("Y (demeaned)", fontsize=13)

axes[1].set_title("Demeaned Data: Within-Group Variation Only", fontsize=13, fontweight="bold")

axes[1].legend(fontsize=11)

plt.savefig("pyfixest_demeaning.png", dpi=300, bbox_inches="tight",

facecolor=DARK_NAVY, edgecolor=DARK_NAVY, pad_inches=0)

plt.show()

The left panel shows the raw data with groups scattered at different vertical levels — this between-group variation is what confounds the OLS estimate. The right panel shows the demeaned data: all groups are now centered at the origin, and the clear negative slope of -1.019 reflects the pure within-group relationship. This visual makes the FE intuition concrete: by removing group averages, we eliminate confounding from any variable that is constant within groups. Now let us explore how to estimate multiple specifications efficiently.

7. Multiple estimation with stepwise operators

7.1 Cumulative stepwise fixed effects

One of PyFixest’s most powerful features is its formula operators for estimating multiple models in a single call. The csw0() operator adds fixed effects cumulatively: csw0(f1, f2) estimates three models — no FE, then f1 only, then f1 + f2 — in one line. This is far more efficient than writing three separate calls and makes it easy to see how results change as we add controls.

fit_multi = pf.feols("Y ~ X1 | csw0(f1, f2)", data=data, vcov="HC1")

# Print summary for each model

models = fit_multi.all_fitted_models

for key in models:

m = models[key]

print(f"\nModel: {key}")

print(m.summary())

Model: Y~X1

Estimation: OLS

Dep. var.: Y, Fixed effects: 0

Inference: HC1

Observations: 998

| Coefficient | Estimate | Std. Error | t value | Pr(>|t|) |

|:--------------|-----------:|-------------:|----------:|-----------:|

| Intercept | 0.919 | 0.112 | 8.223 | 0.000 |

| X1 | -1.000 | 0.082 | -12.134 | 0.000 |

---

RMSE: 2.158 R2: 0.123

Model: Y~X1|f1

Estimation: OLS

Dep. var.: Y, Fixed effects: f1

Inference: HC1

Observations: 997

| Coefficient | Estimate | Std. Error | t value | Pr(>|t|) |

|:--------------|-----------:|-------------:|----------:|-----------:|

| X1 | -0.949 | 0.067 | -14.094 | 0.000 |

---

RMSE: 1.73 R2: 0.437 R2 Within: 0.161

Model: Y~X1|f1+f2

Estimation: OLS

Dep. var.: Y, Fixed effects: f1+f2

Inference: HC1

Observations: 997

| Coefficient | Estimate | Std. Error | t value | Pr(>|t|) |

|:--------------|-----------:|-------------:|----------:|-----------:|

| X1 | -0.919 | 0.060 | -15.440 | 0.000 |

---

RMSE: 1.441 R2: 0.609 R2 Within: 0.200

The coefficient on X1 shifts from -1.000 (no FE) to -0.949 (with f1) to -0.919 (with f1 + f2), while the overall R-squared jumps from 0.123 to 0.437 to 0.609. Adding f1 alone explains an additional 31 percentage points of variation — a massive improvement that shows how much group-level heterogeneity f1 captures. Adding f2 on top of f1 brings R-squared to 0.609, meaning the two fixed effect dimensions together account for over 60% of the total variation in Y. The standard error on X1 also shrinks from 0.082 to 0.060, reflecting the precision gain from reducing residual noise.

| Specification | X1 Coef. | SE | R-squared | R-squared Within |

|---|---|---|---|---|

| No FE | -1.000 | 0.082 | 0.123 | — |

| FE: f1 | -0.949 | 0.067 | 0.437 | 0.161 |

| FE: f1 + f2 | -0.919 | 0.060 | 0.609 | 0.200 |

7.2 Visualizing coefficient stability

The table above shows the numbers, but a figure makes the comparison more immediate. Plotting the coefficient with its 95% confidence interval across specifications reveals both the stability of the point estimate and the precision gain from adding fixed effects.

# Coefficient comparison across specifications

model_names = ["No FE", "FE: f1", "FE: f1 + f2"]

coefs = [models[k].coef()["X1"] for k in models]

ses = [models[k].se()["X1"] for k in models]

fig, ax = plt.subplots(figsize=(8, 5))

y_pos = np.arange(len(model_names))

ax.barh(y_pos, coefs, xerr=[1.96 * s for s in ses], height=0.5,

color=[STEEL_BLUE, WARM_ORANGE, TEAL], edgecolor=DARK_NAVY, capsize=5)

ax.set_yticks(y_pos)

ax.set_yticklabels(model_names, fontsize=12)

ax.set_xlabel("Coefficient on X1", fontsize=13)

ax.set_title("Effect of X1 Across Fixed Effect Specifications", fontsize=14, fontweight="bold")

ax.axvline(x=0, color=NEAR_BLACK, linewidth=0.8, linestyle="--", alpha=0.5)

plt.savefig("pyfixest_coef_comparison.png", dpi=300, bbox_inches="tight",

facecolor=DARK_NAVY, edgecolor=DARK_NAVY, pad_inches=0)

plt.show()

The coefficient comparison chart shows that the point estimate on X1 remains stable around -1.0 across all three specifications, with confidence intervals narrowing as we add fixed effects. This stability suggests the estimate is robust to the inclusion of group-level controls. In applied research, large shifts across specifications would signal omitted variable concerns, making this type of comparison essential for assessing credibility.

8. Inference: choosing the right standard errors

8.1 Comparing standard error estimators

The choice of standard errors can dramatically change statistical inference, even when point estimates remain the same. Standard (iid) errors assume all observations are independent and identically distributed. Heteroskedasticity-robust (HC1) errors relax the constant-variance assumption. Cluster-robust (CRV) errors account for arbitrary correlation within groups — essential when observations within a group are not independent, like repeated measurements of the same individual. Think of it like estimating average height: if you measure the same person ten times, those ten measurements are not ten independent observations, and your standard error should reflect that.

se_types = {

"iid": "iid",

"HC1 (robust)": "HC1",

"CRV1 (group_id)": {"CRV1": "group_id"},

"CRV1 (group_id + f2)": {"CRV1": "group_id + f2"},

"CRV3 (group_id)": {"CRV3": "group_id"},

}

print(f"{'SE Type':<22} {'SE(X1)':<10} {'t-stat':<10} {'p-value':<10}")

print("-" * 52)

for name, vcov in se_types.items():

fit_tmp = pf.feols("Y ~ X1 | group_id", data=data, vcov=vcov)

print(f"{name:<22} {fit_tmp.se()['X1']:<10.4f} "

f"{fit_tmp.tstat()['X1']:<10.3f} {fit_tmp.pvalue()['X1']:<10.4f}")

SE Type SE(X1) t-stat p-value

----------------------------------------------------

iid 0.0858 -11.875 0.0000

HC1 (robust) 0.0833 -12.234 0.0000

CRV1 (group_id) 0.1172 -8.696 0.0000

CRV1 (group_id + f2) 0.1207 -8.445 0.0000

CRV3 (group_id) 0.1247 -8.174 0.0000

The standard error on X1 ranges from 0.0833 (HC1) to 0.1247 (CRV3), a 50% increase depending on the assumption about error correlation. While all p-values remain below 0.001 in this case, the t-statistic drops from 12.2 to 8.2 — a substantial difference that could determine significance for weaker effects. Cluster-robust SEs (CRV1) inflate to 0.1172 because they account for within-group correlation. The CRV3 estimator, which provides a more conservative finite-sample correction, gives the largest SE of 0.1247. In practice, you should cluster at the level where you believe errors are correlated.

8.2 Visualizing the SE tradeoff

fig, ax = plt.subplots(figsize=(9, 5))

se_names = list(se_types.keys())

se_vals = []

for name, vcov in se_types.items():

fit_tmp = pf.feols("Y ~ X1 | group_id", data=data, vcov=vcov)

se_vals.append(fit_tmp.se()["X1"])

colors = [STEEL_BLUE, WARM_ORANGE, TEAL, "#e8956a", "#f0a88c"]

bars = ax.bar(range(len(se_names)), se_vals, color=colors, edgecolor=DARK_NAVY, width=0.6)

ax.set_xticks(range(len(se_names)))

ax.set_xticklabels(se_names, rotation=25, ha="right", fontsize=10)

ax.set_ylabel("Standard Error of X1", fontsize=13)

ax.set_title("Standard Errors Under Different Assumptions", fontsize=14, fontweight="bold")

for i, v in enumerate(se_vals):

ax.text(i, v + 0.002, f"{v:.4f}", ha="center", fontsize=10, fontweight="bold")

plt.savefig("pyfixest_se_comparison.png", dpi=300, bbox_inches="tight",

facecolor=DARK_NAVY, edgecolor=DARK_NAVY, pad_inches=0)

plt.show()

The bar chart makes the progression vivid: moving from iid to cluster-robust standard errors increases uncertainty by nearly 50%. The iid and HC1 estimates are similar because heteroskedasticity is not a major concern here. The real jump occurs when we account for within-group correlation (CRV1), and the CRV3 bias-corrected estimator is the most conservative. For applied work with grouped data, defaulting to cluster-robust errors is the safest choice — underestimating standard errors leads to falsely significant results.

9. Two-way fixed effects

When data has two grouping dimensions — for example, firms and years, or workers and occupations — two-way fixed effects absorb unobserved heterogeneity along both dimensions. In PyFixest, we simply list both FE variables after the pipe: Y ~ X1 + X2 | f1 + f2. This absorbs all factors that are constant within each level of f1 and each level of f2.

fit_twoway = pf.feols("Y ~ X1 + X2 | f1 + f2", data=data, vcov="HC1")

print(fit_twoway.summary())

Estimation: OLS

Dep. var.: Y, Fixed effects: f1+f2

Inference: HC1

Observations: 997

| Coefficient | Estimate | Std. Error | t value | Pr(>|t|) | 2.5% | 97.5% |

|:--------------|-----------:|-------------:|----------:|-----------:|-------:|--------:|

| X1 | -0.924 | 0.056 | -16.375 | 0.000 | -1.035 | -0.813 |

| X2 | -0.174 | 0.015 | -11.246 | 0.000 | -0.204 | -0.144 |

---

RMSE: 1.346 R2: 0.659 R2 Within: 0.303

Adding both f1 and f2 as fixed effects plus the additional covariate X2 yields an R-squared of 0.659 and a within R-squared of 0.303. The coefficient on X1 is -0.924 (SE = 0.056) and X2 is -0.174 (SE = 0.015), both highly significant. The within R-squared of 0.303 means that X1 and X2 together explain about 30% of the variation in Y after absorbing both dimensions of fixed effects — a substantial improvement over the 20% with X1 alone in the previous section.

10. Instrumental variables with fixed effects

Sometimes the explanatory variable itself is endogenous — correlated with the error term due to measurement error, simultaneity, or omitted variables that fixed effects do not capture. Instrumental variables (IV) estimation addresses this by using external variables (instruments) that affect the outcome only through the endogenous variable. Think of instruments as a natural experiment embedded in the data: Z affects X but has no direct path to Y, so any association between Z and Y must flow through X. In PyFixest, the IV syntax uses a second pipe: Y2 ~ 1 | f1 + f2 | X1 ~ Z1 + Z2. This reads: outcome Y2, no exogenous controls (just the intercept 1), fixed effects f1 + f2, and endogenous variable X1 instrumented by Z1 and Z2.

The IV estimator recovers the coefficient on X1 by first predicting X1 using the instruments, then using these predictions in the second-stage regression:

$$\text{First stage: } X_1 = \pi_0 + \pi_1 Z_1 + \pi_2 Z_2 + \alpha_i + \gamma_t + \nu$$

$$\text{Second stage: } Y_2 = \beta X_1^{predicted} + \alpha_i + \gamma_t + \epsilon$$

In words, the first stage isolates the variation in X1 that is driven by the instruments Z1 and Z2, stripping away the endogenous component. The second stage then uses only this “clean” variation to estimate the effect of X1 on Y2. Here, $\alpha_i$ corresponds to the f1 fixed effects, $\gamma_t$ corresponds to the f2 fixed effects, and $\beta$ is the causal parameter of interest that we recover from the X1 coefficient in PyFixest’s output.

fit_iv = pf.feols("Y2 ~ 1 | f1 + f2 | X1 ~ Z1 + Z2", data=data)

print(fit_iv.summary())

print(f"\nFirst-stage F-statistic: {fit_iv._f_stat_1st_stage:.2f}")

Estimation: IV

Dep. var.: Y2, Fixed effects: f1+f2

Inference: iid

Observations: 998

| Coefficient | Estimate | Std. Error | t value | Pr(>|t|) | 2.5% | 97.5% |

|:--------------|-----------:|-------------:|----------:|-----------:|-------:|--------:|

| X1 | -1.600 | 0.336 | -4.768 | 0.000 | -2.259 | -0.942 |

---

First-stage F-statistic: 311.54

The IV estimate of X1 is -1.600 (SE = 0.336), substantially larger in magnitude than the OLS estimate of approximately -1.0. This divergence suggests that the OLS coefficient on X1 is attenuated — a classic sign of measurement error or endogeneity that biases OLS toward zero. The first-stage F-statistic of 311.54 is well above the conventional threshold of 10, indicating that Z1 and Z2 are strong instruments. Strong instruments mean the IV estimate is reliable; with weak instruments, IV can perform worse than OLS. Note that with heterogeneous treatment effects, IV identifies the Local Average Treatment Effect (LATE) — the effect for units whose treatment status is shifted by the instruments — rather than the Average Treatment Effect (ATE) for the entire population.

11. Panel data application: wage determinants

11.1 The wage panel: variables and structure

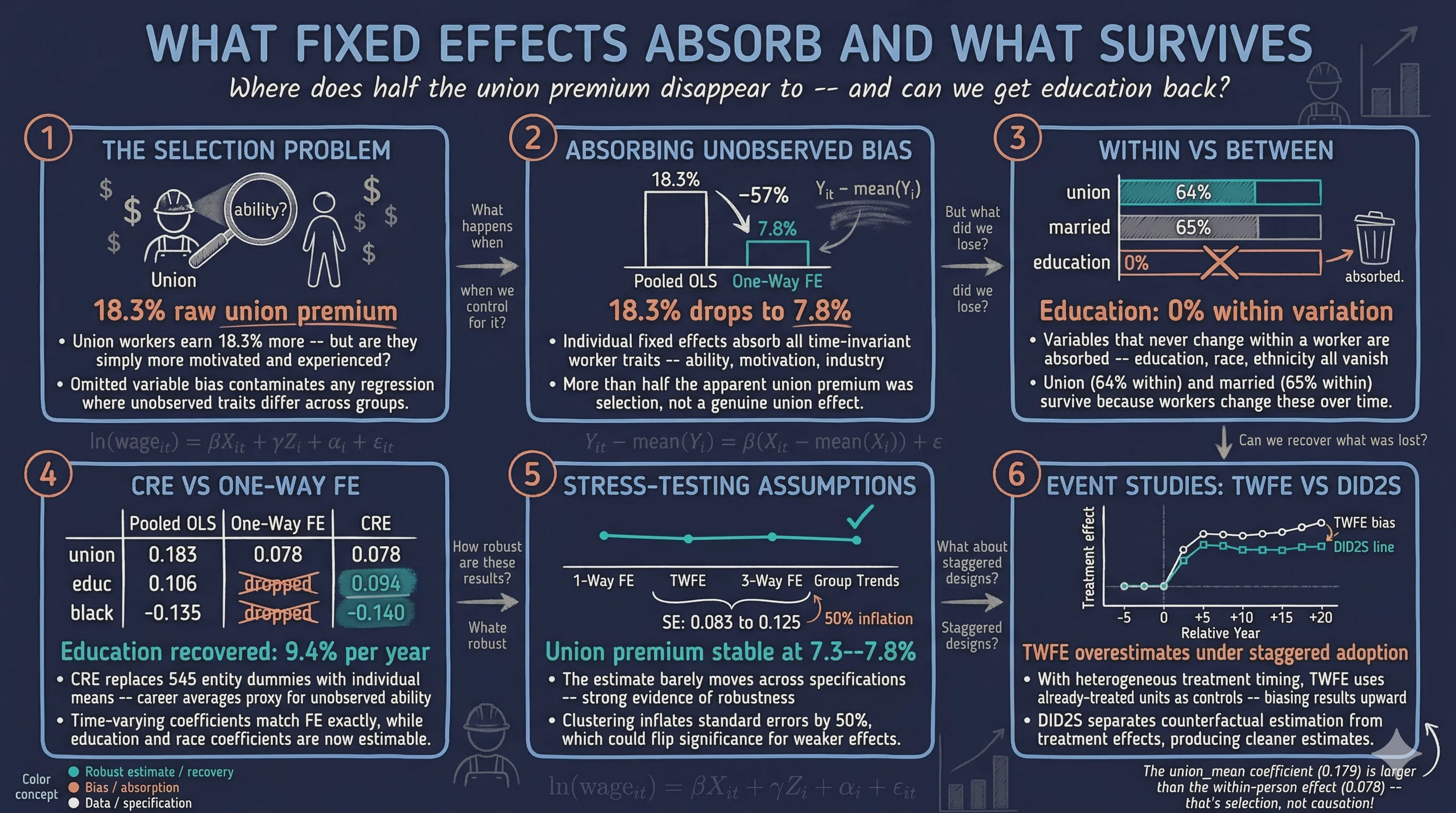

To see fixed effects in action with real data, we analyze the Vella and Verbeek (1998) panel of 545 young men observed over 8 years (1980–1987) from the National Longitudinal Survey of Youth (NLSY). This dataset, used in many econometrics textbooks, is ideal for studying wage determinants because it tracks the same workers as they enter the labor market, gain experience, change jobs, and make decisions about union membership and marriage. The key challenge is that unobserved individual ability differs across workers and correlates with both wages and these covariates — a classic case for one-way fixed effects.

url = "https://raw.githubusercontent.com/bashtage/linearmodels/main/linearmodels/datasets/wage_panel/wage_panel.csv.bz2"

wage_df = pd.read_csv(url, compression="bz2")

print(f"Wage panel shape: {wage_df.shape}")

print(wage_df.describe().round(3))

Wage panel shape: (4360, 12)

nr year black exper hisp ... educ union lwage expersq occupation

count 4360.000 4360.000 4360.000 4360.000 4360.000 ... 4360.000 4360.000 4360.000 4360.000 4360.000

mean 5262.059 1983.500 0.116 6.500 0.161 ... 11.768 0.244 1.649 50.425 4.989

std 3496.150 2.292 0.320 2.292 0.367 ... 1.353 0.430 0.533 40.782 2.320

min 13.000 1980.000 0.000 1.000 0.000 ... 3.000 0.000 -3.579 1.000 1.000

25% 2329.000 1981.750 0.000 4.750 0.000 ... 11.000 0.000 1.351 16.000 4.000

50% 4569.000 1983.500 0.000 6.500 0.000 ... 12.000 0.000 1.671 36.000 5.000

75% 8406.000 1985.250 0.000 8.250 0.000 ... 12.000 0.000 1.991 81.000 6.000

max 12548.000 1987.000 1.000 12.000 1.000 ... 16.000 1.000 4.052 324.000 9.000

The panel contains 4,360 observations (545 individuals over 8 years) with 12 variables. Before running any model, it is important to understand how each variable is defined and measured.

Outcome variable:

lwage— the natural logarithm of hourly wage. The log transformation means that coefficients are interpreted as approximate percentage changes. The mean of 1.649 corresponds to about \$5.20 per hour in 1980s dollars ($e^{1.649} \approx 5.20$). The standard deviation of 0.533 indicates substantial wage dispersion: the gap between a worker at the 25th percentile (\$3.86/hr) and the 75th percentile (\$7.32/hr) is roughly a doubling of wages.

Time-varying covariates (change within a worker over time):

hours— annual hours worked. Mean of 2,191 (roughly 42 hours per week for 52 weeks). Ranges from 120 to 4,992, capturing both part-time spells and heavy overtime. We include hours to control for labor supply differences that affect hourly wage calculations.union— binary indicator (1 = covered by a union contract in the current year, 0 = not covered). About 24.4% of person-year observations are union-covered. Workers can move in and out of union jobs across years, and this within-worker variation in union status is what one-way FE use to identify the union wage premium.married— binary indicator (1 = currently married, 0 = not married). About 43.9% of observations are married. Since these are young men tracked from their early twenties, many transition from single to married during the panel, providing within-worker variation.exper— years of potential labor market experience, defined as age minus years of education minus 6. Ranges from 1 to 12 years. In this balanced panel where every worker is observed in every year, experience increases by exactly 1 each year, making it perfectly collinear with entity + year fixed effects. We therefore useexpersqinstead in FE models.expersq— experience squared ($exper^2$). Captures the well-documented concavity in the experience–earnings profile: wages rise with experience but at a diminishing rate. Unlikeexper, the squared term is a nonlinear function of time, so it is not collinear with entity + year FE and can be estimated.occupation— occupational category, coded 1 through 9 (9 distinct categories). Workers can and do switch occupations across years. This variable can be used as an additional fixed effect dimension.

Time-invariant covariates (fixed for each worker across all years):

educ— years of completed schooling at the start of the panel. Mean of 11.77 years (just below a high school diploma), ranging from 3 to 16 years. Because the sample tracks young men who have already finished their schooling, education does not change over time. The median of 12 years (exactly a high school diploma) and the 75th percentile of 12 years indicate that most workers in this sample have a high school education, with a smaller group holding college degrees.black— binary indicator (1 = Black, 0 = non-Black). About 11.6% of workers are Black. Because race does not change over time, one-way FE absorb any wage differences associated with being Black.hisp— binary indicator (1 = Hispanic, 0 = non-Hispanic). About 16.1% of workers are Hispanic. Likeblack, this is absorbed by one-way FE.

Panel identifiers:

nr— unique worker identifier (545 distinct workers). This defines the entity dimension for fixed effects.year— calendar year, taking values 1980 through 1987. The panel is balanced: every worker appears in every year, giving exactly $545 \times 8 = 4,360$ observations.

The distinction between time-varying and time-invariant variables is the most consequential feature of this dataset for fixed effects analysis. Time-invariant variables will be perfectly collinear with entity dummies and cannot be estimated under one-way FE. Time-varying variables survive the within transformation and their effects can be identified. We verify this classification empirically:

invariance = wage_df.groupby("nr")[["educ", "black", "hisp"]].nunique()

print(f"Max unique values per worker:")

print(invariance.max())

Max unique values per worker:

educ 1

black 1

hisp 1

dtype: int64

Each worker has exactly one value of education, race, and ethnicity across all eight years — confirming these are truly time-invariant. By contrast, occupation is time-varying:

occ_changes = wage_df.groupby("nr")["occupation"].nunique()

print(f"Workers who change occupation: {(occ_changes > 1).sum()} / {len(occ_changes)}")

Workers who change occupation: 484 / 545

Nearly 89% of workers switch occupations at least once during the panel. This high rate of switching makes occupation a valid candidate for a fixed effect dimension of its own (Section 11.5). By contrast, a variable like education, which never changes within a worker, would produce a column of zeros after demeaning and must be dropped — a point we return to in Sections 11.3 and 11.4.

11.2 Within vs between variation

Before estimating any model, it helps to decompose the variation in each variable into between-worker variation (permanent differences across workers) and within-worker variation (changes over a worker’s career). This decomposition foreshadows what one-way fixed effects can and cannot estimate.

cols = ["lwage", "hours", "union", "married", "expersq", "educ"]

between = wage_df.groupby("nr")[cols].mean().std()

for col in cols:

wage_df[f"{col}_within"] = wage_df[col] - wage_df.groupby("nr")[col].transform("mean")

within = wage_df[[f"{c}_within" for c in cols]].std()

variation = pd.DataFrame({"Between": between, "Within": within}).round(4)

print(variation)

Between Within

lwage 0.3907 0.3623

hours 381.7831 418.6057

union 0.3294 0.2760

married 0.3766 0.3236

expersq 26.3513 31.1431

educ 1.7476 0.0000

The raw standard deviations differ wildly across variables (hours is in the hundreds, union is a fraction), so we normalize by computing each variable’s within share — the fraction of total variation that comes from within-worker changes over time. This puts all variables on the same 0–100% scale:

total = np.sqrt(between**2 + within**2)

within_share = (within / total).fillna(0) # educ: 0/0 → 0

between_share = 1 - within_share

fig, ax = plt.subplots(figsize=(10, 5))

y_pos = np.arange(len(cols))

bar_height = 0.55

# Stacked horizontal bars: between (left) + within (right) = 100%

ax.barh(y_pos, between_share.values, bar_height,

label="Between (cross-worker)", color=STEEL_BLUE, edgecolor=DARK_NAVY)

ax.barh(y_pos, within_share.values, bar_height, left=between_share.values,

label="Within (over career)", color=WARM_ORANGE, edgecolor=DARK_NAVY)

plt.savefig("pyfixest_within_between.png", dpi=300, bbox_inches="tight",

facecolor=DARK_NAVY, edgecolor=DARK_NAVY, pad_inches=0)

plt.show()

The decomposition reveals a critical pattern. Education is 100% between-worker variation — its within share is exactly 0% — because no worker changes their education level during the panel. This means one-way FE literally cannot estimate education’s effect: the demeaned education column is all zeros. Log wages have a 68% within share and 32% between share, meaning most wage variation comes from changes over a worker’s career rather than permanent differences across workers. Variables with substantial within shares — union (64%), married (65%), hours (74%), expersq (76%) — can be estimated under one-way FE because they change over a worker’s career. The higher the within share, the more statistical power one-way FE retains for that variable.

11.3 The Mincer equation and its panel extensions

Before estimating any models, it helps to lay out the econometric framework that organizes all subsequent specifications. The classic Mincer equation (Mincer, 1974) is the workhorse model of labor economics:

$$\ln(wage_i) = \beta_0 + \beta_1 educ_i + \beta_2 exper_i + \beta_3 exper_i^2 + \epsilon_i$$

This log-linear specification models wages as a function of years of schooling and experience, with experience entering quadratically to capture concave returns — each additional year of experience raises wages, but by a diminishing amount. It is a cross-sectional model, estimating the average relationship across all workers at a single point in time.

The extended Mincer equation adds controls for union membership, marital status, hours worked, and demographic characteristics:

$$\ln(wage_{it}) = \beta_0 + \beta_1 educ_i + \beta_2 expersq_{it} + \beta_3 union_{it} + \beta_4 married_{it} + \beta_5 hours_{it} + \beta_6 black_i + \beta_7 hisp_i + \epsilon_{it}$$

The panel FE extension replaces explicit controls for time-invariant characteristics with entity and time fixed effects:

$$\ln(wage_{it}) = \beta X_{it} + \gamma Z_i + \alpha_i + \delta_t + \epsilon_{it}$$

where $X_{it}$ denotes time-varying covariates (union, married, hours, experience), $Z_i$ denotes time-invariant characteristics (education, race), $\alpha_i$ captures one-way fixed effects (one intercept per worker), and $\delta_t$ captures year fixed effects. The key insight: when we include $\alpha_i$, the time-invariant variables $Z_i$ become perfectly collinear with the entity dummies and are absorbed. We gain protection against omitted variable bias from all unobserved time-invariant confounders, but we lose the ability to estimate $\gamma$.

The CRE/Mundlak extension — the Mundlak (1978) device — offers a way to recover $\gamma$:

$$\ln(wage_{it}) = \beta X_{it} + \gamma Z_i + \pi \bar{X}_i + \epsilon_{it}$$

where $\bar{X}_i$ are individual means of the time-varying variables. This replaces entity dummies with individual means, which model the correlation between unobserved heterogeneity and the covariates. The result: $\hat{\beta} \approx \hat{\beta}_{FE}$ for the time-varying variables, while $\gamma$ is now estimable because we no longer include entity dummies that absorb it.

Sections 11.4–11.7 estimate these models progressively: pooled OLS and one-way FE (11.4), two-way and three-way FE (11.5), group-specific time trends (11.6), and CRE/Mundlak (11.7).

11.4 From pooled OLS to one-way FE: the education tradeoff

We begin with the extended Mincer equation estimated by pooled OLS, which includes both time-varying and time-invariant variables:

fit_pooled = pf.feols(

"lwage ~ educ + expersq + union + married + hours + black + hisp",

data=wage_df, vcov="HC1"

)

print(fit_pooled.summary())

Estimation: OLS

Dep. var.: lwage, Fixed effects: 0

Inference: HC1

Observations: 4360

| Coefficient | Estimate | Std. Error | t value | Pr(>|t|) | 2.5% | 97.5% |

|:--------------|-----------:|-------------:|----------:|-----------:|-------:|--------:|

| Intercept | 0.265 | 0.069 | 3.823 | 0.000 | 0.129 | 0.402 |

| educ | 0.106 | 0.005 | 22.924 | 0.000 | 0.097 | 0.115 |

| expersq | 0.003 | 0.000 | 16.930 | 0.000 | 0.003 | 0.004 |

| union | 0.183 | 0.016 | 11.205 | 0.000 | 0.151 | 0.215 |

| married | 0.141 | 0.015 | 9.308 | 0.000 | 0.111 | 0.171 |

| hours | -0.000 | 0.000 | -3.139 | 0.002 | -0.000 | -0.000 |

| black | -0.135 | 0.024 | -5.549 | 0.000 | -0.182 | -0.087 |

| hisp | 0.013 | 0.020 | 0.670 | 0.503 | -0.025 | 0.052 |

---

RMSE: 0.484 R2: 0.175

Pooled OLS estimates a 10.6% return to each year of education, an 18.3% union premium, and a 14.1% marriage premium. Black workers earn about 13.5% less, while the Hispanic coefficient is small and insignificant. The R-squared is 0.175 — these variables explain less than a fifth of wage variation.

Now we estimate the one-way FE model, which absorbs all time-invariant worker characteristics:

fit_entity = pf.feols("lwage ~ expersq + union + married + hours | nr",

data=wage_df, vcov={"CRV1": "nr"})

print(fit_entity.summary())

Estimation: OLS

Dep. var.: lwage, Fixed effects: nr

Inference: CRV1

Observations: 4360

| Coefficient | Estimate | Std. Error | t value | Pr(>|t|) | 2.5% | 97.5% |

|:--------------|-----------:|-------------:|----------:|-----------:|-------:|--------:|

| expersq | 0.004 | 0.000 | 16.537 | 0.000 | 0.003 | 0.004 |

| union | 0.078 | 0.024 | 3.319 | 0.001 | 0.032 | 0.125 |

| married | 0.115 | 0.022 | 5.217 | 0.000 | 0.071 | 0.158 |

| hours | -0.000 | 0.000 | -3.807 | 0.000 | -0.000 | -0.000 |

---

RMSE: 0.335 R2: 0.605 R2 Within: 0.145

One-way fixed effects dramatically improve model fit: R-squared jumps from 0.175 (pooled OLS) to 0.605, meaning worker-level heterogeneity accounts for over 40 percentage points of explained variation. The union premium drops from 18.3% to 7.8% (SE = 0.024) — more than half the pooled estimate was driven by selection (workers who join unions differ systematically from those who do not). The marriage premium falls from 14.1% to 11.5% (SE = 0.022), a smaller reduction suggesting that marital status is less confounded by unobserved ability. The expersq coefficient of 0.004 captures the concavity of the experience–earnings profile within workers over time. Notice that educ, black, and hisp are absent: these time-invariant variables are perfectly collinear with the 545 worker dummies and cannot be estimated under one-way FE.

To see what happens when we try to include a time-invariant variable alongside one-way FE:

import warnings

with warnings.catch_warnings(record=True) as w:

warnings.simplefilter("always")

fit_educ = pf.feols("lwage ~ expersq + union + married + educ | nr",

data=wage_df, vcov={"CRV1": "nr"})

print(f"Coefficients estimated: {list(fit_educ.coef().index)}")

Coefficients estimated: ['expersq', 'union', 'married']

Education is silently dropped. This is not a bug — it is a fundamental consequence of the within transformation (Section 6):

$$\ddot{educ}_{it} = educ_i - \bar{educ}_i = 0 \quad \text{for all } t$$

Because a worker’s education does not change over the eight years of the panel, the demeaned value is exactly zero for every observation. A column of zeros is perfectly collinear with the entity dummies, so it must be dropped. The same applies to black and hisp.

| Variable | Pooled OLS | One-Way FE |

|---|---|---|

| educ | 0.106 | dropped |

| expersq | 0.003 | 0.004 |

| union | 0.183 | 0.078 |

| married | 0.141 | 0.115 |

| hours | -0.000 | -0.000 |

| black | -0.135 | dropped |

| hisp | 0.013 | dropped |

| R-squared | 0.175 | 0.605 |

This table crystallizes the fundamental tradeoff. Pooled OLS estimates everything — education, race, union, marriage — but its estimates are biased by unobserved ability. One-Way FE eliminates the ability bias, and the union premium drops from 18.3% to 7.8%, revealing that more than half the raw association was selection. But the price is steep: education, Black, and Hispanic are all absorbed into the individual intercepts. We cannot estimate the return to schooling or the racial wage gap under one-way FE. Sections 11.5–11.6 push further with additional FE dimensions, and Section 11.7 shows how CRE partially resolves this tradeoff.

11.5 Two-way and three-way fixed effects

Adding year fixed effects to one-way FE creates a two-way FE (TWFE) model that absorbs both individual heterogeneity and common time trends:

fit_panel = pf.feols("lwage ~ expersq + union + married + hours | nr + year",

data=wage_df, vcov={"CRV1": "nr + year"})

We can go further by adding occupation as a third fixed effect dimension. As we saw in Section 11.1, nearly 89% of workers switch occupations during the panel, so occupation is a valid time-varying dimension:

fit_threeway = pf.feols(

"lwage ~ expersq + union + married + hours | nr + year + C(occupation)",

data=wage_df, vcov={"CRV1": "nr"}

)

| Variable | Pooled OLS | One-Way FE | Two-Way FE | Three-Way FE |

|---|---|---|---|---|

| expersq | 0.003 | 0.004 | -0.006 | -0.006 |

| union | 0.183 | 0.078 | 0.073 | 0.075 |

| married | 0.141 | 0.115 | 0.048 | 0.047 |

| hours | -0.000 | -0.000 | -0.000 | -0.000 |

| R-squared | 0.175 | 0.605 | 0.631 | 0.632 |

fig, axes = plt.subplots(2, 2, figsize=(12, 8))

panel_models = {"Pooled OLS": fit_pooled, "One-Way FE": fit_entity,

"Two-Way FE": fit_panel, "Three-Way FE": fit_threeway}

panel_vars = ["expersq", "union", "married", "hours"]

panel_colors = [STEEL_BLUE, WARM_ORANGE, TEAL, "#e8956a"]

for idx, var in enumerate(panel_vars):

ax = axes.flatten()[idx]

model_names_p = list(panel_models.keys())

coefs_p = [panel_models[m].coef()[var] for m in model_names_p]

ses_p = [panel_models[m].se()[var] for m in model_names_p]

ax.bar(range(4), coefs_p, yerr=[1.96 * s for s in ses_p],

color=panel_colors, edgecolor=DARK_NAVY, width=0.5, capsize=4)

ax.set_xticks(range(4))

ax.set_xticklabels(model_names_p, fontsize=8, rotation=15)

ax.set_title(var, fontsize=12, fontweight="bold")

ax.axhline(y=0, color=NEAR_BLACK, linewidth=0.5, linestyle="--", alpha=0.5)

fig.suptitle("Coefficient Estimates Across FE Specifications",

fontsize=14, fontweight="bold", y=1.02)

plt.savefig("pyfixest_wage_extended.png", dpi=300, bbox_inches="tight",

facecolor=DARK_NAVY, edgecolor=DARK_NAVY, pad_inches=0)

plt.show()

The results show diminishing returns to additional FE dimensions. The big action was one-way FE: R-squared jumps from 0.175 to 0.605, and the union premium drops from 18.3% to 7.8%. Adding year effects (TWFE) pushes R-squared to 0.631 and the union premium stabilizes at 7.3%. Adding occupation as a third dimension barely moves anything — R-squared rises to 0.632 and the union premium is 7.5%. The expersq coefficient flips sign with TWFE (-0.006) because year effects absorb common trends in experience and wages. The stability of the union and marriage coefficients across the last three specifications suggests these estimates are robust to additional controls for time trends and occupational sorting.

11.6 Interactive fixed effects

Sections 11.4–11.5 used additive fixed effects (nr + year), where every individual shares the same set of year effects. Interactive (or interacted) fixed effects generalize this by allowing one FE dimension to vary across levels of another — producing group-specific intercepts for each time period. Instead of a single set of year dummies shared by all workers, we estimate separate year effects for each demographic group.

Why does this matter? Black and non-Black workers may face different labor market trends during the 1980s. If macroeconomic shocks hit these groups differently, a common set of year effects would be misspecified. We can test this by allowing year effects to vary by race:

$$\ln(wage_{it}) = \beta X_{it} + \alpha_i + \gamma_{t,g(i)} + \epsilon_{it}$$

where $g(i) \in \{Black, non\text{-}Black\}$, so we estimate separate year effects for each racial group.

Pyfixest implements interactive FE with the caret operator (^): the syntax year^black in the fixed-effects slot creates a separate year dummy for each value of black. This mirrors R’s fixest package. The equivalent manual approach is to concatenate the columns (wage_df["year_black"] = wage_df["year"].astype(str) + "_" + wage_df["black"].astype(str)) and absorb the resulting string variable, but the caret operator is preferred because it keeps the interaction structure visible in the formula.

# Pyfixest caret operator for interacted fixed effects

fit_gtrends = pf.feols("lwage ~ expersq + union + married + hours | nr + year^black",

data=wage_df, vcov={"CRV1": "nr"})

print(fit_gtrends.summary())

Estimation: OLS

Dep. var.: lwage, Fixed effects: nr+year^black

Inference: CRV1

Observations: 4360

| Coefficient | Estimate | Std. Error | t value | Pr(>|t|) | 2.5% | 97.5% |

|:--------------|----------: |------------: |--------: |---------: |-----: |------: |

| expersq | -0.006 | 0.001 | -5.878 | 0.000 | -0.008 | -0.004 |

| union | 0.074 | 0.024 | 3.129 | 0.002 | 0.028 | 0.121 |

| married | 0.045 | 0.020 | 2.262 | 0.024 | 0.006 | 0.084 |

| hours | -0.000 | 0.000 | -0.393 | 0.694 | -0.001 | 0.001 |

| Variable | Two-Way FE (additive) | Interactive FE (year × race) |

|---|---|---|

| expersq | -0.006 | -0.006 |

| union | 0.073 | 0.074 |

| married | 0.048 | 0.045 |

| hours | -0.000 | -0.000 |

fig, ax = plt.subplots(figsize=(9, 5))

vars_plot = ["expersq", "union", "married", "hours"]

x = np.arange(len(vars_plot))

width = 0.35

twfe_coefs = [fit_panel.coef()[v] for v in vars_plot]

gtrend_coefs = [fit_gtrends.coef()[v] for v in vars_plot]

ax.bar(x - width/2, twfe_coefs, width, label="Two-Way FE", color=STEEL_BLUE, edgecolor=DARK_NAVY)

ax.bar(x + width/2, gtrend_coefs, width, label="Interactive FE", color=WARM_ORANGE, edgecolor=DARK_NAVY)

ax.set_xticks(x)

ax.set_xticklabels(vars_plot, fontsize=11)

ax.set_ylabel("Coefficient Estimate", fontsize=13)

ax.set_title("Additive vs Interactive Fixed Effects", fontsize=14, fontweight="bold")

ax.legend(fontsize=11)

ax.axhline(y=0, color=NEAR_BLACK, linewidth=0.5, linestyle="--", alpha=0.5)

plt.savefig("pyfixest_group_trends.png", dpi=300, bbox_inches="tight",

facecolor=DARK_NAVY, edgecolor=DARK_NAVY, pad_inches=0)

plt.show()

The coefficients are nearly identical under both specifications. Moving from additive to interactive fixed effects barely changes the estimated returns to union membership (7.3% → 7.4%), marriage (4.8% → 4.5%), or experience. This stability indicates that year effects are similar across racial groups — the additive TWFE specification is not misspecified by imposing common year effects. The interactive model uses 545 one-way FE plus 16 group-year FE (8 years × 2 groups) = 561 FE parameters to explain 4,360 observations — well short of saturation. Had the coefficients shifted substantially, that would have signaled that Black and non-Black workers face sufficiently different macro trends to warrant group-specific year effects, and that the standard additive TWFE was masking this heterogeneity.

11.7 Recovering time-invariant effects: the CRE/Mundlak approach

Sections 11.4–11.6 revealed a fundamental tradeoff in panel econometrics. One-way FE eliminate omitted variable bias from all unobserved time-invariant confounders — a powerful guarantee — but they absorb education, race, and ethnicity in the process. Pooled OLS estimates coefficients for everything, but those estimates are biased whenever unobserved worker traits correlate with the covariates. We want the best of both worlds: the bias protection of FE with the ability to estimate time-invariant effects.

Imagine you could describe each worker’s “type” not with a unique ID but with a summary of their career trajectory — their average union participation rate, average hours worked, average marital status, and so on. Two workers with similar career averages are arguably similar in unobserved ways too: a worker who spends 80% of their career in a union likely differs systematically from one who never joins. The Correlated Random Effects (CRE) model — also called the Mundlak (1978) device — operationalizes this intuition by replacing the 545 entity dummies with a handful of individual-mean variables that capture the same correlation structure.

The CRE equation. Recall from Section 11.3 that the CRE equation replaces entity dummies $\alpha_i$ with individual means $\bar{X}_i$ of the time-varying variables:

$$\ln(wage_{it}) = \beta X_{it} + \gamma Z_i + \pi \bar{X}_i + \epsilon_{it}$$

In words, this equation says that a worker’s log wage depends on three components: (1) their current values of time-varying covariates ($X_{it}$), (2) their permanent characteristics ($Z_i$ like education and race), and (3) a set of correction terms ($\bar{X}_i$) that capture the average level of each time-varying variable across their career. In our code, $X_{it}$ corresponds to expersq, union, married, and hours in each year; $Z_i$ corresponds to educ, black, and hisp; and $\bar{X}_i$ corresponds to the *_mean columns we compute below.

Why does including $\bar{X}_i$ work? The individual means proxy for the unobserved individual effect $\alpha_i$. Consider union membership: if workers who join unions more often (high $\overline{union}_i$) also have higher unobserved ability or motivation, then $\overline{union}_i$ captures that correlation. Once we control for it, the remaining within-person variation in union status is “clean” — and the time-invariant variables are no longer collinear with entity dummies (because there are no entity dummies).

Contrast with FE. One-way FE assumes $\alpha_i$ can be anything — completely unrestricted. CRE assumes $\alpha_i = \pi \bar{X}_i + \text{error}$ — the individual effect is a linear function of the career averages. This is a stronger assumption, but it buys back education and race. The payoff: $\hat{\beta}$ for time-varying variables should approximately match the one-way FE estimates (because the means absorb the same correlation), while $\gamma$ for time-invariant variables is now estimable.

mundlak_vars = ["union", "married", "hours", "expersq"]

for var in mundlak_vars:

wage_df[f"{var}_mean"] = wage_df.groupby("nr")[var].transform("mean")

fit_mundlak = pf.feols(

"lwage ~ expersq + union + married + hours + educ + black + hisp "

"+ expersq_mean + union_mean + married_mean + hours_mean",

data=wage_df, vcov={"CRV1": "nr"}

)

print(fit_mundlak.summary())

Estimation: OLS

Dep. var.: lwage, Fixed effects: 0

Inference: CRV1

Observations: 4360

| Coefficient | Estimate | Std. Error | t value | Pr(>|t|) | 2.5% | 97.5% |

|:--------------|-----------:|-------------:|----------:|-----------:|-------:|--------:|

| Intercept | 0.276 | 0.073 | 3.798 | 0.000 | 0.133 | 0.418 |

| expersq | 0.004 | 0.000 | 13.284 | 0.000 | 0.004 | 0.005 |

| union | 0.078 | 0.019 | 4.050 | 0.000 | 0.040 | 0.116 |

| married | 0.115 | 0.017 | 6.664 | 0.000 | 0.081 | 0.149 |

| hours | -0.000 | 0.000 | -0.007 | 0.994 | -0.000 | 0.000 |

| educ | 0.094 | 0.005 | 17.295 | 0.000 | 0.083 | 0.104 |

| black | -0.140 | 0.024 | -5.930 | 0.000 | -0.187 | -0.094 |

| hisp | 0.009 | 0.019 | 0.469 | 0.639 | -0.028 | 0.045 |

| expersq_mean | -0.003 | 0.001 | -3.498 | 0.001 | -0.005 | -0.001 |

| union_mean | 0.179 | 0.037 | 4.838 | 0.000 | 0.106 | 0.251 |

| married_mean | -0.041 | 0.042 | -0.969 | 0.333 | -0.123 | 0.042 |

| hours_mean | 0.002 | 0.001 | 3.109 | 0.002 | 0.001 | 0.003 |

| Variable | One-Way FE | CRE |

|---|---|---|

| expersq | 0.004 | 0.004 |

| union | 0.078 | 0.078 |

| married | 0.115 | 0.115 |

| hours | -0.000 | -0.000 |

| educ | dropped | 0.094 |

| black | dropped | -0.140 |

| hisp | dropped | 0.009 |

fig, ax = plt.subplots(figsize=(10, 6))

compare_vars = ["expersq", "union", "married", "hours", "educ", "black", "hisp"]

x = np.arange(len(compare_vars))

width = 0.25

pooled_vals = [fit_pooled.coef()[v] for v in compare_vars]

entity_vals = [fit_entity.coef()[v] if v in fit_entity.coef().index else 0 for v in compare_vars]

mundlak_vals = [fit_mundlak.coef()[v] if v in fit_mundlak.coef().index else 0 for v in compare_vars]

ax.bar(x - width, pooled_vals, width, label="Pooled OLS", color=STEEL_BLUE, edgecolor=DARK_NAVY)

ax.bar(x, entity_vals, width, label="One-Way FE", color=WARM_ORANGE, edgecolor=DARK_NAVY)

ax.bar(x + width, mundlak_vals, width, label="CRE", color=TEAL, edgecolor=DARK_NAVY)

ax.set_xticks(x)

ax.set_xticklabels(compare_vars, fontsize=10, rotation=15)

ax.set_ylabel("Coefficient Estimate", fontsize=13)

ax.set_title("Pooled OLS vs One-Way FE vs CRE", fontsize=14, fontweight="bold")

ax.legend(fontsize=11)

ax.axhline(y=0, color=NEAR_BLACK, linewidth=0.5, linestyle="--", alpha=0.5)

plt.savefig("pyfixest_mundlak.png", dpi=300, bbox_inches="tight",

facecolor=DARK_NAVY, edgecolor=DARK_NAVY, pad_inches=0)

plt.show()

The CRE model bridges one-way FE and pooled OLS. For time-varying variables (union, married, hours, expersq), the CRE coefficients closely match the one-way FE estimates — confirming that the individual means successfully proxy for entity dummies. For time-invariant variables, CRE recovers what one-way FE cannot: education’s coefficient is 0.094 per year of schooling (a 9.4% return), and the Black wage gap is -0.140 (14.0% lower wages). These are close to the pooled OLS estimates, but now they are estimated in a framework that controls for the correlation between unobserved heterogeneity and the covariates (via the individual means).

The CRE correction terms ($\pi$ coefficients) are informative in their own right. The union_mean coefficient of 0.179 is large and highly significant ($p < 0.001$): workers with persistently higher union participation earn substantially more on average, even after controlling for the within-person union effect (0.078). This gap — 0.179 versus 0.078 — is evidence of positive selection into unions: workers who join unions more often tend to have higher unobserved ability or to work in higher-paying industries. The hours_mean coefficient (0.002, $p = 0.002$) suggests that workers who consistently work longer hours earn more per hour on average, while married_mean is small and insignificant, indicating that selection into marriage is not strongly associated with unobserved wage determinants once other factors are controlled.

The caveat is that CRE relies on the assumption that unobserved heterogeneity correlates with covariates only through their individual means — a stronger assumption than one-way FE, which makes no such restriction. However, this assumption is testable. The CRE correction terms provide a built-in Hausman-type test: if $\pi = 0$ jointly (all correction terms are zero), then pooled OLS and one-way FE yield the same estimates, and the simpler random effects model is efficient. In our case, the large and significant union_mean and hours_mean coefficients strongly reject $\pi = 0$, confirming that unobserved heterogeneity does correlate with the covariates and that FE or CRE is needed over pooled OLS. Exercise 6 asks you to formalize this test.

11.8 What fixed effects absorb vs. what survives

The wage panel illustrates a general principle: one-way fixed effects absorb everything about a person that does not change over the observation window. Variables that do change over time — like union status, marital status, and occupation — survive the within transformation and can be estimated. The CRE/Mundlak approach (Section 11.7) partially resolves the tradeoff by recovering time-invariant coefficients. The diagram below summarizes this partition and recovery:

graph LR

subgraph "Absorbed by One-Way FE"

ED["<b>Education</b><br/>(time-invariant)"]

AB["<b>Ability</b><br/>(unobserved)"]

RC["<b>Race</b><br/>(time-invariant)"]

end

subgraph "Estimated (time-varying)"

UN["<b>Union</b>"]

MA["<b>Married</b>"]

OC["<b>Occupation</b>"]

end

subgraph "Recovery strategies"

MK["<b>CRE/Mundlak</b><br/>(individual means)"]

end

UN --> W["<b>Log Wage</b>"]

MA --> W

OC --> W

ED -.-> W

AB -.-> W

MK -.->|"recovers γ"| ED

MK -.->|"recovers γ"| RC

style ED fill:#d97757,stroke:#141413,color:#fff,stroke-dasharray: 5 5

style AB fill:#d97757,stroke:#141413,color:#fff,stroke-dasharray: 5 5

style RC fill:#d97757,stroke:#141413,color:#fff,stroke-dasharray: 5 5

style UN fill:#6a9bcc,stroke:#141413,color:#fff

style MA fill:#6a9bcc,stroke:#141413,color:#fff

style OC fill:#6a9bcc,stroke:#141413,color:#fff

style W fill:#00d4c8,stroke:#141413,color:#fff

style MK fill:#1a3a8a,stroke:#141413,color:#fff,stroke-dasharray: 5 5

The dashed arrows from the orange (absorbed) variables indicate that their effects on wages are real but unestimable under one-way FE — they are folded into each worker’s individual intercept. The solid arrows from the blue (estimated) variables show the effects we can identify: changes in union status, marital status, and occupation that occur within a worker’s career. The dark blue CRE/Mundlak node represents the recovery strategy from Section 11.7: by substituting individual means for entity dummies, we recover the coefficients $\gamma$ for education and race while producing time-varying estimates that closely match one-way FE. This partially resolves the tradeoff from Section 11.4, though at the cost of a stronger modeling assumption.

12. Event study: difference-in-differences

12.1 Staggered treatment adoption

Event studies are a popular extension of fixed effects that estimate dynamic treatment effects around the time of an intervention. In a staggered design, different groups (states, firms, individuals) receive treatment at different times — for example, states adopting a minimum wage increase in different years. The standard approach uses TWFE with relative-time indicators. However, this can produce biased estimates when treatment timing varies across groups and effects are heterogeneous. The DID2S estimator (Gardner, 2022) addresses this by separating the estimation into two stages: first estimating fixed effects from untreated observations, then recovering treatment effects from the residuals. The target estimand in this design is the Average Treatment Effect on the Treated (ATT) — the average effect for units that actually received treatment.

PyFixest provides both approaches. We use a simulated dataset with staggered treatment adoption across states:

df_het = pd.read_csv(

"https://raw.githubusercontent.com/py-econometrics/pyfixest/master/pyfixest/did/data/df_het.csv"

)

print(f"DiD dataset shape: {df_het.shape}")

print(f"Columns: {list(df_het.columns)}")

DiD dataset shape: (46500, 14)

Columns: ['unit', 'state', 'group', 'unit_fe', 'g', 'year', 'year_fe', 'treat',

'rel_year', 'rel_year_binned', 'error', 'te', 'te_dynamic', 'dep_var']

The event study dataset contains 46,500 observations across units nested in states, with a binary treatment indicator and relative time variable measuring periods before and after treatment onset. The dep_var column is the outcome we want to explain, and rel_year measures the distance in years from each unit’s treatment date (negative values are pre-treatment). This structure is typical of policy evaluation studies where different states adopt a policy at different times.

12.2 Year −1 as the universal baseline

Both estimators use ref=-1.0, setting the last pre-treatment period as the baseline. This choice is not arbitrary — it is the conventional and most informative reference point for three reasons:

-

Closest to treatment onset. Period −1 is the last observation before treatment begins. Using it as the baseline minimizes the extrapolation distance: we compare each period’s outcome to the most recent untreated state, rather than to some distant past.

-

Universal across cohorts. In staggered designs, different states adopt treatment in different calendar years. But

rel_year = -1has the same meaning for every cohort: “the last year before this group was treated.” It aligns all cohorts to a common relative-time clock, making the coefficients directly comparable. -

Transparent parallel trends test. Pre-treatment coefficients (periods −20 through −2) measure deviations from the baseline. If these coefficients are near zero, the treated and control groups were on parallel trajectories before treatment — validating the key identifying assumption. Choosing −1 as the baseline makes this test as transparent as possible: any non-zero pre-treatment coefficient is a direct signal of differential pre-trends.

How to read the event study plot. Each coefficient represents the difference in outcomes between treatment and control groups, relative to their difference at period −1. Pre-treatment coefficients near zero validate parallel trends. The coefficient at period 0 is the immediate treatment effect. Post-treatment coefficients show how the effect evolves over time. If we had chosen a different baseline (say, period −5), all coefficients would shift by a constant — the shape of the event study would be identical, but the levels would change. The convention of using −1 simply makes the plot easiest to interpret.

12.3 TWFE vs DID2S

We estimate event study coefficients using both TWFE and DID2S, with period -1 (the year before treatment) as the reference category. The i() operator in PyFixest creates indicator variables for each relative year, analogous to R’s i() function.

# TWFE event study

fit_twfe = pf.feols(

"dep_var ~ i(rel_year, ref=-1.0) | state + year",

data=df_het, vcov={"CRV1": "state"},

)

# DID2S (Gardner 2022) -- two-stage estimator

fit_did2s = pf.did2s(

df_het, yname="dep_var",

first_stage="~ 0 | state + year",

second_stage="~ i(rel_year, ref=-1.0)",

treatment="treat", cluster="state",

)

# Extract coefficients from both estimators for plotting

import re

def parse_rel_years(coef_dict, se_dict):

years, vals, ses_list = [], [], []

for k in coef_dict.index:

match = re.search(r'\[T\.(-?\d+\.?\d*)\]', str(k))

if match:

years.append(float(match.group(1)))

vals.append(coef_dict[k])

ses_list.append(se_dict[k])

return years, vals, ses_list

twfe_years, twfe_vals, twfe_ses = parse_rel_years(fit_twfe.coef(), fit_twfe.se())

did2s_years, did2s_vals, did2s_ses = parse_rel_years(fit_did2s.coef(), fit_did2s.se())

PyFixest stores event study coefficients with names like [T.-5.0], [T.0.0], etc. The helper function above extracts the relative year from each coefficient name and pairs it with the estimate and standard error, giving us arrays ready for plotting.

fig, ax = plt.subplots(figsize=(12, 6))

offset = 0.15

ax.errorbar([y - offset for y in twfe_years], twfe_vals,

yerr=[1.96*s for s in twfe_ses],

fmt='o', color=STEEL_BLUE, capsize=3, label='TWFE')

ax.errorbar([y + offset for y in did2s_years], did2s_vals,

yerr=[1.96*s for s in did2s_ses],

fmt='s', color=WARM_ORANGE, capsize=3, label='DID2S (Gardner 2022)')

ax.axhline(y=0, color=LIGHT_TEXT, linewidth=0.8, linestyle="--", alpha=0.5)

ax.axvline(x=-0.5, color=LIGHT_TEXT, linewidth=1, linestyle="--", alpha=0.6)

ax.plot(-1, 0, 'D', color=TEAL, markersize=10, zorder=5,

label="Baseline (t = −1)")

ax.set_xlabel("Relative Year", fontsize=13)

ax.set_ylabel("Coefficient Estimate", fontsize=13)

ax.set_title("Event Study: TWFE vs DID2S", fontsize=14, fontweight="bold")

ax.legend(fontsize=11)

plt.savefig("pyfixest_event_study.png", dpi=300, bbox_inches="tight",

facecolor=DARK_NAVY, edgecolor=DARK_NAVY, pad_inches=0)

plt.show()

Both estimators show near-zero pre-treatment coefficients (validating the parallel trends assumption) and a sharp jump at treatment onset. The immediate treatment effect at period 0 is approximately 1.3–1.4, growing steadily to about 2.8 by period 20. The TWFE estimates (blue circles) are slightly larger than DID2S (orange squares) in post-treatment periods — this upward bias is the well-documented problem with TWFE under staggered adoption and heterogeneous effects. The DID2S estimator corrects this by using only untreated observations to estimate the counterfactual, producing cleaner estimates of the dynamic treatment path.

13. Hypothesis testing: Wald test

PyFixest supports joint hypothesis testing via Wald tests, which assess whether multiple coefficients are simultaneously equal to zero. This is useful when you want to test whether a group of related variables jointly matters, not just one at a time.

fit_wald = pf.feols("Y ~ X1 + X2 | f1", data=data, vcov="HC1")

R = np.eye(2) # Test both X1=0 and X2=0 jointly

wald_result = fit_wald.wald_test(R=R)

print(f"Wald test (joint null: X1=0, X2=0):")

print(wald_result)

Wald test (joint null: X1=0, X2=0):

statistic 1.554006e+02

pvalue 1.110223e-16

The Wald test statistic is 155.4 with a p-value effectively zero (< 10^{-16}), overwhelmingly rejecting the null hypothesis that both X1 and X2 have zero effect on Y. This joint test is more informative than individual t-tests because it accounts for the correlation between the two coefficient estimates. In practice, Wald tests are essential for testing hypotheses about groups of variables, such as whether all interaction terms or all year dummies are jointly significant.

14. Wild cluster bootstrap

When the number of clusters is small (roughly below 50), cluster-robust standard errors can be unreliable. The wild cluster bootstrap provides more accurate inference in this setting by simulating the distribution of the test statistic under the null hypothesis. PyFixest integrates with the wildboottest package to make this straightforward:

fit_boot = pf.feols("Y ~ X1 | group_id", data=data, vcov={"CRV1": "group_id"})

boot_result = fit_boot.wildboottest(param="X1", reps=999, seed=42)

print(boot_result)

param X1

t value -8.616818459577098

Pr(>|t|) 0.0

bootstrap_type 11

inference CRV(group_id)

impose_null True

The wild bootstrap t-statistic of -8.62 and p-value of 0.0 confirm that the effect of X1 remains highly significant even under the more conservative bootstrap inference. The impose_null=True setting means the bootstrap simulates data under the null hypothesis of no effect, which generally provides better size control in finite samples. With only ~20 groups in this dataset, the bootstrap p-value is more trustworthy than the asymptotic cluster-robust p-value.

15. Discussion

This tutorial posed a simple question: how do unobserved group-level characteristics bias regression estimates, and how can we account for them? The answer, demonstrated across multiple settings, is that fixed effects regression removes this bias by focusing on within-group variation only.

The synthetic data showed that OLS estimates shift from -1.000 to -1.019 when absorbing group fixed effects — a modest change in this controlled setting, but one that demonstrates the mechanism. The real-world wage panel told a more dramatic story: the union wage premium dropped from 18.3% (pooled OLS) to 7.3% (two-way FE), revealing that more than half of the apparent union premium reflects worker selection rather than a genuine union effect. This has direct implications for labor economists and policymakers: overestimating the union premium leads to overestimating the economic impact of declining unionization.

Framing the wage panel through the Mincer equation (Section 11.3) provided a unifying thread for the entire analysis. The classic Mincer specification — log wages as a function of education, experience, and experience squared — is the starting point for virtually all empirical wage research. By extending it with additional controls and then progressively adding fixed effects, we traced a clear arc from pooled cross-sectional estimation to panel methods that account for unobserved heterogeneity. The within-versus-between decomposition (Section 11.2) made this arc concrete: education has zero within-worker variation, so one-way FE cannot estimate its effect, while variables like union status and marital status have substantial within-worker variation and can be identified.

The wage panel also highlighted a fundamental tradeoff in fixed effects estimation: the very mechanism that removes ability bias — absorbing all time-invariant individual characteristics — also prevents estimation of time-invariant variables like education. This is not a limitation to be worked around but a defining feature of the method. The CRE/Mundlak approach (Section 11.7) offers a principled resolution: by including individual means of time-varying variables as additional regressors, it proxies for the unobserved heterogeneity that one-way FE would absorb, recovering education’s coefficient (0.094 per year of schooling) while producing time-varying estimates that closely match one-way FE. The key assumption — that unobserved heterogeneity correlates with covariates only through their individual means — is stronger than FE’s assumption of no time-varying confounding, but it is the price of recovering time-invariant effects.

The three-way FE extension (adding occupation fixed effects) showed that occupation sorting explains negligible additional wage variation beyond individual and time effects, confirming that the dominant source of wage heterogeneity is persistent individual characteristics. The group-specific time trends analysis (Section 11.6) showed that allowing Black and non-Black workers to have different year effects produces estimates nearly identical to standard TWFE, supporting the common trends assumption in this particular panel. This is a useful diagnostic in practice: if group-specific trends substantially change the coefficients, the researcher should worry about whether the standard TWFE results are confounded by differential macro trends.

PyFixest makes the entire workflow — from simple OLS through two-way FE, IV, CRE/Mundlak, and event studies — accessible with a concise formula syntax. The ability to estimate multiple specifications in one call (csw0) and compare inference methods (iid, HC1, CRV1, CRV3, wild bootstrap) means researchers can quickly build a comprehensive picture of how sensitive their results are to modeling choices.

16. Summary and next steps

Key takeaways:

-