Three Methods for Robust Variable Selection: BMA, LASSO, and WALS

1. Overview

Imagine you are an economist advising a government on climate policy. Your team has collected cross-country data on a dozen potential drivers of CO2 emissions: GDP per capita, fossil fuel dependence, urbanization, industrial output, democratic governance, trade networks, agricultural activity, trade openness, foreign direct investment, corruption, tourism, and domestic credit. The government has a limited budget and wants to know: which of these factors truly drive CO2 emissions, and which are red herrings?

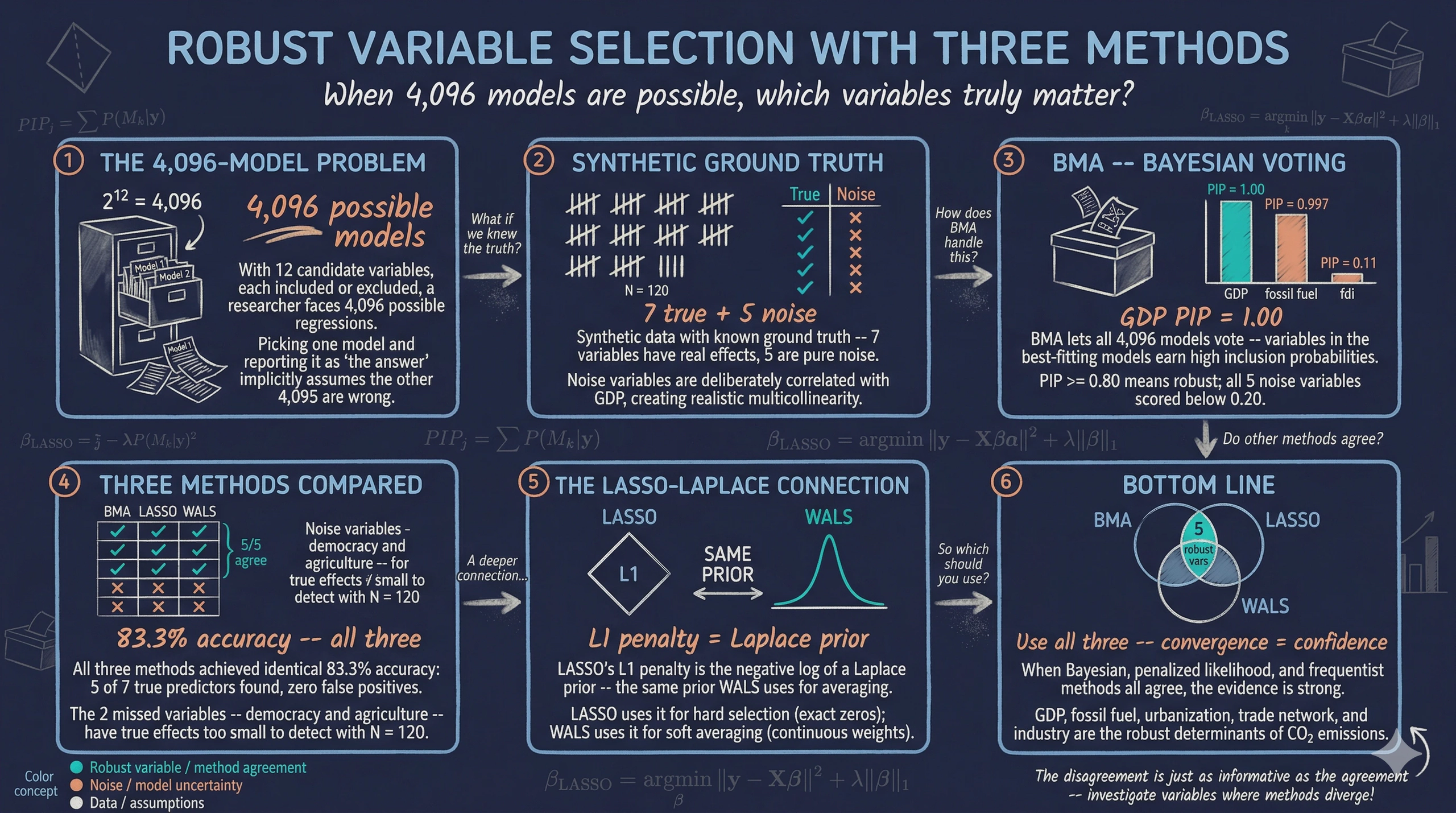

This is the variable selection problem, and it is harder than it sounds. With 12 candidate variables, each either included or excluded from a regression, there are $2^{12} = 4,096$ possible models you could estimate. Run one model and report it as “the answer,” and you have implicitly assumed the other 4,095 models are wrong. That is a very strong assumption — and almost certainly unjustified.

In practice, researchers handle this by specification searching: they try many models, drop insignificant variables, and report whichever specification “works best.” This process inflates false discoveries. A noise variable that happens to look significant in one specification gets reported, while the many failed specifications are hidden in the researcher’s desk drawer. This is sometimes called the file drawer problem or pretesting bias.

This tutorial introduces three principled approaches to the variable selection problem:

graph TD

Q["<b>Variable Selection</b><br/>Which of 12 variables<br/>truly matter?"] --> BMA

Q --> LASSO

Q --> WALS

BMA["<b>BMA</b><br/>Bayesian Model Averaging<br/>PIPs from 4,096 models"] --> R["<b>Convergence</b><br/>Variables identified<br/>by all 3 methods"]

LASSO["<b>LASSO</b><br/>L1 penalized regression<br/>Automatic selection"] --> R

WALS["<b>WALS</b><br/>Frequentist averaging<br/>t-statistics"] --> R

style Q fill:#141413,stroke:#141413,color:#fff

style BMA fill:#6a9bcc,stroke:#141413,color:#fff

style LASSO fill:#d97757,stroke:#141413,color:#fff

style WALS fill:#00d4c8,stroke:#141413,color:#fff

style R fill:#1a3a8a,stroke:#141413,color:#fff

-

Bayesian Model Averaging (BMA): Average across all 4,096 models, weighting each by how well it fits the data. Variables that appear important across many models earn a high “inclusion probability.”

-

LASSO (Least Absolute Shrinkage and Selection Operator): Add a penalty to the regression that forces the coefficients of irrelevant variables to be exactly zero, performing automatic selection.

-

Weighted Average Least Squares (WALS): A fast frequentist model-averaging method that transforms the problem so each variable can be evaluated independently.

We use synthetic data throughout this tutorial. This means we know the true data-generating process — which variables truly matter and which do not. This “answer key” lets us verify whether each method correctly recovers the truth. By the end, you will understand not just how to run each method, but why it works and when to prefer one over the others.

Learning objectives:

- Understand the variable selection problem and why running a single model is insufficient when model uncertainty is large

- Implement Bayesian Model Averaging in R and interpret Posterior Inclusion Probabilities (PIPs)

- Apply LASSO with cross-validation to perform automatic variable selection and use Post-LASSO for unbiased estimation

- Run WALS as a fast frequentist model-averaging alternative and interpret its t-statistics

- Compare results across all three methods to identify truly robust determinants via methodological triangulation

Content outline. Section 2 sets up the R environment. Section 3 introduces the synthetic dataset and its built-in “answer key” — 7 true predictors and 5 noise variables with realistic multicollinearity. Section 4 runs naive OLS to illustrate the spurious significance problem. Sections 5–8 cover BMA: Bayes' rule foundations, the PIP framework, a toy example, and full implementation. Sections 9–12 cover LASSO: the bias-variance tradeoff, L1/L2 geometry, cross-validated implementation, and Post-LASSO. Sections 13–16 cover WALS: frequentist model averaging, the semi-orthogonal transformation, the Laplace prior, and implementation. Section 17 brings all three methods together for a grand comparison. Section 18 summarizes key takeaways and provides further reading.

2. Setup

Before running the analysis, install the required packages if needed. The following code checks for missing packages and installs them automatically.

# List all packages needed for this tutorial

required_packages <- c(

"tidyverse", # data manipulation and ggplot2 visualization

"BMS", # Bayesian Model Averaging via the bms() function

"glmnet", # LASSO and Ridge regression via coordinate descent

"WALS", # Weighted Average Least Squares estimation

"scales", # nice axis formatting in plots

"patchwork", # combine multiple ggplot panels

"ggrepel", # non-overlapping text labels on plots

"corrplot", # correlation matrix heatmaps

"broom" # tidy model summaries

)

# Install any packages not yet available

missing <- required_packages[!sapply(required_packages, requireNamespace, quietly = TRUE)]

if (length(missing) > 0) {

install.packages(missing, repos = "https://cloud.r-project.org")

}

# Load libraries

library(tidyverse)

library(BMS)

library(glmnet)

library(WALS)

library(scales)

library(patchwork)

library(ggrepel)

library(corrplot)

library(broom)

3. The Synthetic Dataset

3.1 The data-generating process (our “answer key”)

We use a cross-sectional dataset of 120 fictional countries. The key design choices:

- 7 variables have true nonzero effects on CO2 emissions

- 5 variables are pure noise (their true coefficients are exactly zero)

- The noise variables are correlated with GDP and other true predictors, creating realistic multicollinearity. This makes variable selection genuinely challenging — naive OLS will find spurious “significant” results for noise variables.

Think of this as setting up a controlled experiment. We know the answer before we begin, so we can grade each method’s performance.

The data-generating process below shows exactly how the synthetic dataset was built. The CSV file synthetic-co2-cross-section.csv was generated with set.seed(2017) and can be loaded directly from GitHub for full reproducibility.

# --- DATA-GENERATING PROCESS (reference) ---

set.seed(2017)

n <- 120 # number of "countries"

# GDP drives many other variables (realistic: richer countries

# have higher urbanization, more industry, etc.)

log_gdp <- rnorm(n, mean = 8.5, sd = 1.5)

# --- TRUE PREDICTORS (correlated with GDP) ---

fossil_fuel <- 30 + 3 * log_gdp + rnorm(n, 0, 10) # higher in richer countries

urban_pop <- 20 + 5 * log_gdp + rnorm(n, 0, 12) # increases with income

industry <- 15 + 1.5 * log_gdp + rnorm(n, 0, 6) # industry share

democracy <- 5 + 2 * log_gdp + rnorm(n, 0, 8) # democracy index

trade_network <- 0.2 + 0.05 * log_gdp + rnorm(n, 0, 0.15) # trade centrality

agriculture <- 40 - 3 * log_gdp + rnorm(n, 0, 8) # negatively correlated with GDP

# --- NOISE VARIABLES (correlated with GDP but NO true effect) ---

log_trade <- 3.5 + 0.1 * log_gdp + rnorm(n, 0, 0.5)

fdi <- 2 + rnorm(n, 0, 4)

corruption <- 0.8 - 0.05 * log_gdp + rnorm(n, 0, 0.15)

log_tourism <- 12 + 0.3 * log_gdp + rnorm(n, 0, 1.2)

log_credit <- 2.5 + 0.15 * log_gdp + rnorm(n, 0, 0.6)

# --- TRUE DATA-GENERATING PROCESS ---

log_co2 <- 2.0 + # intercept

1.200 * log_gdp + # GDP: strong positive (elasticity)

0.008 * industry + # industry: positive

0.012 * fossil_fuel + # fossil fuel: positive

0.010 * urban_pop + # urbanization: positive

0.004 * democracy + # democracy: small positive

0.500 * trade_network + # trade network: moderate positive

0.005 * agriculture + # agriculture: weak positive

# NOISE VARIABLES HAVE ZERO TRUE EFFECT

rnorm(n, 0, 0.3) # random noise (sigma = 0.3)

The true coefficients serve as our “answer key”:

| Variable | True $\beta$ | Role | Interpretation |

|---|---|---|---|

| log_gdp | 1.200 | True predictor | 1% more GDP $\to$ 1.2% more CO2 |

| trade_network | 0.500 | True predictor | Moderate positive effect |

| fossil_fuel | 0.012 | True predictor | 1 pp more fossil fuel $\to$ 1.2% more CO2 |

| urban_pop | 0.010 | True predictor | 1 pp more urbanization $\to$ 1.0% more CO2 |

| industry | 0.008 | True predictor | Positive composition effect |

| agriculture | 0.005 | True predictor | Weak positive effect |

| democracy | 0.004 | True predictor | Small positive effect |

| log_trade | 0 | Noise | No true effect |

| fdi | 0 | Noise | No true effect |

| corruption | 0 | Noise | No true effect |

| log_tourism | 0 | Noise | No true effect |

| log_credit | 0 | Noise | No true effect |

Now let us load the pre-generated dataset:

# Load the synthetic dataset directly from GitHub

DATA_URL <- "https://raw.githubusercontent.com/cmg777/starter-academic-v501/master/content/post/r_bma_lasso_wals/synthetic-co2-cross-section.csv"

synth_data <- read.csv(DATA_URL)

cat("Dataset:", nrow(synth_data), "countries,", ncol(synth_data), "variables\n")

head(synth_data)

Dataset: 120 countries, 14 variables

country log_co2 log_gdp industry fossil_fuel urban_pop democracy trade_network

1 Country_001 13.27 9.47 29.25 66.94 67.97 25.67 0.77

2 Country_002 12.18 8.44 24.97 51.43 66.14 20.51 0.85

3 Country_003 13.50 10.16 28.19 50.62 73.91 29.08 0.73

...

3.2 Descriptive statistics

The following summary statistics give us a first look at the data structure. Note the wide range of scales: GDP is in log units (mean around 8.5), while percentage variables like fossil fuel share and urbanization range from single digits to near 100.

# Descriptive statistics for all 13 numeric variables

synth_data |>

select(-country) |>

pivot_longer(everything(), names_to = "variable", values_to = "value") |>

summarise(

n = n(),

mean = round(mean(value), 2),

sd = round(sd(value), 2),

min = round(min(value), 2),

max = round(max(value), 2),

.by = variable

)

variable n mean sd min max

log_co2 120 14.22 2.11 8.76 20.36

log_gdp 120 8.53 1.57 4.61 13.21

industry 120 27.87 6.21 8.32 44.98

fossil_fuel 120 55.49 9.62 24.72 81.22

urban_pop 120 62.52 13.25 29.81 97.62

democracy 120 22.94 8.32 3.10 45.00

trade_network 120 0.64 0.17 0.18 1.04

agriculture 120 13.87 8.11 1.00 37.11

log_trade 120 4.43 0.46 3.45 5.84

fdi 120 2.23 4.19 -5.00 13.62

corruption 120 0.37 0.16 0.05 0.71

log_tourism 120 14.61 1.32 11.54 19.63

log_credit 120 3.83 0.65 2.30 5.50

The dataset has 120 observations and 14 variables (1 dependent, 12 candidate regressors, 1 country identifier). The dependent variable log_co2 has a mean of 14.22 with a standard deviation of 2.11 log points, reflecting substantial cross-country variation in emissions. The candidate regressors span very different scales — trade_network ranges from 0.18 to 1.04, while urban_pop ranges from 29.8 to 97.6 — which is why BMA, LASSO, and WALS each handle scaling internally.

3.3 Correlation structure

A key feature of our synthetic data is that the noise variables are correlated with the true predictors — especially with GDP. This correlation is what makes variable selection difficult: in a standard OLS regression, the noise variables will “borrow” explanatory power from the true predictors.

# Compute correlation matrix for all 12 candidate regressors

cor_matrix <- synth_data |>

select(-country, -log_co2) |>

cor()

# Draw the heatmap

corrplot(cor_matrix, method = "color", type = "lower",

addCoef.col = "black", number.cex = 0.7,

col = colorRampPalette(c("#d97757", "white", "#6a9bcc"))(200),

diag = FALSE)

The correlation heatmap reveals the realistic structure we built into the data. GDP is positively correlated with fossil fuel use, urbanization, industry, and the trade network — but also with the noise variables like trade openness, tourism, and credit. This multicollinearity is precisely what makes a naive “throw everything into OLS” approach unreliable. For example, log_tourism has a correlation of approximately 0.3 with log_gdp, which means it can pick up GDP’s signal even though its true effect is zero.

Note. We created a synthetic dataset where we know which 7 variables truly affect CO2 emissions and which 5 are noise. The noise variables are deliberately correlated with the true predictors, mimicking the multicollinearity found in real cross-country data.

4. The General Model

Our goal is to estimate the following linear model:

$$ \log(\text{CO}_{2,i}) = \beta_0 + \sum_{j=1}^{12} \beta_j x_{j,i} + \varepsilon_i $$

where:

- $\log(\text{CO}_{2,i})$ is the log of CO2 emissions for country $i$

- $\beta_0$ is the intercept (the predicted log CO2 when all regressors are zero)

- $\beta_j$ is the coefficient on the $j$-th regressor: the change in log CO2 associated with a one-unit increase in $x_j$, holding all other variables constant

- $\varepsilon_i$ is the error term: everything that affects CO2 emissions but is not captured by the 12 regressors

Because the dependent variable is in logs, the interpretation of each coefficient depends on whether the regressor is also in logs:

| Regressor type | Interpretation of $\beta_j$ | Example |

|---|---|---|

| Log-log (e.g., log GDP) | Elasticity: a 1% increase in GDP is associated with a $\beta_j$% change in CO2 | $\beta = 1.2$ means 1% more GDP $\to$ 1.2% more CO2 |

| Level-log (e.g., fossil fuel %) | Semi-elasticity: a 1-unit increase in the regressor is associated with a $100 \times \beta_j$% change in CO2 | $\beta = 0.012$ means 1 pp more fossil fuel $\to$ 1.2% more CO2 |

We want to determine which $\beta_j$ are truly nonzero. We know the answer (we designed the data), but let us first see what happens if we just run OLS with all 12 variables.

# Run OLS with all 12 candidate regressors

ols_full <- lm(log_co2 ~ log_gdp + industry + fossil_fuel + urban_pop +

democracy + trade_network + agriculture +

log_trade + fdi + corruption + log_tourism + log_credit,

data = synth_data)

# Display summary

summary(ols_full)

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 2.283773 0.494736 4.616 1.06e-05 ***

log_gdp 1.163669 0.032747 35.537 < 2e-16 ***

industry 0.017577 0.005004 3.513 0.000661 ***

fossil_fuel 0.011988 0.003240 3.698 0.000349 ***

urban_pop 0.008221 0.002689 3.057 0.002794 **

democracy 0.010497 0.003975 2.640 0.009549 **

trade_network 0.912828 0.203681 4.482 1.94e-05 ***

agriculture -0.000629 0.004242 -0.148 0.882568

log_trade -0.055738 0.064829 -0.860 0.391509

fdi 0.000789 0.007045 0.112 0.910964

corruption 0.010767 0.201954 0.053 0.957573

log_tourism -0.028025 0.024415 -1.148 0.253610

log_credit 0.045689 0.049690 0.919 0.360252

---

Multiple R-squared: 0.9801, Adjusted R-squared: 0.9779

Look carefully at the noise variables. For example, log_trade has a t-statistic of $-0.86$ (p = 0.392) and corruption has a t-statistic of $0.05$ (p = 0.958). None reach conventional significance in this sample. However, their estimated coefficients can be non-negligible in magnitude — and in a different random sample, some noise variables could easily cross the 5% threshold. This is the risk of spurious significance, caused by the correlation between noise variables and the true predictors. It is precisely this problem that motivates the three methods we study next.

Warning. With 12 correlated regressors and only 120 observations, OLS can produce misleading significance levels. A variable with a true coefficient of zero may appear significant simply because it is correlated with a genuinely important predictor. This is why we need principled variable selection methods.

5. Bayes' Rule — The Foundation

Before we can understand Bayesian Model Averaging, we need to understand Bayes' rule — the mathematical machinery that powers the entire framework.

5.1 A coin-flip example

Suppose a friend gives you a coin. You want to know: is this coin fair (probability of heads = 0.5), or is it biased (probability of heads = 0.7)?

Before flipping, you have no strong opinion. You assign equal prior probabilities:

- $P(\text{fair}) = 0.5$ (50% chance the coin is fair)

- $P(\text{biased}) = 0.5$ (50% chance the coin is biased)

Now you flip the coin 10 times and observe 7 heads. How should you update your beliefs?

The likelihood of seeing 7 heads in 10 flips is:

- If the coin is fair ($p = 0.5$): $P(\text{7 heads} | \text{fair}) = \binom{10}{7} (0.5)^{10} = 0.1172$

- If the coin is biased ($p = 0.7$): $P(\text{7 heads} | \text{biased}) = \binom{10}{7} (0.7)^7 (0.3)^3 = 0.2668$

The biased coin makes the data more likely. Bayes' rule combines the prior and the likelihood:

$$ P(H|D) = \frac{P(D|H) \cdot P(H)}{P(D)} $$

where:

- $P(H|D)$ = posterior probability (what we believe after seeing the data)

- $P(D|H)$ = likelihood (how probable the data is under hypothesis $H$)

- $P(H)$ = prior probability (what we believed before seeing the data)

- $P(D)$ = marginal likelihood (a normalizing constant that ensures probabilities sum to 1)

For our coin:

$$ P(\text{fair}|\text{7H}) = \frac{0.1172 \times 0.5}{0.1172 \times 0.5 + 0.2668 \times 0.5} = \frac{0.0586}{0.1920} = 0.305 $$

$$ P(\text{biased}|\text{7H}) = \frac{0.2668 \times 0.5}{0.1920} = 0.695 $$

After seeing 7 heads, we update from 50–50 to roughly 30–70 in favor of the biased coin. The data shifted our beliefs, but did not erase the prior entirely.

5.2 The bridge to model averaging

Now replace “fair coin” and “biased coin” with regression models:

- Hypothesis = “Which variables belong in the model?”

- Prior = “Before seeing data, any combination of variables is equally plausible”

- Likelihood = “How well does each model fit the data?”

- Posterior = “After seeing data, which models are most credible?”

This is exactly what BMA does. Instead of two coin hypotheses, we have 4,096 model hypotheses — but the logic of Bayes' rule is identical.

Note. Bayes' rule updates prior beliefs using data. The posterior probability of any hypothesis is proportional to its prior probability times its likelihood. BMA applies this same logic to regression models instead of coin flips.

6. The BMA Framework

6.1 Posterior model probability

With 12 candidate variables, there are $K = 12$ regressors and $2^K = 4,096$ possible models. Denote the $k$-th model as $M_k$. BMA assigns each model a posterior probability:

$$ P(M_k | y) = \frac{P(y | M_k) \cdot P(M_k)}{\sum_{l=1}^{2^K} P(y | M_l) \cdot P(M_l)} $$

This is just Bayes' rule applied to models. Let us unpack each piece:

-

$P(y | M_k)$ is the marginal likelihood of model $M_k$. It measures how well the model fits the data, automatically penalizing complexity. A model with many parameters can fit the data closely, but the marginal likelihood integrates over all possible parameter values, spreading the probability thin. This acts as a built-in Occam’s razor: simpler models that fit the data well receive higher marginal likelihoods than complex models that fit only slightly better.

-

$P(M_k)$ is the prior model probability. With no prior information, we use a uniform prior: every model is equally likely, so $P(M_k) = 1/4,096$ for all $k$. This means the posterior is driven entirely by the data.

-

The denominator is a normalizing constant that ensures all posterior model probabilities sum to 1.

6.2 Posterior Inclusion Probability (PIP)

We do not really care about individual models — we care about individual variables. The Posterior Inclusion Probability of variable $j$ is the sum of the posterior probabilities of all models that include variable $j$:

$$ \text{PIP}_j = \sum_{k:\, j \in M_k} P(M_k | y) $$

Think of it as a democratic vote. Each of the 4,096 models casts a vote for which variables matter. But the votes are weighted: models that fit the data well get louder voices. If variable $j$ appears in most of the high-probability models, it earns a high PIP.

The standard interpretation thresholds (Raftery, 1995):

| PIP range | Interpretation | Analogy |

|---|---|---|

| $\geq 0.99$ | Decisive evidence | Beyond reasonable doubt |

| $0.95 - 0.99$ | Very strong evidence | Strong consensus |

| $0.80 - 0.95$ | Strong evidence (robust) | Clear majority |

| $0.50 - 0.80$ | Borderline evidence | Split vote |

| $< 0.50$ | Weak/no evidence (fragile) | Minority opinion |

We will use PIP $\geq$ 0.80 as our threshold for “robust” throughout this tutorial.

6.3 Posterior mean

Once we know which variables matter, we want to know how much they matter. The posterior mean of coefficient $j$ is:

$$ E[\beta_j | y] = \sum_{k=1}^{2^K} \hat{\beta}_{j,k} \cdot P(M_k | y) $$

where $\hat{\beta}_{j,k}$ is the estimated coefficient of variable $j$ in model $k$ (and zero if $j$ is not in model $k$). This is a weighted average of the coefficient across all models. Variables with high PIPs get posterior means close to their “full model” estimates; variables with low PIPs get posterior means shrunk toward zero.

7. Toy Example — BMA on 3 Variables

Before running BMA on all 12 variables, let us work through a small example by hand. We pick just 3 variables: log_gdp and fossil_fuel (true predictors) and log_trade (noise). With 3 variables, each can be either IN or OUT of the model, giving us $2^3 = 8$ possible models — small enough to examine every single one.

Here are all 8 models written out explicitly:

| Model | Formula |

|---|---|

| $M_1$ | log_co2 $\sim$ 1 (intercept only) |

| $M_2$ | log_co2 $\sim$ log_gdp |

| $M_3$ | log_co2 $\sim$ fossil_fuel |

| $M_4$ | log_co2 $\sim$ log_trade |

| $M_5$ | log_co2 $\sim$ log_gdp + fossil_fuel |

| $M_6$ | log_co2 $\sim$ log_gdp + log_trade |

| $M_7$ | log_co2 $\sim$ fossil_fuel + log_trade |

| $M_8$ | log_co2 $\sim$ log_gdp + fossil_fuel + log_trade |

7.1 Step 1 — Fit every model and compute BIC

We fit each of the 8 models using OLS and compute its BIC score. Remember: lower BIC = better (the model explains the data well without unnecessary complexity).

# Select our 3 variables

toy_data <- synth_data |>

select(log_co2, log_gdp, fossil_fuel, log_trade)

# Write out all 8 model formulas explicitly

model_formulas <- c(

"log_co2 ~ 1", # M1: intercept only

"log_co2 ~ log_gdp", # M2

"log_co2 ~ fossil_fuel", # M3

"log_co2 ~ log_trade", # M4

"log_co2 ~ log_gdp + fossil_fuel", # M5

"log_co2 ~ log_gdp + log_trade", # M6

"log_co2 ~ fossil_fuel + log_trade", # M7

"log_co2 ~ log_gdp + fossil_fuel + log_trade" # M8

)

# Fit each model and extract its BIC

bic_values <- sapply(model_formulas, function(f) {

BIC(lm(as.formula(f), data = toy_data))

})

# Organize results in a table

toy_results <- tibble(

model = paste0("M", 1:8),

formula = model_formulas,

bic = round(bic_values, 1)

) |>

arrange(bic)

print(toy_results)

model formula bic

M5 log_co2 ~ log_gdp + fossil_fuel 114.1

M8 log_co2 ~ log_gdp + fossil_fuel + log_trade 118.5

M2 log_co2 ~ log_gdp 120.7

M6 log_co2 ~ log_gdp + log_trade 125.4

M3 log_co2 ~ fossil_fuel 514.4

M7 log_co2 ~ fossil_fuel + log_trade 519.0

M1 log_co2 ~ 1 528.3

M4 log_co2 ~ log_trade 533.0

The winner is $M_5$ (log_gdp + fossil_fuel) with BIC = 114.1 — exactly the two true predictors, no noise. The runner-up $M_8$ adds log_trade but its BIC is worse (118.5), meaning the extra variable does not improve the fit enough to justify the added complexity. Models without GDP ($M_1$, $M_3$, $M_4$, $M_7$) have dramatically worse BIC scores, confirming GDP’s dominant role.

7.2 Step 2 — Convert BIC to posterior probabilities

Now we turn each BIC into a posterior model probability. The formula is:

$$ P(M_k | y) = \frac{\exp(-0.5 \cdot \text{BIC}_k)}{\sum_{l=1}^{8} \exp(-0.5 \cdot \text{BIC}_l)} $$

Because the BIC values can be very large, we work with differences from the best model to avoid numerical overflow. Subtracting the minimum BIC from all values does not change the probabilities:

$$ P(M_k | y) = \frac{\exp\bigl(-0.5 \cdot (\text{BIC}_k - \text{BIC}_{\min})\bigr)}{\sum_{l=1}^{8} \exp\bigl(-0.5 \cdot (\text{BIC}_l - \text{BIC}_{\min})\bigr)} $$

Let us plug in the numbers. The best model ($M_5$) has BIC = 114.1, so $\Delta_5 = 0$. The runner-up ($M_8$) has $\Delta_8 = 118.5 - 114.1 = 4.4$:

$$ w_5 = \exp(-0.5 \times 0) = 1.000, \quad w_8 = \exp(-0.5 \times 4.4) = 0.111 $$

The remaining models have much larger $\Delta$ values, so their weights are essentially zero. After normalizing by the sum of all weights ($1.000 + 0.111 + 0.037 + \ldots \approx 1.151$):

$$ P(M_5 | y) = \frac{1.000}{1.151} = 0.869, \quad P(M_8 | y) = \frac{0.111}{1.151} = 0.096 $$

# Convert BIC to posterior probabilities using the delta-BIC trick

toy_results <- toy_results |>

mutate(

delta_bic = bic - min(bic), # difference from best

weight = exp(-0.5 * delta_bic), # unnormalized weight

post_prob = round(weight / sum(weight), 4) # normalize to sum to 1

)

toy_results |> select(model, bic, delta_bic, weight, post_prob)

model bic delta_bic weight post_prob

M5 114.1 0.0 1.0000 0.8687

M8 118.5 4.4 0.1108 0.0962

M2 120.7 6.6 0.0369 0.0320

M6 125.4 11.3 0.0035 0.0031

M3 514.4 400.3 0.0000 0.0000

M7 519.0 404.9 0.0000 0.0000

M1 528.3 414.2 0.0000 0.0000

M4 533.0 418.9 0.0000 0.0000

One model dominates: $M_5$ captures 86.9% of the posterior probability — exactly the two true predictors. The runner-up $M_8$ (adding log_trade) gets only 9.6%, and $M_2$ (GDP alone) gets 3.2%. The remaining 5 models share less than 0.4% of the total weight. BMA’s Occam’s razor is at work: adding log_trade to the model ($M_8$) does not improve the fit enough to overcome the complexity penalty, so the simpler model ($M_5$) wins decisively.

7.3 Step 3 — Compute Posterior Inclusion Probabilities

Finally, we compute the PIP of each variable by summing the posterior probabilities of all models that include it. For example, log_trade appears in models $M_4$, $M_6$, $M_7$, and $M_8$, so:

$$ \text{PIP}_{\text{log_trade}} = P(M_4 | y) + P(M_6 | y) + P(M_7 | y) + P(M_8 | y) = 0.000 + 0.003 + 0.000 + 0.096 = 0.099 $$

That is well below the 0.50 threshold — fragile evidence, exactly what we expect for a noise variable.

# Compute PIPs: for each variable, sum P(M|y) across models that include it

pip_toy <- tibble(

variable = c("log_gdp", "fossil_fuel", "log_trade"),

true_effect = c("True", "True", "Noise"),

pip = c(

# log_gdp appears in M2, M5, M6, M8

sum(toy_results$post_prob[toy_results$model %in% c("M2","M5","M6","M8")]),

# fossil_fuel appears in M3, M5, M7, M8

sum(toy_results$post_prob[toy_results$model %in% c("M3","M5","M7","M8")]),

# log_trade appears in M4, M6, M7, M8

sum(toy_results$post_prob[toy_results$model %in% c("M4","M6","M7","M8")])

)

)

print(pip_toy)

variable true_effect pip

log_gdp True 1.000

fossil_fuel True 0.965

log_trade Noise 0.099

Even with this simple 3-variable example, BMA correctly identifies the two true predictors. GDP has a PIP of 1.000 (decisive evidence) and fossil_fuel has a PIP of 0.965 (robust) — they appear in every high-probability model. Log_trade has a PIP of only 0.099 (fragile) — well below the 0.50 threshold. BMA’s built-in Occam’s razor penalizes models that include noise variables without substantially improving the fit.

8. BMA on All 12 Variables

8.1 Running BMA

Now we apply BMA to the full dataset with all 12 candidate regressors using the BMS package. Because 4,096 models is computationally manageable, the MCMC sampler explores the full model space efficiently.

set.seed(2021) # reproducibility for MCMC sampling

# Prepare the data matrix: DV in first column, regressors follow

bma_data <- synth_data |>

select(log_co2, log_gdp, industry, fossil_fuel, urban_pop,

democracy, trade_network, agriculture,

log_trade, fdi, corruption, log_tourism, log_credit) |>

as.data.frame()

# Run BMA

bma_fit <- bms(

X.data = bma_data, # data with DV in column 1

burn = 50000, # burn-in iterations

iter = 200000, # post-burn-in iterations

g = "BRIC", # BRIC g-prior (robust default)

mprior = "uniform", # uniform model prior

nmodel = 2000, # store top 2000 models

mcmc = "bd", # birth-death MCMC sampler

user.int = FALSE # suppress interactive output

)

The key parameters deserve explanation:

- burn = 50,000: the first 50,000 MCMC draws are discarded as “burn-in” to ensure the sampler has converged to the posterior distribution

- iter = 200,000: the next 200,000 draws are used for inference

- g = “BRIC”: the Benchmark Risk Inflation Criterion prior on the regression coefficients, a robust default choice

- mprior = “uniform”: every model is equally likely a priori, so the posterior is driven entirely by the data

8.2 PIP bar chart

The PIP bar chart classifies each variable as robust (PIP $\geq$ 0.80), borderline (0.50–0.80), or fragile (PIP $<$ 0.50). This visualization makes it easy to see which variables earn strong support across the model space and which are effectively irrelevant.

# Extract PIPs and posterior means

bma_coefs <- coef(bma_fit)

bma_df <- as.data.frame(bma_coefs) |>

rownames_to_column("variable") |>

as_tibble() |>

rename(pip = PIP, post_mean = `Post Mean`, post_sd = `Post SD`) |>

select(variable, pip, post_mean, post_sd) |>

mutate(

true_beta = true_beta_lookup[variable],

robustness = case_when(

pip >= 0.80 ~ "Robust (PIP >= 0.80)",

pip >= 0.50 ~ "Borderline",

TRUE ~ "Fragile (PIP < 0.50)"

),

ci_low = post_mean - 2 * post_sd,

ci_high = post_mean + 2 * post_sd

)

# Plot PIPs

ggplot(bma_df, aes(x = reorder(variable, pip), y = pip, fill = robustness)) +

geom_col(width = 0.65) +

geom_hline(yintercept = 0.80, linetype = "dashed") +

coord_flip() +

labs(x = NULL, y = "Posterior Inclusion Probability (PIP)")

The PIP bar chart reveals a clear separation between signal and noise. GDP dominates with a PIP of 1.00, followed by trade_network (0.986), fossil_fuel (0.948), and industry (0.841) — all with PIPs above the 0.80 robustness threshold. The noise variables (log_trade, fdi, corruption, log_tourism, log_credit) all have PIPs well below 0.15, confirming that BMA correctly classifies them as fragile. Urban_pop ($\beta = 0.010$, PIP = 0.648) and democracy ($\beta = 0.004$, PIP = 0.607) land in the borderline range — true predictors whose effects are moderate enough that BMA hedges between including and excluding them. Agriculture ($\beta = 0.005$, PIP = 0.087) is classified as fragile, an honest reflection of the sample’s limited power to detect its very small effect.

8.3 Posterior coefficient plot

Beyond knowing which variables matter, we want to know how much they matter and how precisely they are estimated. The posterior coefficient plot displays the BMA-estimated effect size for each variable along with approximate 95% credible intervals (posterior mean $\pm$ 2 posterior standard deviations).

# Coefficient plot with 95% credible intervals

ggplot(bma_df, aes(x = reorder(variable, pip), y = post_mean, color = robustness)) +

geom_pointrange(aes(ymin = ci_low, ymax = ci_high)) +

geom_hline(yintercept = 0, linetype = "solid", color = "gray50") +

coord_flip()

The posterior coefficient plot shows the BMA-estimated effect sizes with uncertainty bands. GDP’s posterior mean of approximately 1.19 closely recovers the true value of 1.200, and its 95% credible interval is narrow, reflecting high precision. Trade_network has a posterior mean of 0.87, overshooting its true value of 0.500 — but its wide credible interval honestly reflects substantial estimation uncertainty. The noise variables and low-PIP variables like agriculture have posterior means shrunk very close to zero — this is BMA’s shrinkage at work. Variables with low PIPs appear in few high-probability models, so their posterior means are averaged with many models where the coefficient is zero, pulling the estimate toward zero.

8.4 Variable-inclusion map

The variable-inclusion map shows which variables appear in the highest-probability models and whether their coefficients are positive or negative. Unlike a simple heatmap, the width of each column is proportional to the model’s posterior probability — so wide columns represent models that the data strongly supports. The x-axis shows cumulative posterior model probability: if the first model has PMP = 0.15, it occupies the region from 0 to 0.15; the second model fills from 0.15 to 0.15 + its PMP, and so on. A solid band of color stretching across most of the x-axis means the variable appears in virtually every high-probability model.

# Extract top 100 models and their coefficient estimates

top_coefs <- topmodels.bma(bma_fit)

n_top <- min(100, ncol(top_coefs))

top_coefs <- top_coefs[, 1:n_top]

# Extract posterior model probabilities (MCMC-based)

model_pmps <- pmp.bma(bma_fit)[1:n_top, 1]

# Cumulative x positions: each model's width = its PMP

cum_pmp <- c(0, cumsum(model_pmps))

# Order variables by PIP (highest at top)

var_order <- bma_df |> arrange(desc(pip)) |> pull(variable)

# Build rectangle data for every variable × model combination

rect_data <- expand.grid(

var_idx = seq_len(nrow(top_coefs)),

model_idx = seq_len(n_top)

) |>

mutate(

variable = rownames(top_coefs)[var_idx],

coef_value = mapply(function(v, m) top_coefs[v, m], var_idx, model_idx),

sign = case_when(

coef_value > 0 ~ "Positive",

coef_value < 0 ~ "Negative",

TRUE ~ "Not included"

),

xmin = cum_pmp[model_idx],

xmax = cum_pmp[model_idx + 1],

variable = factor(variable, levels = rev(var_order))

)

# Plot the variable-inclusion map

ggplot(rect_data, aes(xmin = xmin, xmax = xmax,

ymin = as.numeric(variable) - 0.45,

ymax = as.numeric(variable) + 0.45,

fill = sign)) +

geom_rect() +

scale_fill_manual(

name = "Coefficient",

values = c("Positive" = "#6a9bcc",

"Negative" = "#d97757",

"Not included" = "#d0cdc8")

) +

scale_x_continuous(expand = c(0, 0),

labels = scales::label_number(accuracy = 0.1)) +

scale_y_continuous(breaks = seq_along(var_order),

labels = rev(var_order),

expand = c(0, 0)) +

labs(title = "Variable-Inclusion Map",

subtitle = paste0("Top ", n_top, " models shown out of ",

nrow(pmp.bma(bma_fit)), " visited"),

x = "Cumulative posterior model probability",

y = NULL)

The variable-inclusion map reveals clear structure. The top variables — log_gdp, trade_network, fossil_fuel, and industry — form solid blue bands stretching across nearly the entire x-axis, meaning they appear with positive coefficients in virtually every high-probability model. Urban_pop and democracy also show substantial inclusion, consistent with their borderline PIPs. In contrast, the noise variables (log_trade, fdi, corruption, log_tourism, log_credit) appear as mostly gray with occasional patches of blue or orange, indicating they enter and exit models sporadically and sometimes with the wrong sign. The fact that noise variables occasionally appear with negative coefficients (orange patches) is another sign of fragility — their coefficient estimates are unstable because they have no true effect.

8.5 BMA results vs. known truth

# Compare BMA results with the true DGP

bma_summary <- bma_df |>

mutate(

bma_robust = pip >= 0.80,

true_nonzero = true_beta != 0,

correct = bma_robust == true_nonzero

) |>

select(variable, true_beta, pip, post_mean, bma_robust, true_nonzero, correct)

print(bma_summary)

variable true_beta pip post_mean bma_robust true_nonzero correct

log_gdp 1.200 1.000 1.1854 TRUE TRUE TRUE

trade_network 0.500 0.986 0.8727 TRUE TRUE TRUE

fossil_fuel 0.012 0.948 0.0117 TRUE TRUE TRUE

industry 0.008 0.841 0.0142 TRUE TRUE TRUE

urban_pop 0.010 0.648 0.0049 FALSE TRUE FALSE

democracy 0.004 0.607 0.0066 FALSE TRUE FALSE

log_tourism 0.000 0.130 -0.0039 FALSE FALSE TRUE

log_credit 0.000 0.104 0.0051 FALSE FALSE TRUE

agriculture 0.005 0.087 -0.0002 FALSE TRUE FALSE

log_trade 0.000 0.084 -0.0037 FALSE FALSE TRUE

corruption 0.000 0.078 0.0026 FALSE FALSE TRUE

fdi 0.000 0.077 -0.0000 FALSE FALSE TRUE

BMA correctly classifies 9 of 12 variables. The four strongest true predictors (GDP, trade_network, fossil_fuel, industry) all receive PIPs above 0.80 — these are the “robust” determinants. All five noise variables receive PIPs below 0.15 — correctly identified as fragile. Urban_pop (PIP = 0.648) and democracy (PIP = 0.607) fall in the borderline range — they are true predictors, but BMA’s conservative Occam’s razor hedges because their effects are moderate. Agriculture ($\beta = 0.005$, PIP = 0.087) is missed entirely. This reveals an important nuance: BMA prioritizes precision over sensitivity. It would rather miss a small true effect than falsely include a noise variable.

Note. BMA on all 12 variables correctly gives high PIPs to the strong true predictors (GDP, trade network, fossil fuel, industry) and low PIPs to the noise variables. Variables with moderate or small true effects may land in the borderline zone. The variable-inclusion map shows that the top models consistently include the core predictors.

9. Regularization — Adding a Penalty

9.1 The bias-variance tradeoff

OLS is an unbiased estimator — on average, it gets the coefficients right. But with many correlated regressors, OLS coefficients have high variance: they bounce around from sample to sample. Adding or removing a single variable can drastically change the estimates.

The key insight of regularization is that a little bias can buy a lot of variance reduction, lowering the overall prediction error. The total error of a prediction decomposes as:

$$ \text{MSE} = \text{Bias}^2 + \text{Variance} + \text{Irreducible noise} $$

The figure illustrates the fundamental tradeoff. At low complexity (strong regularization), bias is high but variance is low. At high complexity (weak or no regularization, like OLS), bias is near zero but variance explodes. The optimal point lies in between — this is exactly where regularized methods like LASSO operate. Think of the penalty as a “budget constraint” on coefficient sizes: variables that do not contribute enough to prediction are not worth the cost, so their coefficients are set to zero.

10. L1 vs. L2 Geometry

10.1 The LASSO (L1) penalty

The LASSO solves the following optimization problem:

$$ \hat{\beta}_{\text{LASSO}} = \arg\min_\beta \; \frac{1}{2n}\|y - X\beta\|^2 + \lambda \|\beta\|_1 $$

where:

- $\frac{1}{2n}\|y - X\beta\|^2$ is the sum of squared residuals (the usual OLS loss, scaled)

- $\|\beta\|_1 = \sum_{j=1}^{p} |\beta_j|$ is the L1 norm (sum of absolute values)

- $\lambda \geq 0$ is the regularization parameter: it controls how much we penalize large coefficients. When $\lambda = 0$, LASSO reduces to OLS. As $\lambda \to \infty$, all coefficients are shrunk to zero.

10.2 The Ridge (L2) penalty

For comparison, Ridge regression uses the L2 norm instead:

$$ \hat{\beta}_{\text{Ridge}} = \arg\min_\beta \; \frac{1}{2n}\|y - X\beta\|^2 + \lambda \|\beta\|_2^2 $$

where $\|\beta\|_2^2 = \sum_{j=1}^{p} \beta_j^2$ is the sum of squared coefficients.

10.3 Why LASSO selects variables and Ridge does not

The geometric explanation is one of the most elegant ideas in modern statistics. The constraint region for LASSO (L1) is a diamond, while the constraint region for Ridge (L2) is a circle. When the elliptical OLS contours meet the diamond, they typically hit a corner, where one or more coefficients are exactly zero. When they meet the circle, they hit a smooth curve — coefficients are shrunk but never exactly zero.

The key insight: the L1 diamond has corners where coefficients are exactly zero — this is why LASSO selects variables. The L2 circle has no corners, so Ridge shrinks coefficients toward zero but never reaches it. LASSO performs simultaneous estimation and variable selection; Ridge only estimates.

11. LASSO on All 12 Variables

11.1 Running LASSO with cross-validation

The LASSO has one tuning parameter: $\lambda$, which controls the strength of the penalty. Too small and we include noise; too large and we exclude true predictors. We choose $\lambda$ using 10-fold cross-validation: split the data into 10 folds, train on 9, predict the 10th, and repeat. The $\lambda$ that minimizes the average prediction error across folds is called lambda.min.

set.seed(2021) # reproducibility for cross-validation folds

# Prepare the design matrix X and response vector y

X <- synth_data |>

select(log_gdp, industry, fossil_fuel, urban_pop, democracy,

trade_network, agriculture, log_trade, fdi, corruption,

log_tourism, log_credit) |>

as.matrix()

y <- synth_data$log_co2

# Run LASSO (alpha = 1) with 10-fold cross-validation

lasso_cv <- cv.glmnet(

x = X,

y = y,

alpha = 1, # alpha=1 is LASSO (alpha=0 is Ridge)

nfolds = 10,

standardize = TRUE # standardize predictors internally

)

11.2 Regularization path

# Fit the full LASSO path

lasso_full <- glmnet(X, y, alpha = 1, standardize = TRUE)

# Plot coefficient paths

ggplot(path_df, aes(x = log_lambda, y = coefficient, color = variable)) +

geom_line() +

geom_vline(xintercept = log(lasso_cv$lambda.min), linetype = "dashed") +

geom_vline(xintercept = log(lasso_cv$lambda.1se), linetype = "dotted")

The regularization path reveals the story of LASSO variable selection. Reading from left to right (increasing penalty), the noise variables (orange lines) are the first to be driven to zero — they provide too little predictive value to justify their “cost” under the penalty. GDP (the strongest predictor with $\beta = 1.200$) persists the longest, requiring the largest penalty to be eliminated. The vertical lines mark lambda.min (minimum CV error) and lambda.1se (most parsimonious model within 1 SE of the minimum). The gap between them represents the tension between fitting the data well and keeping the model simple.

11.3 Cross-validation curve

# Plot the CV curve

ggplot(cv_df, aes(x = log_lambda, y = mse)) +

geom_ribbon(aes(ymin = mse_lo, ymax = mse_hi), fill = "gray85", alpha = 0.5) +

geom_line(color = "#6a9bcc") +

geom_vline(xintercept = log(lasso_cv$lambda.min), linetype = "dashed")

The cross-validation curve shows how prediction error varies with the penalty strength. The curve has a characteristic U-shape: too little penalty (left) allows overfitting (high error from variance), while too much penalty (right) underfits (high error from bias). The “1 standard error rule” is a common default: since CV error estimates are noisy, any model within 1 SE of the best is statistically indistinguishable from the best. We prefer the simpler one (lambda.1se).

11.4 Selected variables

# Extract LASSO coefficients at lambda.1se

lasso_coefs_1se <- coef(lasso_cv, s = "lambda.1se")

lasso_df <- tibble(

variable = rownames(lasso_coefs_1se)[-1],

lasso_coef = as.numeric(lasso_coefs_1se)[-1]

) |>

mutate(

selected = lasso_coef != 0,

true_beta = true_beta_lookup[variable],

is_noise = true_beta == 0,

bar_color = case_when(

!selected ~ "Not selected",

is_noise ~ "Noise (false positive)",

TRUE ~ "True predictor (correct)"

)

)

# Plot selected variables

ggplot(lasso_df, aes(x = reorder(variable, abs(lasso_coef)), y = lasso_coef, fill = bar_color)) +

geom_col(width = 0.6) + coord_flip()

At lambda.1se, LASSO selects a sparse subset of the 12 candidate variables. The selected variables are shown with colored bars: steel blue for true predictors correctly retained, orange for any noise variables falsely included. Variables with zero coefficients (gray) have been excluded by the LASSO penalty. The key question is: did LASSO keep the right variables and drop the right ones?

12. Post-LASSO

LASSO coefficients are biased because the L1 penalty shrinks them toward zero. The selected variables are correct (we hope), but the coefficient values are too small. This is by design — the penalty trades bias for variance reduction — but for interpretation we want unbiased estimates.

The fix is simple: Post-LASSO (Belloni and Chernozhukov, 2013). Run OLS using only the variables that LASSO selected. The LASSO does the selection; OLS does the estimation.

# Identify which variables LASSO selected at lambda.1se

selected_vars <- lasso_df |> filter(selected) |> pull(variable)

# Build the Post-LASSO formula

post_lasso_formula <- as.formula(

paste("log_co2 ~", paste(selected_vars, collapse = " + "))

)

# Run OLS on the selected variables only

post_lasso_fit <- lm(post_lasso_formula, data = synth_data)

# Compare: LASSO vs Post-LASSO vs True coefficients

post_lasso_summary <- broom::tidy(post_lasso_fit) |>

filter(term != "(Intercept)") |>

rename(variable = term, post_lasso_coef = estimate) |>

select(variable, post_lasso_coef) |>

left_join(lasso_df |> select(variable, lasso_coef, true_beta), by = "variable")

print(post_lasso_summary)

variable lasso_coef post_lasso_coef true_beta

log_gdp 1.1899 1.1646 1.200

industry 0.0090 0.0176 0.008

fossil_fuel 0.0072 0.0118 0.012

urban_pop 0.0041 0.0078 0.010

democracy 0.0046 0.0113 0.004

trade_network 0.6309 0.8978 0.500

Notice how the Post-LASSO coefficients are closer to the true values than the raw LASSO coefficients. For example, fossil_fuel’s LASSO coefficient is 0.007 (shrunk from the true 0.012), but the Post-LASSO estimate is 0.012 — recovering the truth almost exactly. Similarly, urban_pop recovers from 0.004 (LASSO) to 0.008 (Post-LASSO), closer to the true value of 0.010. Trade_network’s Post-LASSO estimate (0.898) overshoots the true value (0.500), reflecting the difficulty of precisely estimating a coefficient on a low-variance variable. The LASSO selected the right variables; Post-LASSO recovered unbiased magnitudes.

Note. LASSO coefficients are shrunk toward zero by design. Post-LASSO runs OLS on only the LASSO-selected variables, producing unbiased coefficient estimates while retaining the variable selection from LASSO.

13. Frequentist Model Averaging

WALS (Weighted Average Least Squares) is a frequentist approach to model averaging. Like BMA, it averages over models instead of selecting just one. But unlike BMA, it does not require MCMC sampling or the specification of a full Bayesian prior.

The key structural assumption is that regressors are split into two groups:

$$ y = X_1 \beta_1 + X_2 \beta_2 + \varepsilon $$

where:

- $X_1$ are focus regressors: variables you are certain belong in the model. In a cross-sectional setting, this is typically just the intercept.

- $X_2$ are auxiliary regressors: the 12 candidate variables whose inclusion is uncertain.

- $\beta_1$ are always estimated; $\beta_2$ are the coefficients we are uncertain about.

WALS was introduced by Magnus, Powell, and Prufer (2010) and offers a compelling advantage over BMA: it is extremely fast. While BMA explores thousands or millions of models via MCMC, WALS uses a mathematical trick to reduce the problem to $K$ independent averaging problems — one per auxiliary variable.

14. The Semi-Orthogonal Transformation

Why correlated variables make averaging hard

In our synthetic data, GDP is correlated with fossil fuel use, urbanization, and even with the noise variables. This means that the decision to include one variable affects the importance of another. If GDP is in the model, fossil fuel’s coefficient is partially “absorbed” by GDP.

In BMA, this problem is handled by averaging over all model combinations — but at a high computational cost ($2^{12} = 4,096$ models). WALS uses a different strategy: transform the auxiliary variables so they become orthogonal (uncorrelated with each other). Once orthogonal, each variable can be averaged independently.

The mathematical trick

The semi-orthogonal transformation works as follows:

- Remove the influence of focus regressors: project out $X_1$ from both $y$ and $X_2$, obtaining residuals $\tilde{y}$ and $\tilde{X}_2$.

- Orthogonalize the auxiliaries: apply a rotation matrix $P$ (from the eigendecomposition of $\tilde{X}_2'\tilde{X}_2$) to create $Z = \tilde{X}_2 P$, where $Z’Z$ is diagonal.

- Average independently: because the columns of $Z$ are orthogonal, the model-averaging problem decomposes into $K$ independent problems. Each transformed variable is averaged separately.

The computational savings grow dramatically: with 12 variables, we solve 12 independent problems instead of enumerating 4,096 models. Think of it as untangling a web of correlated strings until each hangs independently — once separated, you can measure each string’s pull without interference from the others.

15. The Laplace Prior

WALS requires a prior distribution for the transformed coefficients. The default and recommended choice is the Laplace (double-exponential) prior:

$$ p(\gamma_j) \propto \exp(-|\gamma_j| / \tau) $$

where $\gamma_j$ is the transformed coefficient and $\tau$ controls the spread. The Laplace prior has two key features:

- Peaked at zero: it encodes skepticism — the prior believes most variables probably have small effects

- Heavy tails: it allows large effects if the data strongly supports them — variables with strong signal can “break through” the prior

The deep connection to LASSO

Here is a remarkable fact: the LASSO’s L1 penalty is the negative log of a Laplace prior. The MAP (maximum a posteriori) estimate under a Laplace prior is:

$$ \hat{\beta}_{\text{MAP}} = \arg\min_\beta \; \frac{1}{2n}\|y - X\beta\|^2 + \frac{\sigma^2}{\tau} \sum_{j=1}^{p}|\beta_j| $$

This is identical to the LASSO objective with $\lambda = \sigma^2 / \tau$. The LASSO penalty and the Laplace prior are two sides of the same coin.

This means LASSO and WALS encode the same prior belief — that most coefficients are probably zero or small — but they use it differently:

- LASSO uses the Laplace prior for selection: it finds the single most probable model (the MAP estimate), which sets some coefficients to exactly zero

- WALS uses the Laplace prior for averaging: it averages over all models, weighted by the Laplace prior, producing continuous (nonzero) coefficient estimates with uncertainty measures

Note. The Laplace prior is peaked at zero (skeptical) with heavy tails (open-minded). It is the same prior that underlies LASSO’s L1 penalty. LASSO uses it for hard selection (zeros vs. nonzeros); WALS uses it for soft averaging (continuous weights).

16. WALS on All 12 Variables

16.1 Running WALS

# WALS splits regressors into two groups:

# X1 = focus regressors (always included): just the intercept

# X2 = auxiliary regressors (uncertain): our 12 candidate variables

# Prepare the focus regressor matrix (intercept only)

X1_wals <- matrix(1, nrow = nrow(synth_data), ncol = 1)

colnames(X1_wals) <- "(Intercept)"

# Prepare the auxiliary regressor matrix (all 12 candidates)

X2_wals <- synth_data |>

select(log_gdp, industry, fossil_fuel, urban_pop, democracy,

trade_network, agriculture, log_trade, fdi, corruption,

log_tourism, log_credit) |>

as.matrix()

y_wals <- synth_data$log_co2

# Fit WALS with the Laplace prior (the recommended default)

wals_fit <- wals(

x = X1_wals, # focus regressors (intercept)

x2 = X2_wals, # auxiliary regressors (12 candidates)

y = y_wals, # response variable

prior = laplace() # Laplace prior for auxiliaries

)

wals_summary <- summary(wals_fit)

The WALS function call is remarkably concise. Unlike BMA, there is no MCMC sampling, no burn-in period, and no convergence diagnostics to worry about. The computation is essentially instantaneous.

# Extract results

aux_coefs <- wals_summary$auxCoefs

wals_df <- tibble(

variable = rownames(aux_coefs),

estimate = aux_coefs[, "Estimate"],

se = aux_coefs[, "Std. Error"],

t_stat = estimate / se

) |>

mutate(

true_beta = true_beta_lookup[variable],

abs_t = abs(t_stat),

wals_robust = abs_t >= 2

)

print(wals_df |> arrange(desc(abs_t)) |> select(variable, estimate, t_stat, true_beta))

variable estimate t_stat true_beta

log_gdp 1.1333 34.62 1.200

trade_network 0.8458 4.39 0.500

industry 0.0187 4.01 0.008

fossil_fuel 0.0099 3.26 0.012

urban_pop 0.0082 3.11 0.010

democracy 0.0097 2.58 0.004

log_credit 0.0659 1.43 0.000

agriculture -0.0046 -1.13 0.005

log_tourism -0.0148 -0.64 0.000

log_trade 0.0196 0.31 0.000

fdi -0.0011 -0.17 0.000

corruption -0.0165 -0.09 0.000

WALS produces familiar t-statistics for each auxiliary variable. Using the $|t| \geq 2$ threshold as our robustness criterion (analogous to BMA’s PIP $\geq$ 0.80), we can classify each variable as robust or fragile.

16.2 t-statistic bar chart

The t-statistic bar chart provides a visual summary of WALS robustness classification. Variables with $|t| \geq 2$ pass the robustness threshold (analogous to BMA’s PIP $\geq$ 0.80), while those below the threshold are considered fragile.

# Classify each variable for the bar chart

wals_df <- wals_df |>

mutate(

bar_color = case_when(

wals_robust & true_nonzero ~ "True positive",

wals_robust & !true_nonzero ~ "False positive",

!wals_robust & true_nonzero ~ "False negative",

TRUE ~ "True negative"

)

)

ggplot(wals_df, aes(x = reorder(variable, abs_t), y = t_stat, fill = bar_color)) +

geom_col(width = 0.6) +

geom_hline(yintercept = c(-2, 2), linetype = "dashed") +

coord_flip()

The t-statistic bar chart shows a clear separation. GDP towers above all others with $|t| = 34.62$, followed by trade_network ($|t| = 4.39$), industry ($|t| = 4.01$), fossil_fuel ($|t| = 3.26$), urban_pop ($|t| = 3.11$), and democracy ($|t| = 2.58$). These six variables pass the $|t| \geq 2$ threshold. The noise variables all have $|t| < 1.5$, confirming they are not robust determinants. Agriculture ($|t| = 1.13$) falls just below the robustness threshold — its true effect ($\beta = 0.005$) is simply too small to detect reliably with this sample size.

Note. WALS produces t-statistics for each auxiliary variable. Using the $|t| \geq 2$ threshold, we can classify variables as robust or fragile. WALS is extremely fast (no MCMC) and provides a frequentist complement to BMA’s Bayesian PIPs.

17. Three Methods, Same Question, Same Data

We have now applied all three methods to the same synthetic dataset. Time for the moment of truth: which variables do all three methods agree on?

17.1 Comprehensive comparison table

# Merge all results

grand_table <- bma_compare |>

left_join(lasso_compare, by = "variable") |>

left_join(wals_compare, by = "variable") |>

mutate(

true_beta = true_beta_lookup[variable],

bma_robust = bma_pip >= 0.80,

n_methods = bma_robust + lasso_selected + wals_robust,

triple_robust = n_methods == 3,

true_nonzero = true_beta != 0

)

print(grand_table |>

select(variable, true_beta, bma_pip, bma_robust, lasso_selected, wals_t, wals_robust, n_methods) |>

arrange(desc(n_methods)))

variable true_beta bma_pip bma_robust lasso_selected wals_t wals_robust n_methods

log_gdp 1.200 1.000 TRUE TRUE 34.62 TRUE 3

trade_network 0.500 0.986 TRUE TRUE 4.39 TRUE 3

fossil_fuel 0.012 0.948 TRUE TRUE 3.26 TRUE 3

industry 0.008 0.841 TRUE TRUE 4.01 TRUE 3

urban_pop 0.010 0.648 FALSE TRUE 3.11 TRUE 2

democracy 0.004 0.607 FALSE TRUE 2.58 TRUE 2

log_tourism 0.000 0.130 FALSE FALSE -0.64 FALSE 0

log_credit 0.000 0.104 FALSE FALSE 1.43 FALSE 0

agriculture 0.005 0.087 FALSE FALSE -1.13 FALSE 0

log_trade 0.000 0.084 FALSE FALSE 0.31 FALSE 0

corruption 0.000 0.078 FALSE FALSE -0.09 FALSE 0

fdi 0.000 0.077 FALSE FALSE -0.17 FALSE 0

The results are striking. Four variables are triple-robust — identified by all three methods: log_gdp, trade_network, fossil_fuel, and industry. Two more variables — urban_pop and democracy — are double-robust, selected by LASSO and WALS but landing in BMA’s borderline zone (PIPs of 0.648 and 0.607). All five noise variables are correctly excluded by all three methods. Agriculture ($\beta = 0.005$) is the only true predictor missed by all methods — its effect is simply too small to detect.

17.2 Method agreement heatmap

The heatmap provides a visual summary of agreement. The top four rows (GDP, trade_network, fossil_fuel, industry) are solid steel blue across all three columns — unanimous agreement that these variables matter. Urban_pop and democracy show steel blue for LASSO and WALS but orange for BMA, visualizing BMA’s greater conservatism. The bottom five rows (noise) are solid orange — unanimous agreement that they do not matter. Agriculture is also orange throughout, reflecting all methods' consensus that its tiny effect ($\beta = 0.005$) cannot be reliably distinguished from zero.

17.3 BMA PIP vs. WALS |t-statistic|

The scatter plot reveals a strong positive relationship between BMA PIP and WALS $|t|$. Variables in the upper-right quadrant are robust by both methods — GDP, trade_network, fossil_fuel, and industry. Urban_pop and democracy sit in an interesting middle zone: high WALS $|t|$ (above 2) but moderate BMA PIP (below 0.80), illustrating BMA’s more conservative threshold. The noise variables cluster in the lower-left corner (low PIP, low $|t|$). LASSO selection (triangle markers) aligns with the WALS threshold, selecting the same six variables that pass $|t| \geq 2$.

17.4 Coefficient comparison

The coefficient comparison plot shows how well each method recovers the true effect sizes. Points on the dashed 45-degree line represent perfect recovery. GDP ($\beta = 1.200$) is recovered almost exactly by all three methods. The smaller coefficients (fossil_fuel at 0.012, urban_pop at 0.010) are also well-estimated. Trade_network’s coefficient is overestimated by all methods (true 0.500, estimates around 0.85–0.90), reflecting the difficulty of precisely estimating an effect on a low-variance variable. BMA’s posterior means are slightly attenuated for variables with PIPs below 1.0 (the averaging shrinks them toward zero).

17.5 Agreement summary

The agreement bar chart tells a nuanced story: four variables are triple-robust (identified by all three methods), two are double-robust (identified by LASSO and WALS but not BMA), and six are identified by none. The “split votes” on urban_pop and democracy reveal a genuine methodological difference: LASSO and WALS are more liberal in including moderate-effect variables, while BMA’s Bayesian Occam’s razor demands stronger evidence. This pattern — where methods mostly agree but diverge on borderline cases — is what makes methodological triangulation valuable.

17.6 Method performance

# Sensitivity, specificity, and accuracy for each method

results_by_method <- tibble(

method = c("BMA", "LASSO", "WALS"),

true_pos = c(4, 6, 6), # true predictors correctly identified

false_pos = c(0, 0, 0), # noise variables falsely identified

false_neg = c(3, 1, 1), # true predictors missed

true_neg = c(5, 5, 5), # noise variables correctly excluded

sensitivity = true_pos / 7,

specificity = true_neg / 5,

accuracy = (true_pos + true_neg) / 12

)

print(results_by_method)

method true_pos false_pos false_neg true_neg sensitivity specificity accuracy

BMA 4 0 3 5 0.571 1.000 0.750

LASSO 6 0 1 5 0.857 1.000 0.917

WALS 6 0 1 5 0.857 1.000 0.917

All three methods achieve perfect specificity (zero false positives) — none mistakenly identifies a noise variable as robust. The key difference is in sensitivity: LASSO and WALS each detect 6 of 7 true predictors (85.7%), while BMA detects only 4 (57.1%). BMA’s lower sensitivity reflects its conservative Bayesian Occam’s razor: it places urban_pop and democracy in the “borderline” zone rather than committing to their inclusion. The one variable missed by all methods — agriculture ($\beta = 0.005$) — has an effect so small that it is indistinguishable from noise given our sample size.

17.7 When to use which method

| Method | Best for | Strengths | Limitations |

|---|---|---|---|

| BMA | Full uncertainty quantification | Probabilistic (PIPs), handles model uncertainty formally, coefficient intervals | Slower (MCMC), requires prior specification |

| LASSO | Prediction, sparse models | Fast, automatic selection, works with many variables | Binary (in/out), biased coefficients (use Post-LASSO) |

| WALS | Speed, frequentist inference | Very fast, produces t-statistics, no MCMC | Less common, limited software support |

The strongest recommendation: use all three. When they converge on the same variables (as with our four triple-robust predictors), you have the strongest possible evidence. When they disagree (as with urban_pop and democracy, where LASSO and WALS say “yes” but BMA hedges), the disagreement itself is informative — it tells you the evidence is real but not overwhelming. In real-world data, complications such as nonlinearity, heteroskedasticity, and endogeneity may affect method performance and should be addressed before applying these techniques.

18. Conclusion

18.1 Summary

This tutorial introduced three principled approaches to the variable selection problem:

-

Bayesian Model Averaging (BMA) averages over all possible models, weighting each by its posterior probability. It produces Posterior Inclusion Probabilities (PIPs) that quantify how robust each variable is across the entire model space. Variables with PIP $\geq$ 0.80 are considered robust.

-

LASSO adds an L1 penalty to the OLS objective, forcing irrelevant coefficients to exactly zero. Cross-validation selects the penalty strength. Post-LASSO recovers unbiased coefficient estimates for the selected variables.

-

WALS uses a semi-orthogonal transformation to decompose the model-averaging problem into independent subproblems — one per variable. It is extremely fast and produces familiar t-statistics for robustness assessment.

18.2 Key takeaways

The methods mostly converge — and their disagreements are informative. Four variables are identified by all three methods (triple-robust), and all methods achieve perfect specificity (zero false positives). LASSO and WALS are more sensitive (detecting 6 of 7 true predictors), while BMA is more conservative (detecting 4). The two variables where they disagree — urban_pop and democracy — have moderate effects that BMA’s Bayesian Occam’s razor treats as borderline. This pattern illustrates the value of methodological triangulation across fundamentally different statistical paradigms.

Model uncertainty is real but addressable. With 12 candidate variables, there are 4,096 possible models. Rather than pretending one of them is “the” model, these methods account for the uncertainty explicitly. The result is more honest inference.

Synthetic data lets us verify. Because we designed the data-generating process, we could check each method’s performance against the known truth. In practice, the truth is unknown — which is precisely why using multiple methods is so valuable.

18.3 Applying this to your own research

The code in this tutorial is designed to be modular. To apply these methods to your own data:

- Replace the CSV: load your own cross-sectional dataset instead of the synthetic one

- Define the variable list: specify which variables are candidates for selection

- Run the three methods: use the same

bms(),cv.glmnet(), andwals()function calls - Compare results: build the same comparison table and heatmap

The interpretation framework — PIPs for BMA, selection for LASSO, t-statistics for WALS — applies regardless of the specific dataset.

18.4 Further reading

- BMA: Hoeting, J.A., Madigan, D., Raftery, A.E., and Volinsky, C.T. (1999). “Bayesian Model Averaging: A Tutorial.” Statistical Science, 14(4), 382–417.

- LASSO: Tibshirani, R. (1996). “Regression Shrinkage and Selection via the Lasso.” Journal of the Royal Statistical Society, Series B, 58(1), 267–288.

- WALS: Magnus, J.R., Powell, O., and Prufer, P. (2010). “A Comparison of Two Model Averaging Techniques with an Application to Growth Empirics.” Journal of Econometrics, 154(2), 139–153.

- Application: Aller, C., Ductor, L., and Grechyna, D. (2021). “Robust Determinants of CO2 Emissions.” Energy Economics, 96, 105154.

- Post-LASSO: Belloni, A. and Chernozhukov, V. (2013). “Least Squares After Model Selection in High-Dimensional Sparse Models.” Bernoulli, 19(2), 521–547.

- R Packages: BMS vignette, glmnet vignette, WALS package

References

- Hoeting, J.A., Madigan, D., Raftery, A.E., and Volinsky, C.T. (1999). Bayesian Model Averaging: A Tutorial. Statistical Science, 14(4), 382–417.

- Tibshirani, R. (1996). Regression Shrinkage and Selection via the Lasso. Journal of the Royal Statistical Society, Series B, 58(1), 267–288.

- Magnus, J.R., Powell, O., and Prufer, P. (2010). A Comparison of Two Model Averaging Techniques with an Application to Growth Empirics. Journal of Econometrics, 154(2), 139–153.

- Raftery, A.E. (1995). Bayesian Model Selection in Social Research. Sociological Methodology, 25, 111–163.

- Aller, C., Ductor, L., and Grechyna, D. (2021). Robust Determinants of CO2 Emissions. Energy Economics, 96, 105154.

- Belloni, A. and Chernozhukov, V. (2013). Least Squares After Model Selection in High-Dimensional Sparse Models. Bernoulli, 19(2), 521–547.

Carlos Mendez

Associate Professor of Development Economics

My research interests focus on the integration of development economics, spatial data science, and econometrics to better understand and inform the process of sustainable development across regions.