The 95% CI is roughly \([0.85, 1.45]\) — it contains 1. We cannot reject full pass-through.

If oil firms had absorbed the tax, the price signal never reaches drivers. They didn’t — so the behavioural channel is real.

Consumers respond ~3× more strongly to a tax krona than to a price krona

Price semi-elasticity

\(\hat\beta_{\text{price}} = -0.060\)

+1 SEK/litre real price \(\Rightarrow\) −6% gasoline use

stable across OLS1–OLS4

IV (oil price): −0.064

Tax semi-elasticity

\(\hat\beta_{\text{tax}} = -0.186\)

+1 SEK/litre real tax \(\Rightarrow\) −18.6% gasoline use

stable across OLS1–OLS4

IV: pinned at −0.186

Salience + permanence: a tax is announced, debated, and persistent; a price drift is just a number on a billboard.

IV barely moves OLS — and that itself is informative

Price and tax semi-elasticities under OLS4 and three IV specifications. The tax coefficient is locked at −0.186.

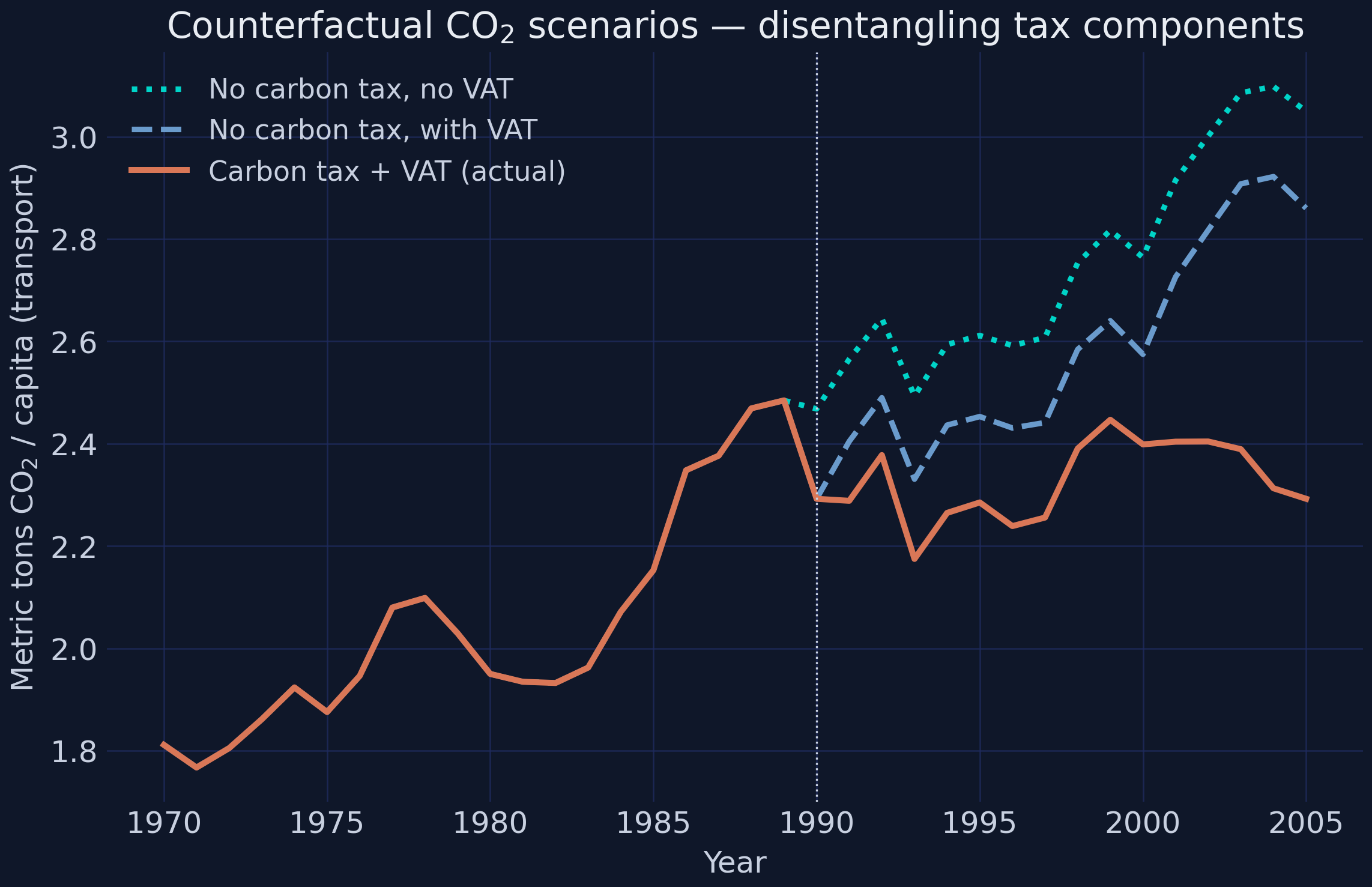

The carbon tax alone explains ~75% of the 2005 reform wedge

Three counterfactual CO2 paths. The orange-to-blue gap is the carbon-tax-only contribution; orange-to-teal adds the VAT.

The Resolution

Act III

One sentence: the tax cut CO2 ~11% a year, at no measurable cost to growth

Quantity

Value

Reading

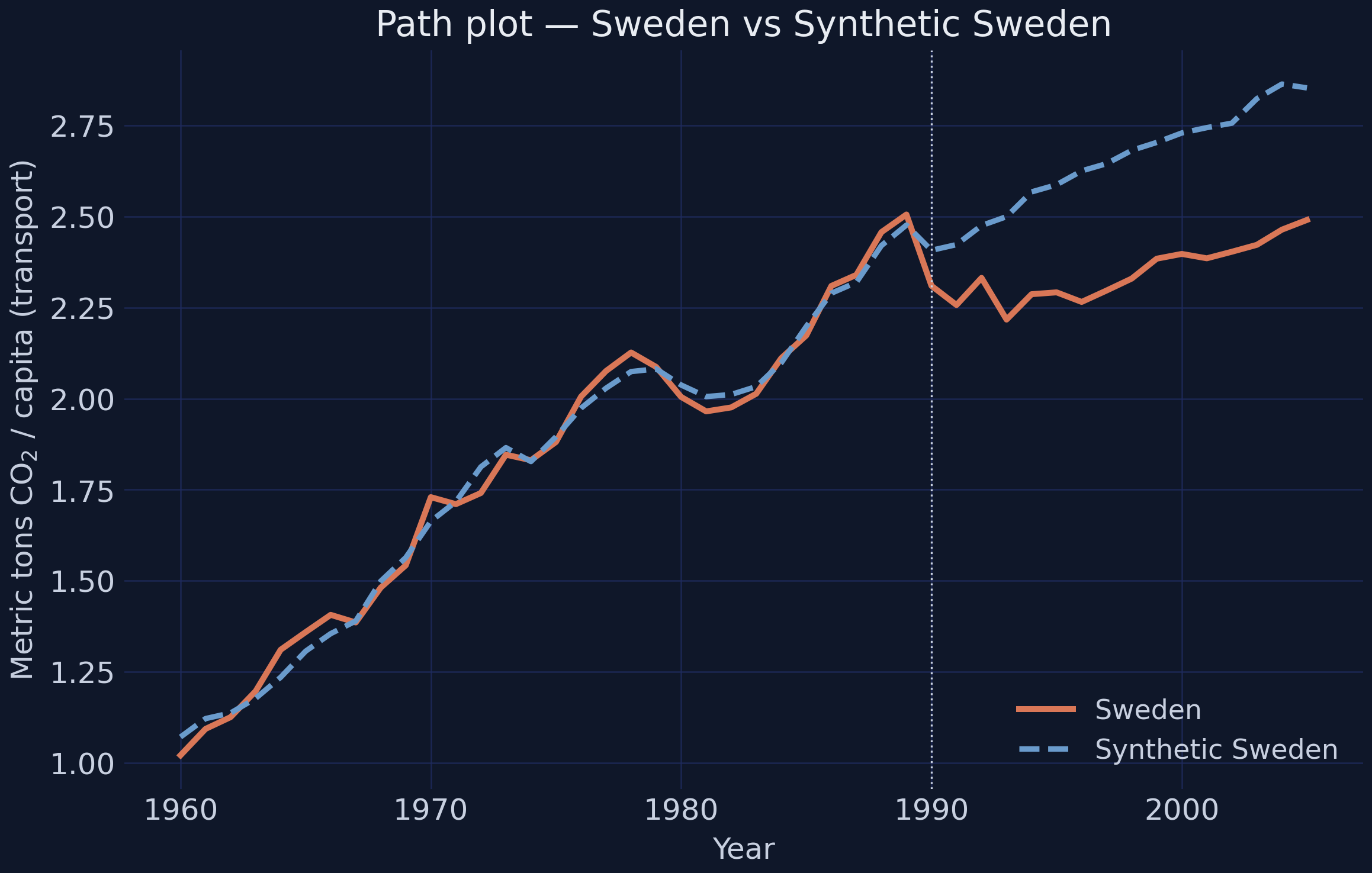

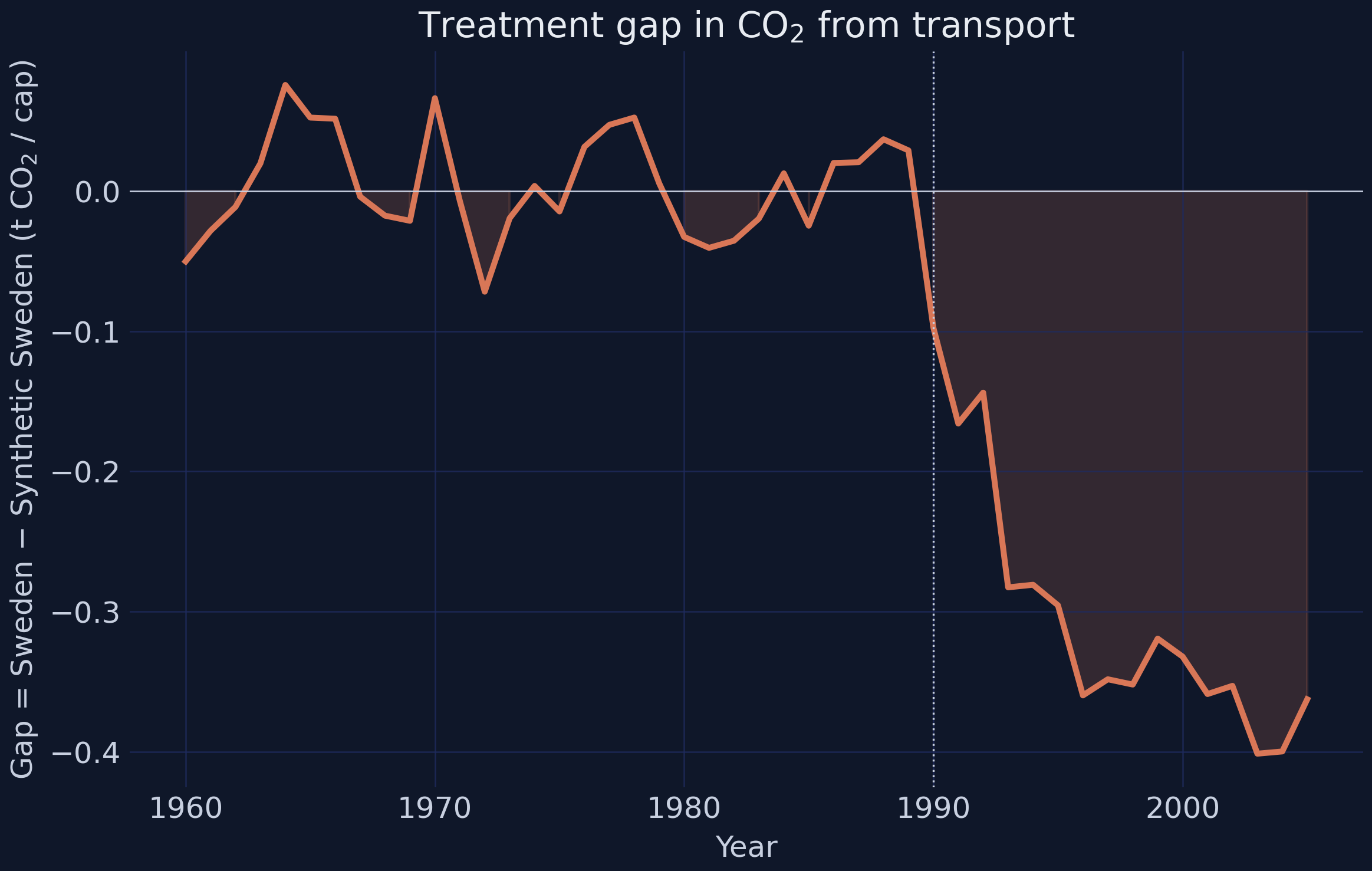

Synthetic gap, avg

−11.3%

CO2 cut ~a tenth, every year, 16 years

Permutation \(p\)

0.067

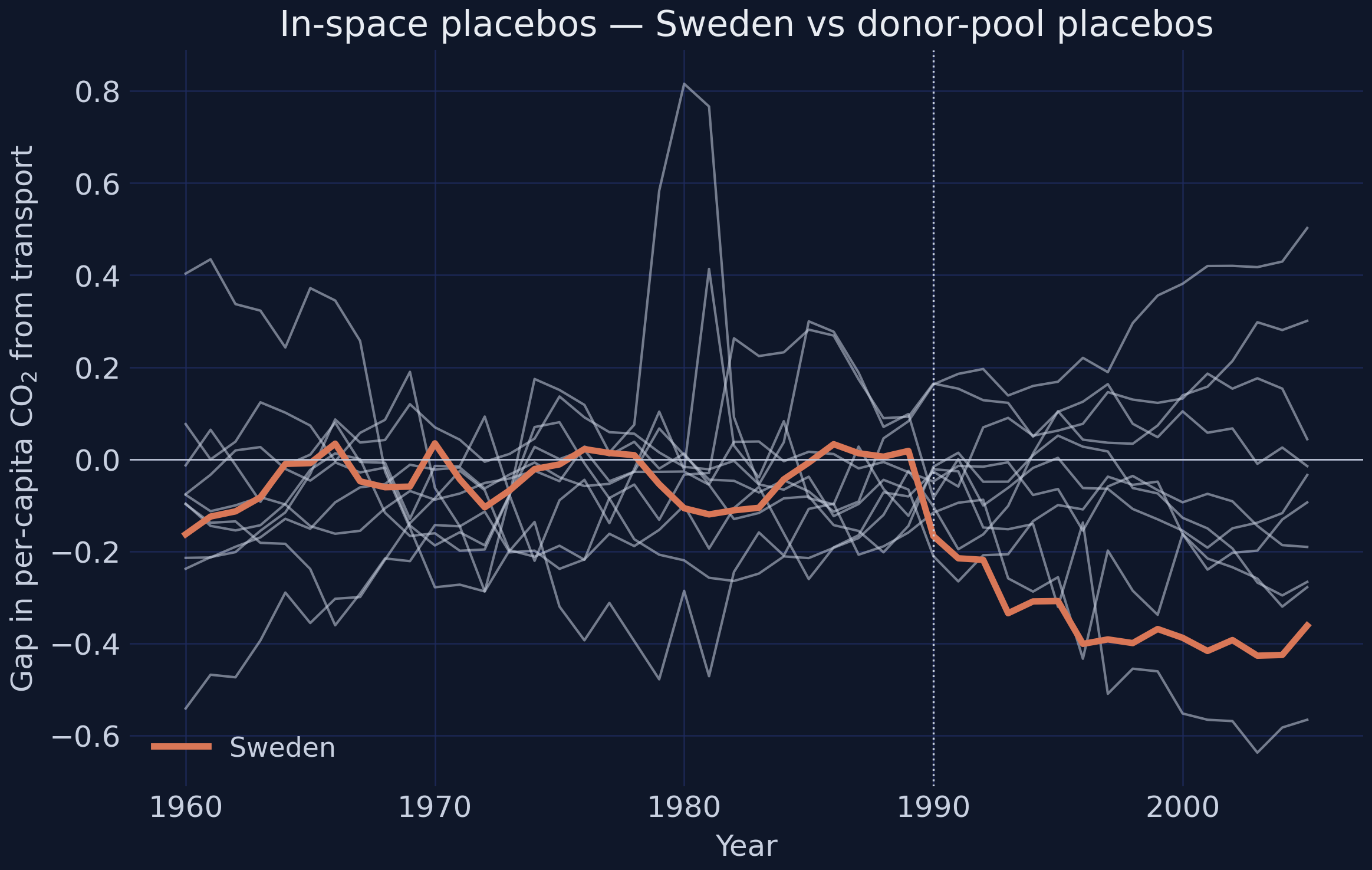

1 of 15 placebos is this extreme

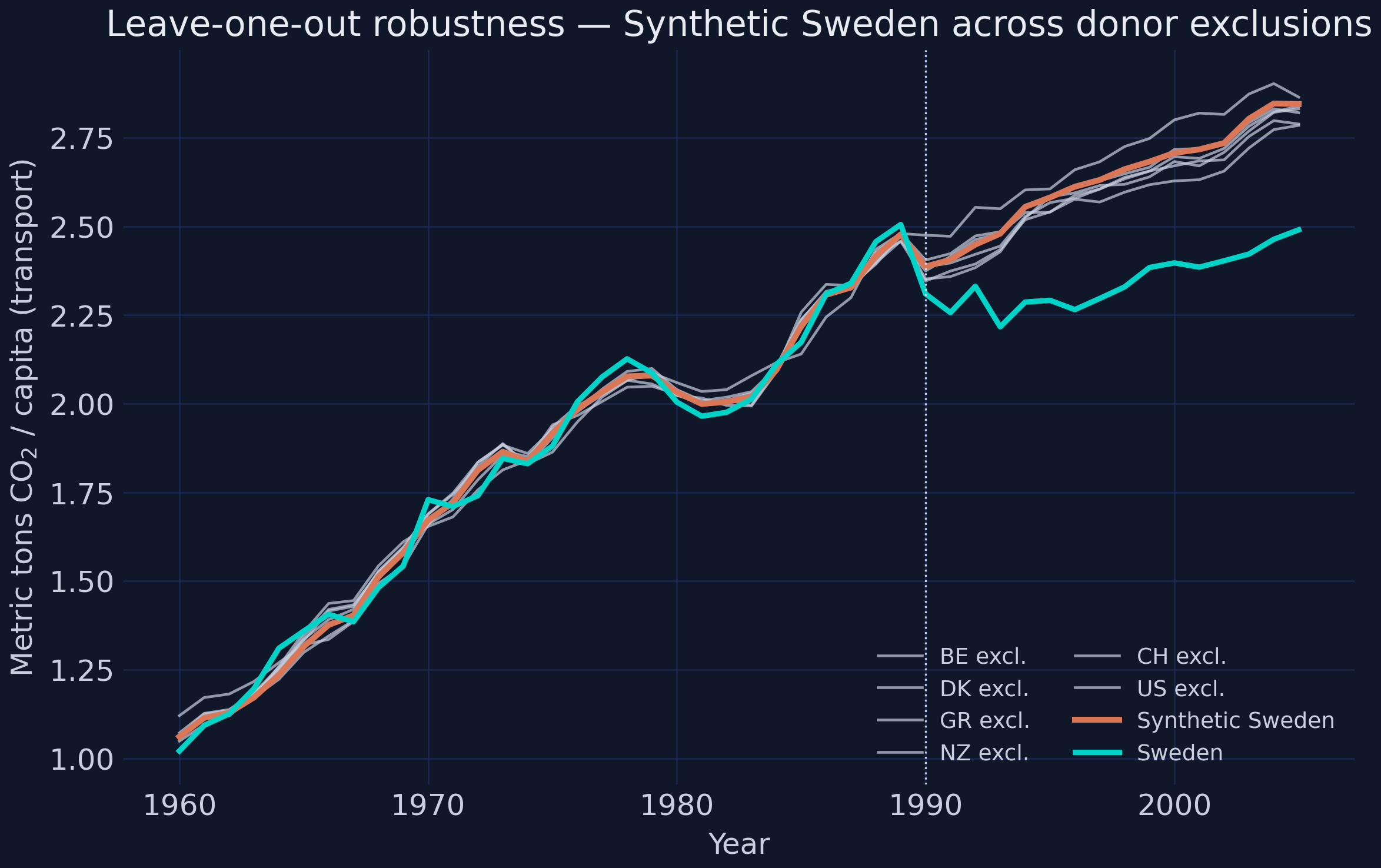

Leave-one-out

8.8%–13%

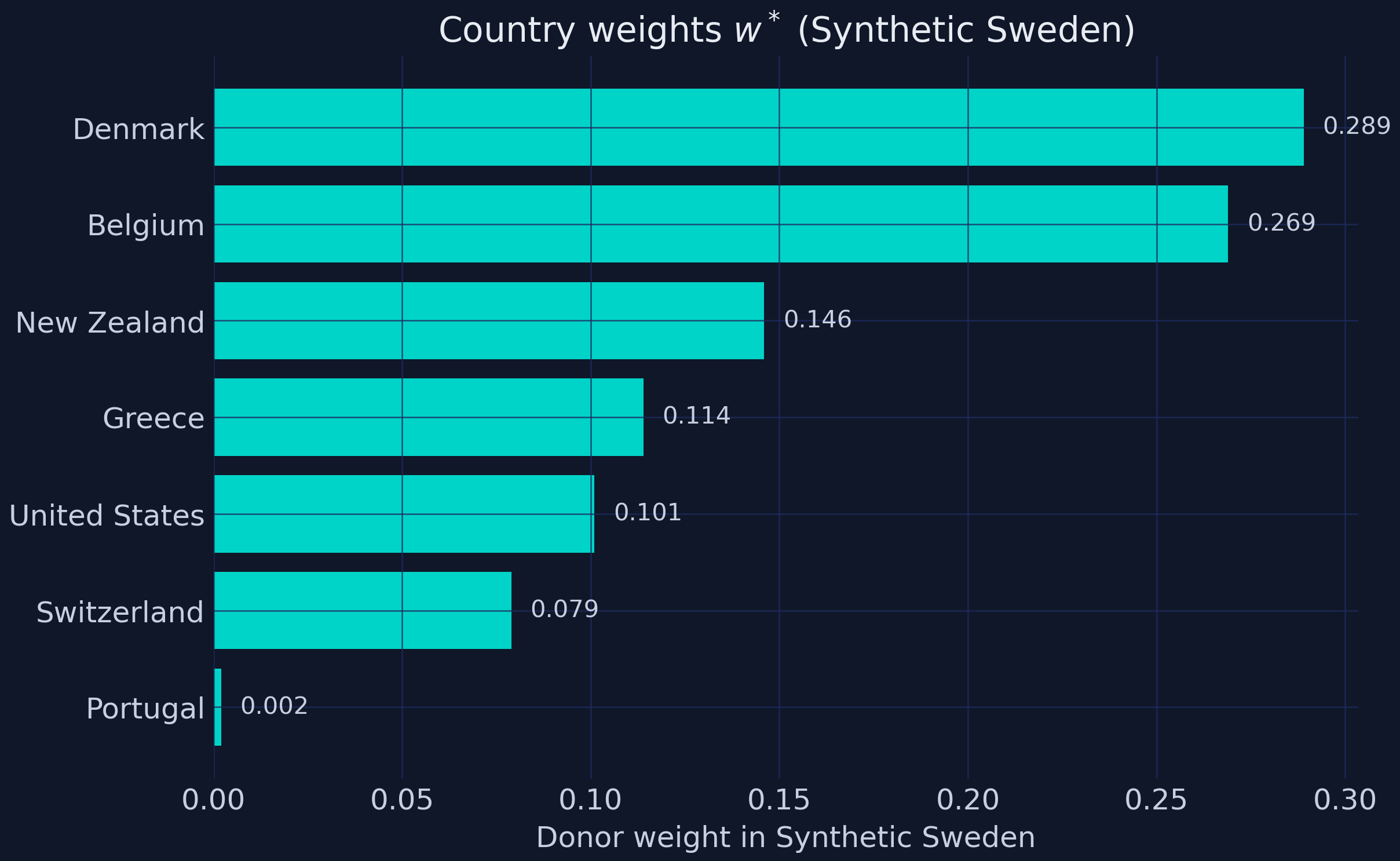

survives dropping any single donor

Tax vs price

3×

tax bites 3× harder per SEK

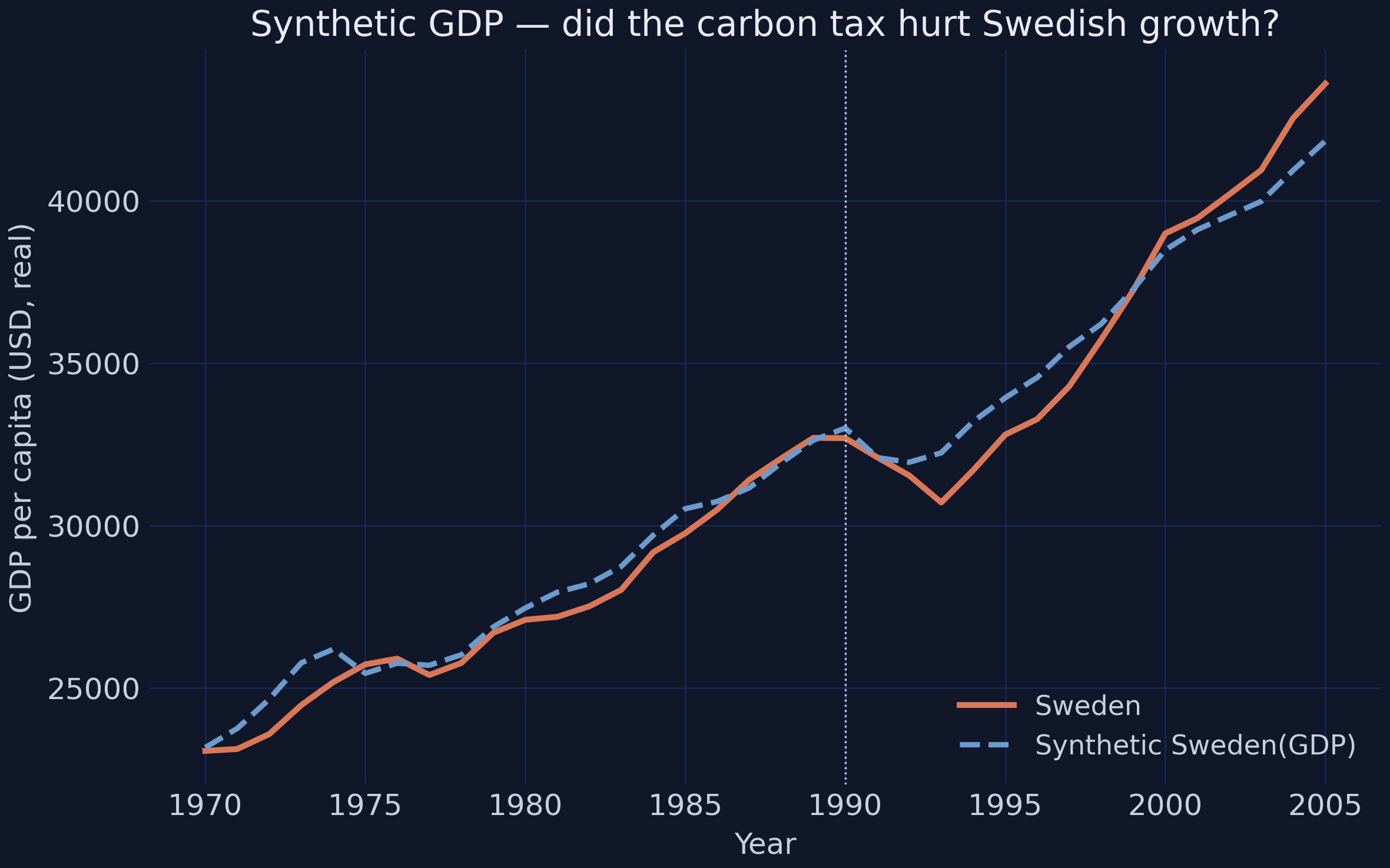

Synthetic GDP gap

< $233/cap

no detectable growth penalty

The strongest objection — and the answer

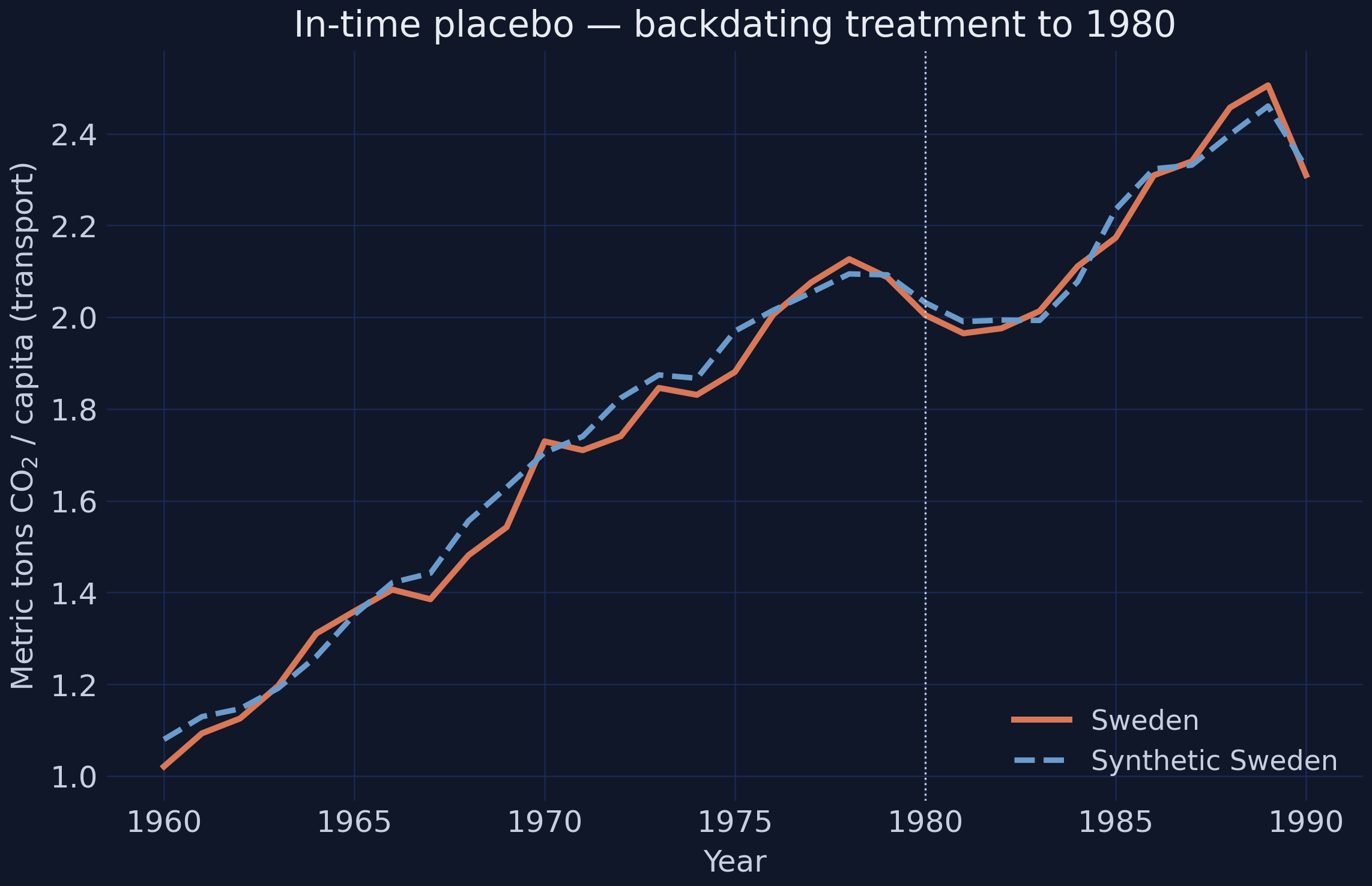

Objection. Sweden is one country, one observation. With 15 donors the smallest possible \(p\) is \(1/15 \approx 0.067\) — you hit the floor, not a clean rejection. And the analysis stops in 2005.

Response. All true, and stated plainly. But three independent falsifications point the same way, the GDP placebo rules out the recession story, and the demand-side mechanism is identified separately. The design under-claims by construction; the convergence of evidence is the argument, not any single \(p\).

A salient, persistent, fully passed-through carbon tax cut emissions — without cutting growth.