Augmented Synthetic Control for Multiple Countries

Validate on a known truth, then trust the euro question

Nagoya University (GSID)

July 8, 2026

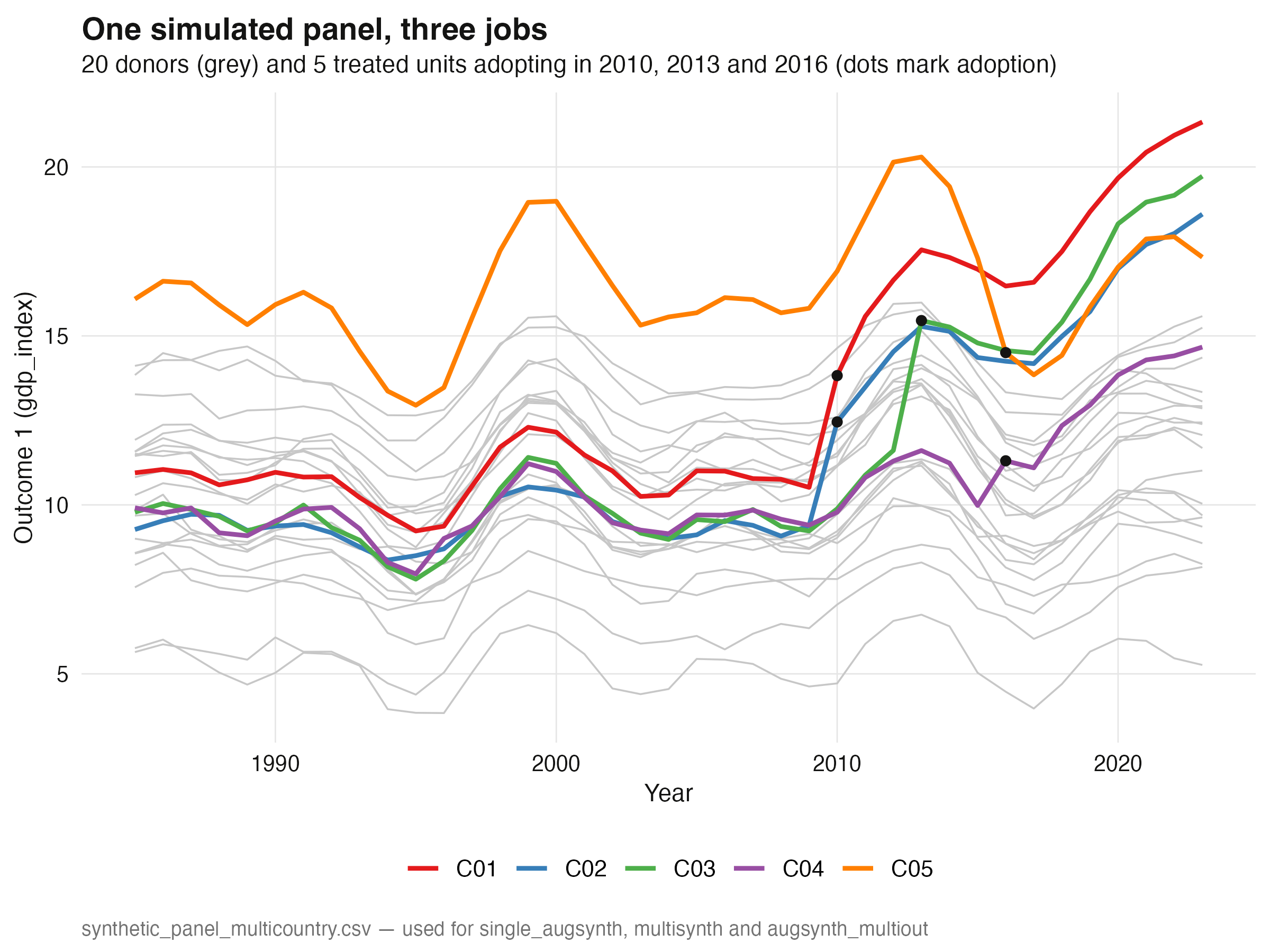

The lab: 25 countries, 39 years, a known effect injected into five of them

25 simulated paths — five treated units (colored) inside a cloud of 20 donors (grey); dots mark each adoption year.

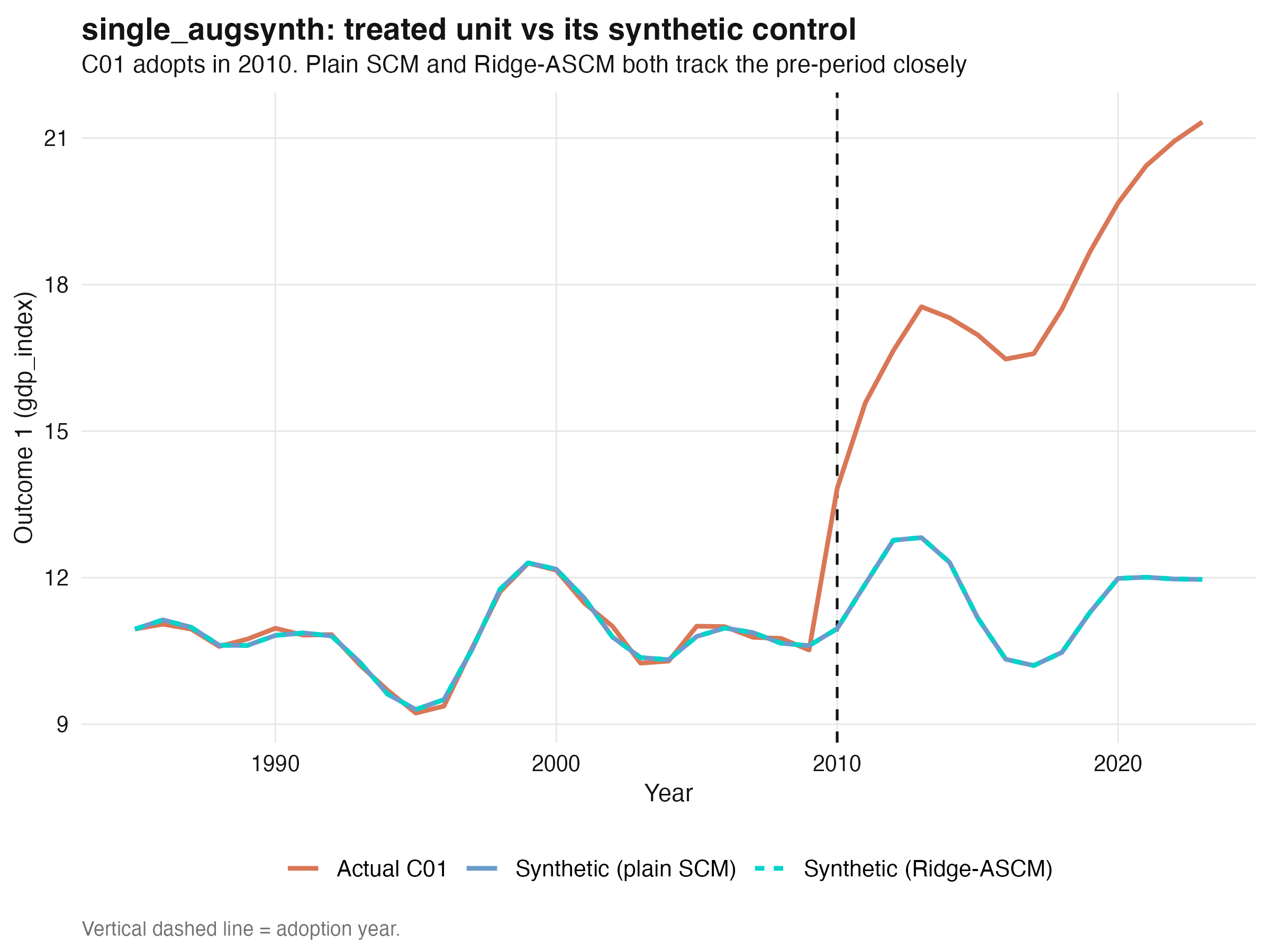

single_augsynth recovers C01’s ATT to within 0.1% — and it’s significant

C01 actual vs its synthetic control: the synthetic tracks the pre-2010 path closely, then the gap opens.

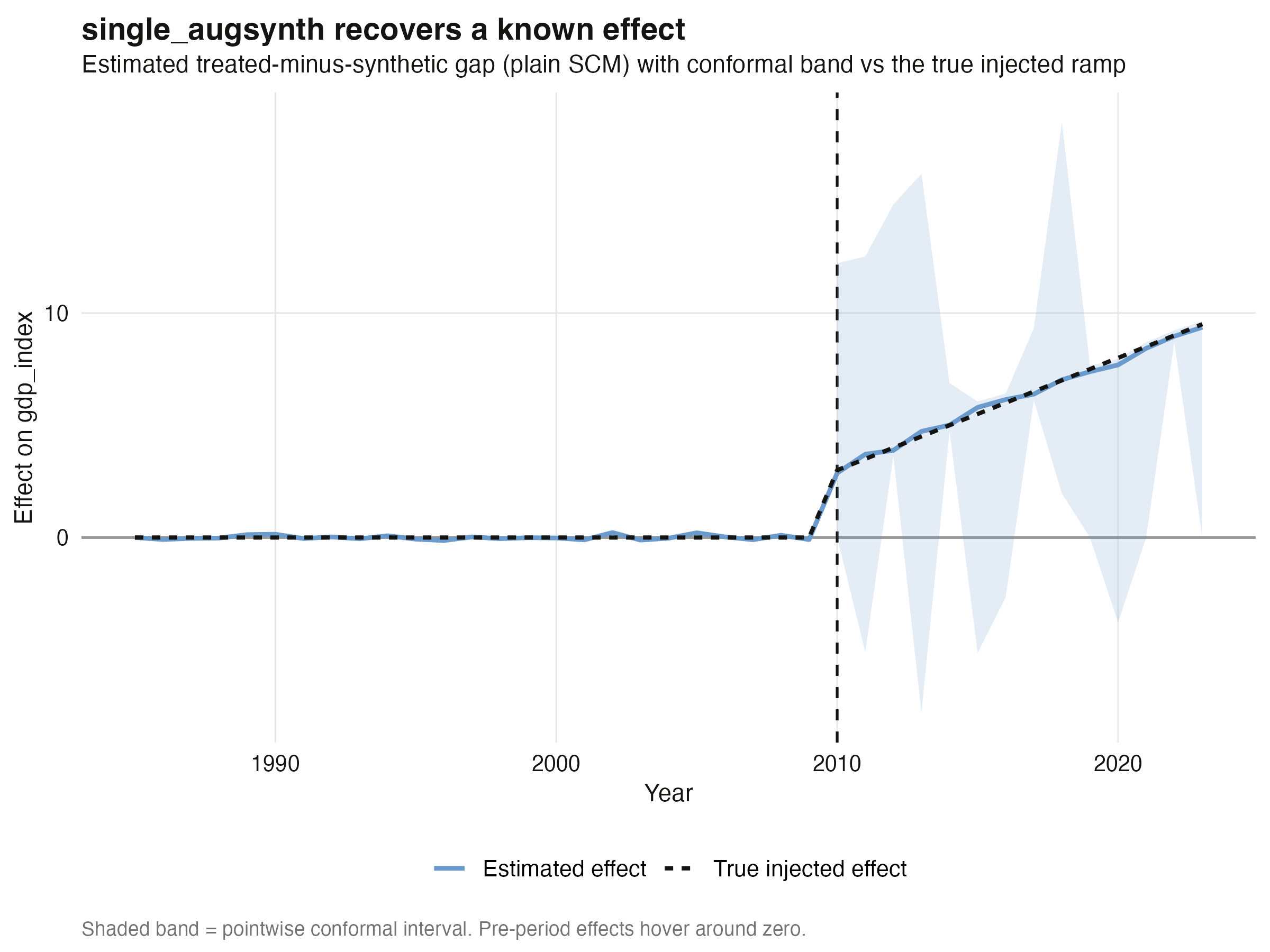

The dynamic gap lands on the true injected effect after treatment

Estimated treated-minus-synthetic gap with its conformal band, overlaid on the true injected effect — near-perfect recovery.

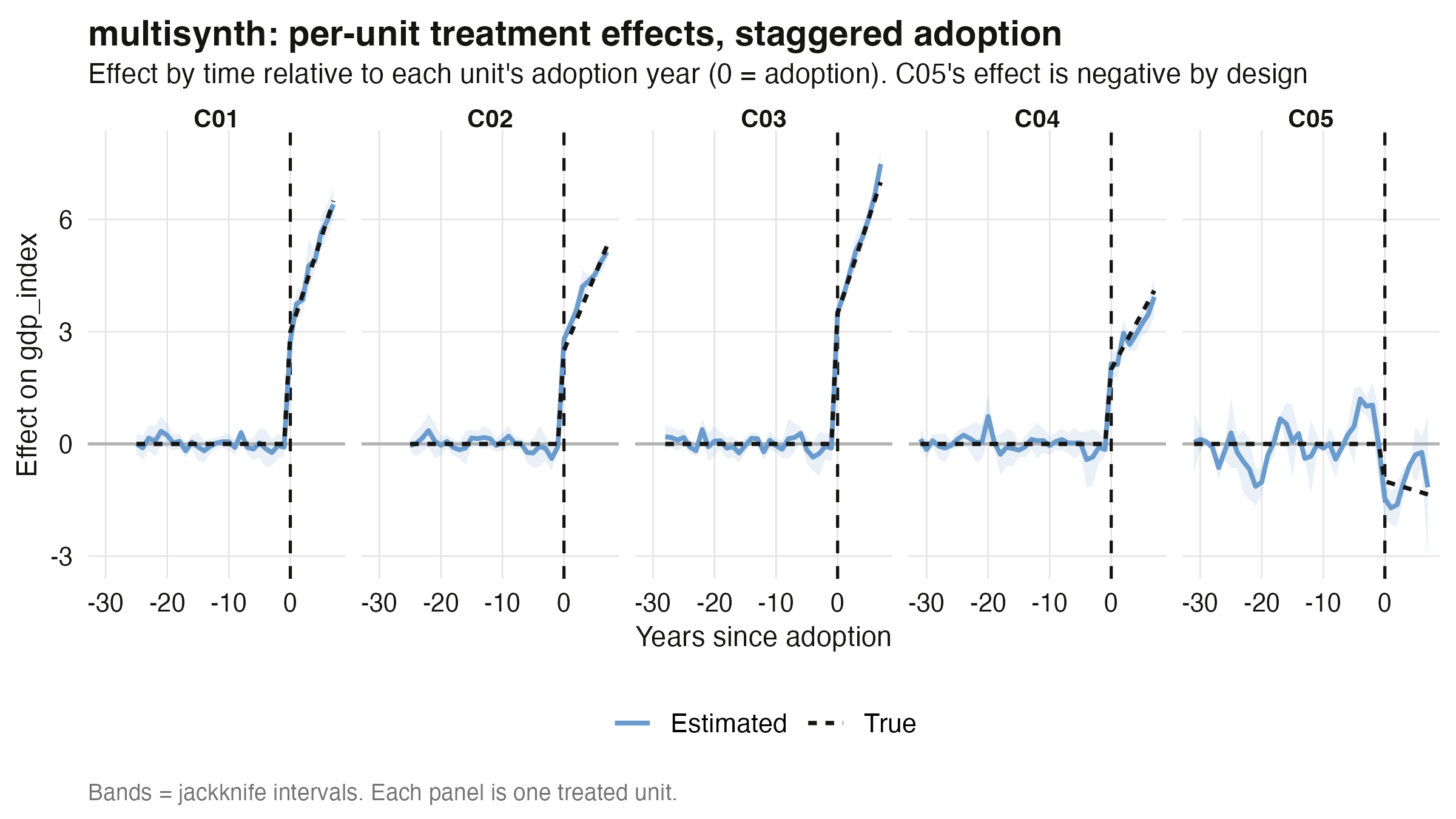

multisynth recovers the pooled ATT — and every per-unit sign, including a negative one

Per-unit treatment effects under staggered adoption: each unit’s estimate climbs to meet its dashed truth line — and C05 drops the opposite way.

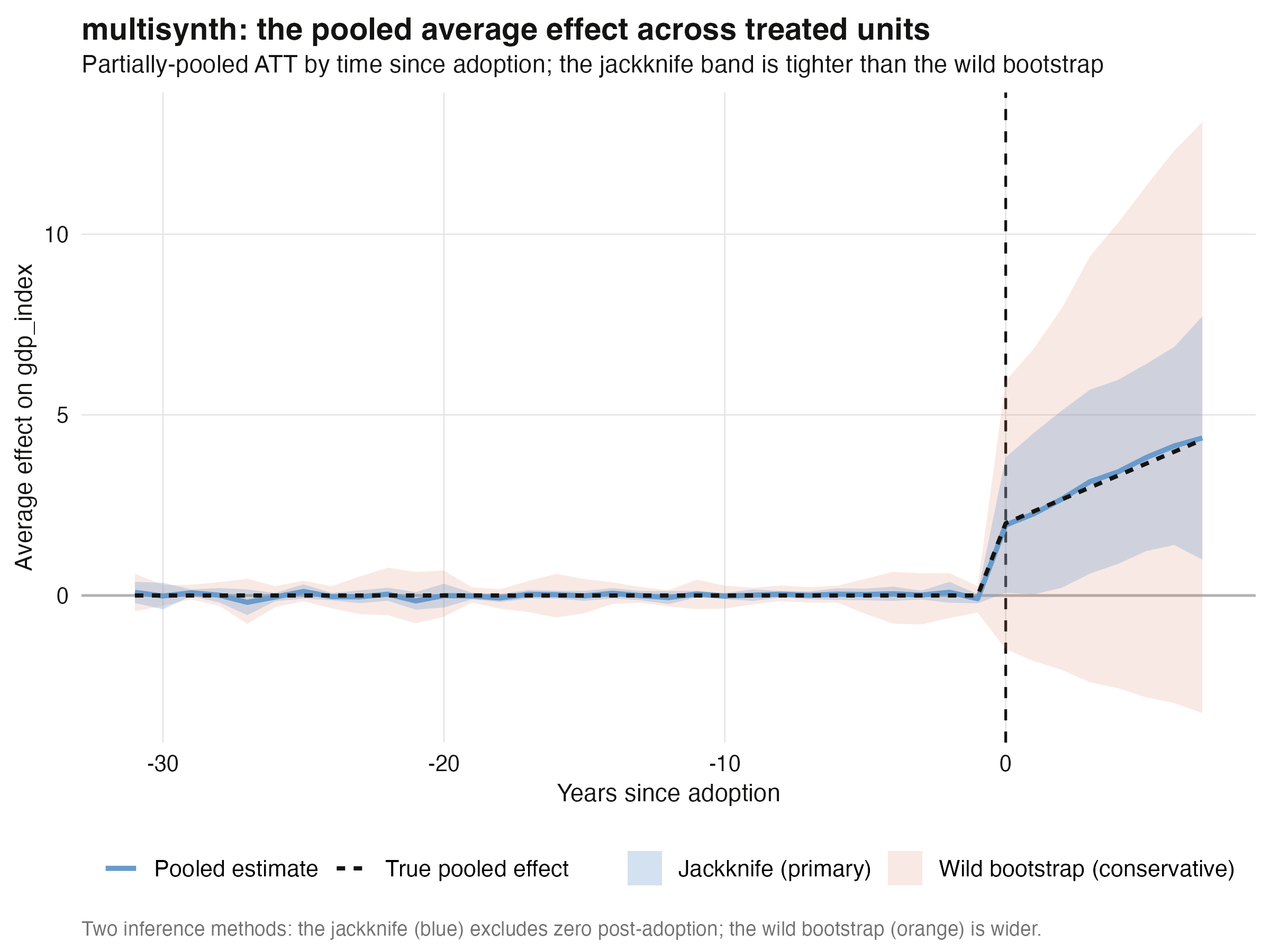

Same estimate, different verdict: jackknife says significant, the bootstrap says not

Pooled average effect with the tight jackknife band (excludes zero) and the wide wild-bootstrap band (includes zero), vs the true pooled effect.

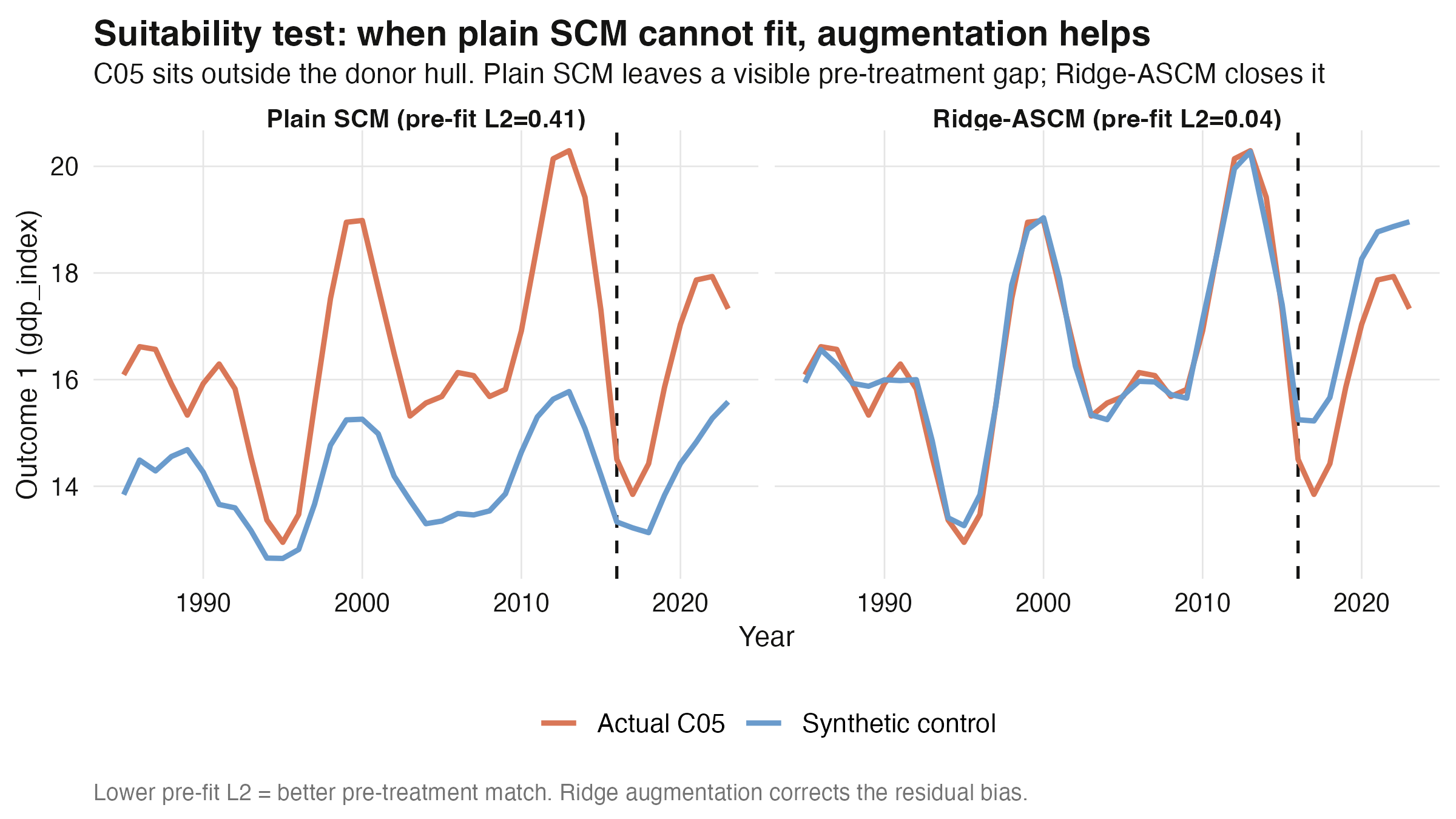

When a unit sits outside the donor hull, plain SCM gets the sign wrong

Suitability test for C05: plain SCM (blue) drifts from actual C05 (orange) before treatment; Ridge-ASCM pins them together pre-2016.

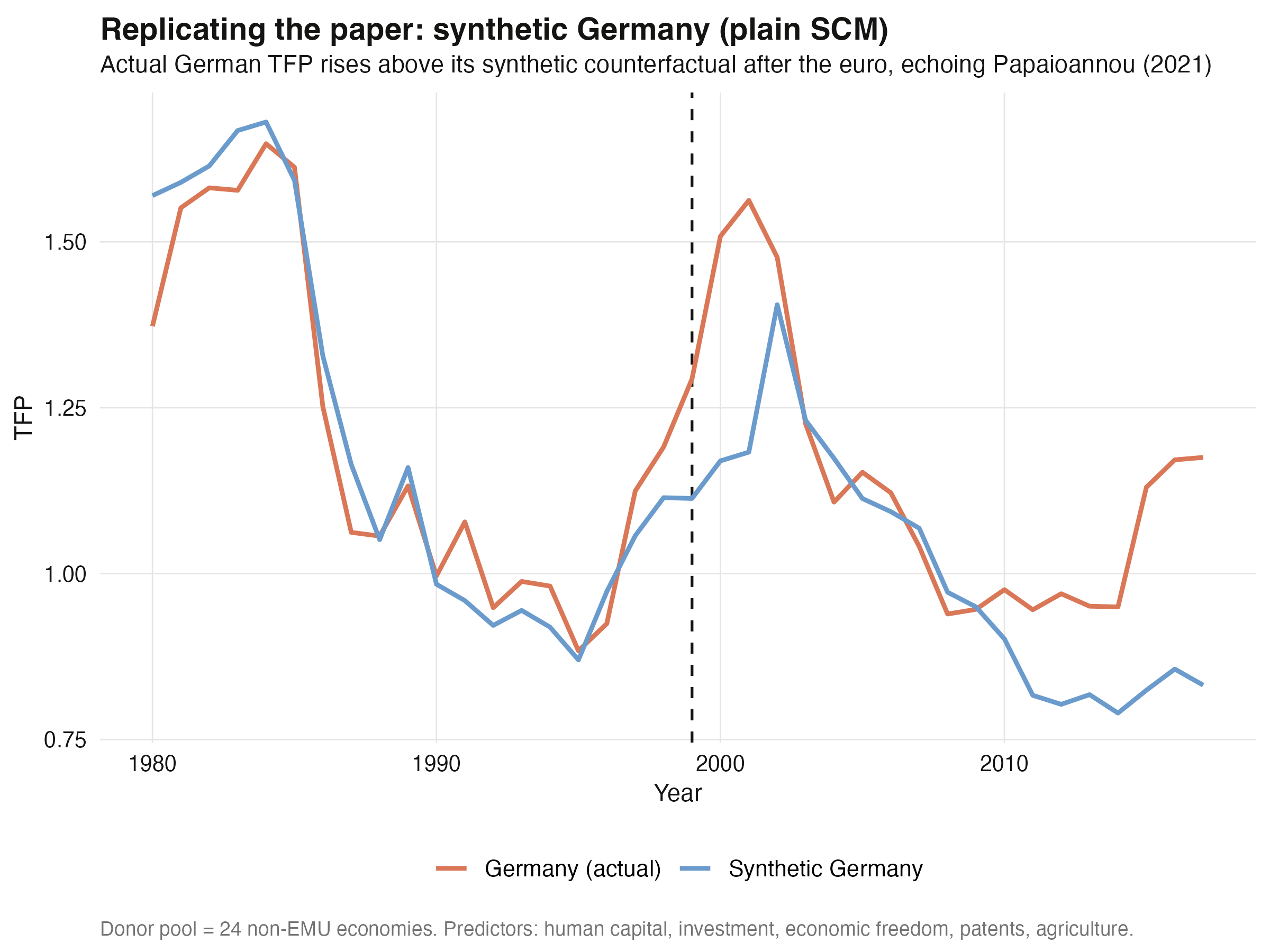

On real data, synthetic Germany’s TFP runs +0.133 above its counterfactual after 1999

Synthetic Germany under plain SCM: actual TFP (orange) rises above the synthetic counterfactual (blue) after the 1999 euro launch.

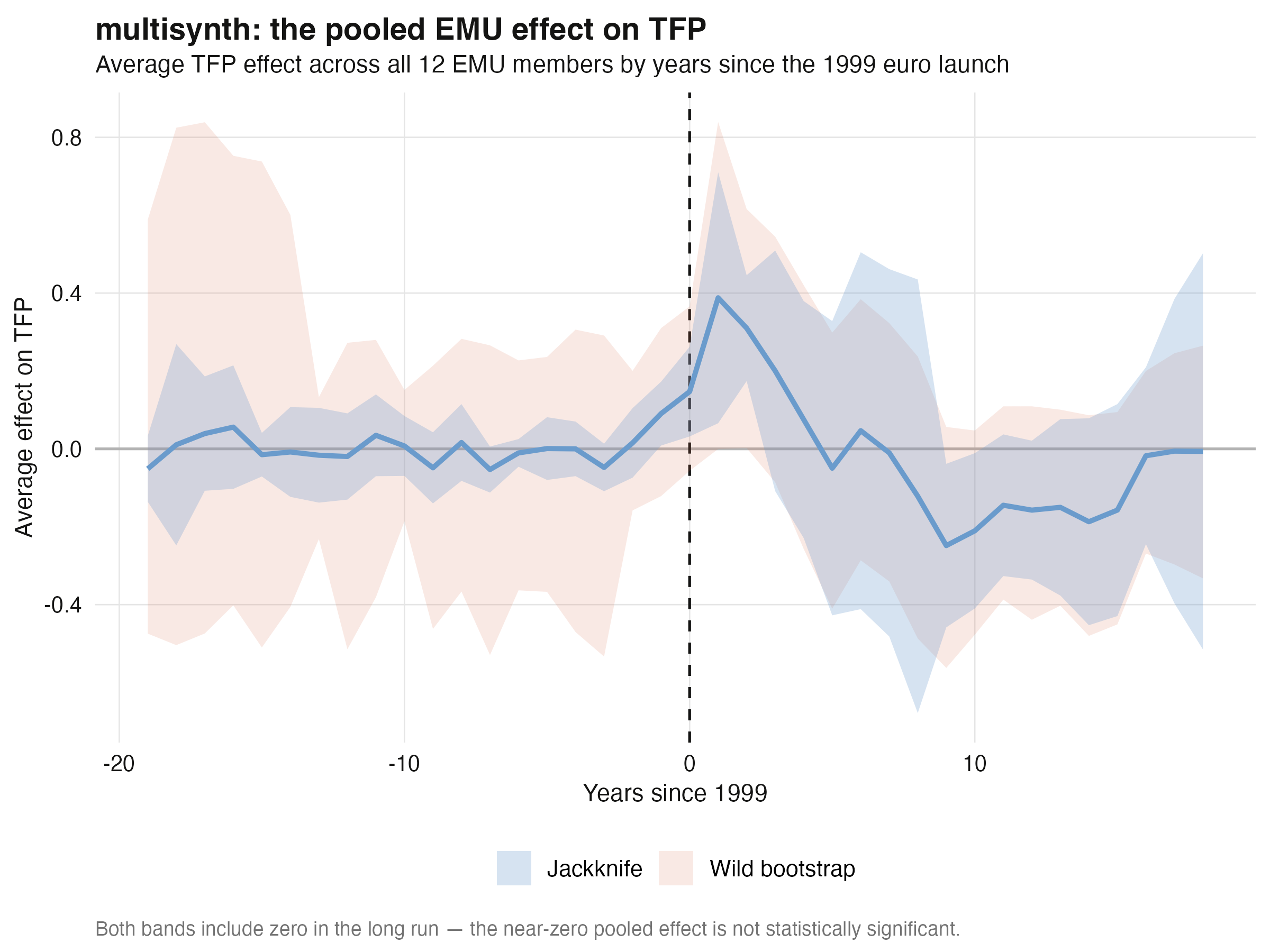

The pooled euro average is a forgettable −0.016 — but the path tells the story

Pooled euro-area effect on TFP: flat pre-1999, a +0.39 early bump, eroded into negative territory by the 2008–2014 crisis, recovering by 2017.

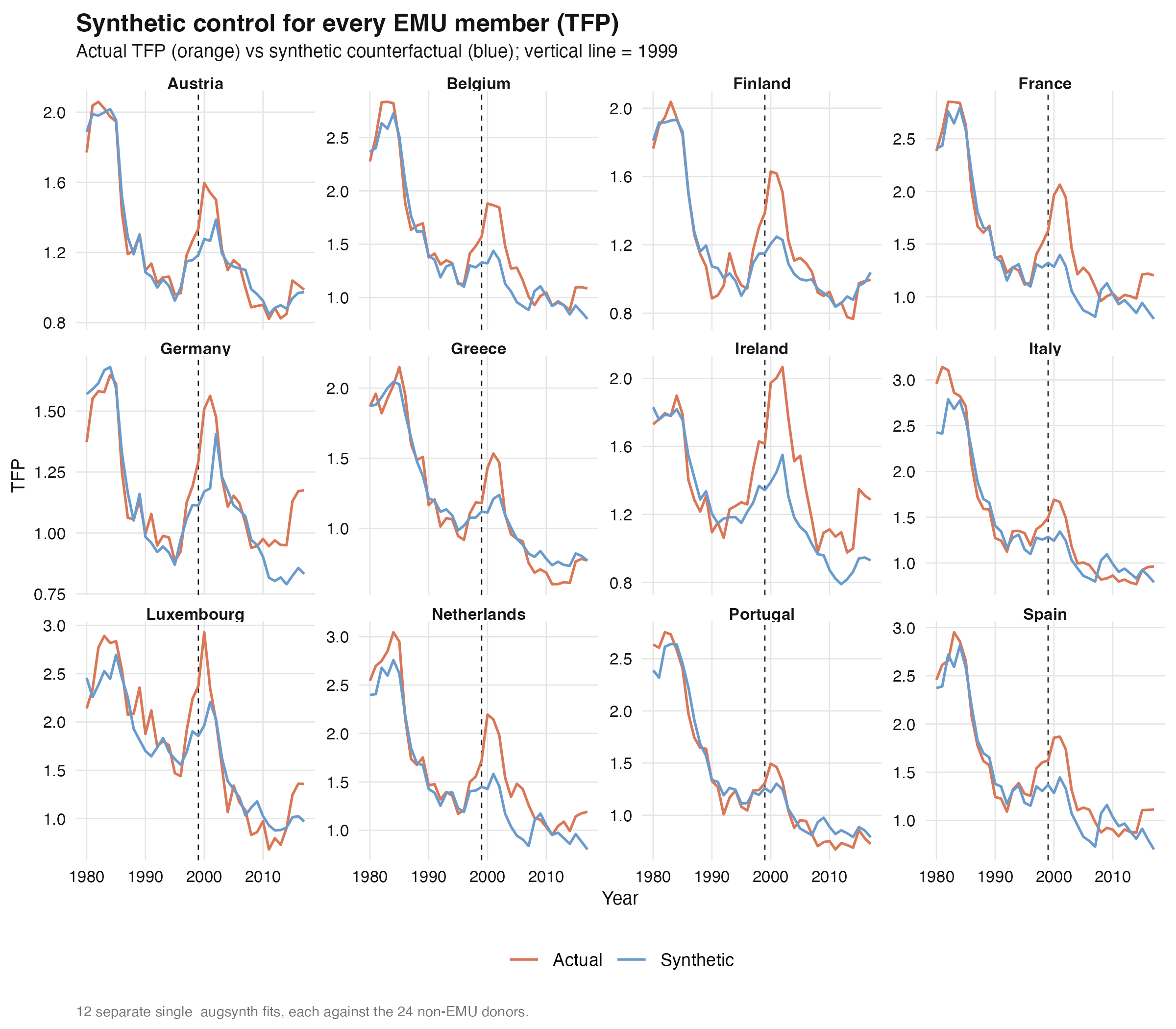

Per-member fits reveal the heterogeneity the average hides

Synthetic control for every euro member: most run above their synthetic counterfactual after 1999; Greece and Portugal fall below post-crisis.

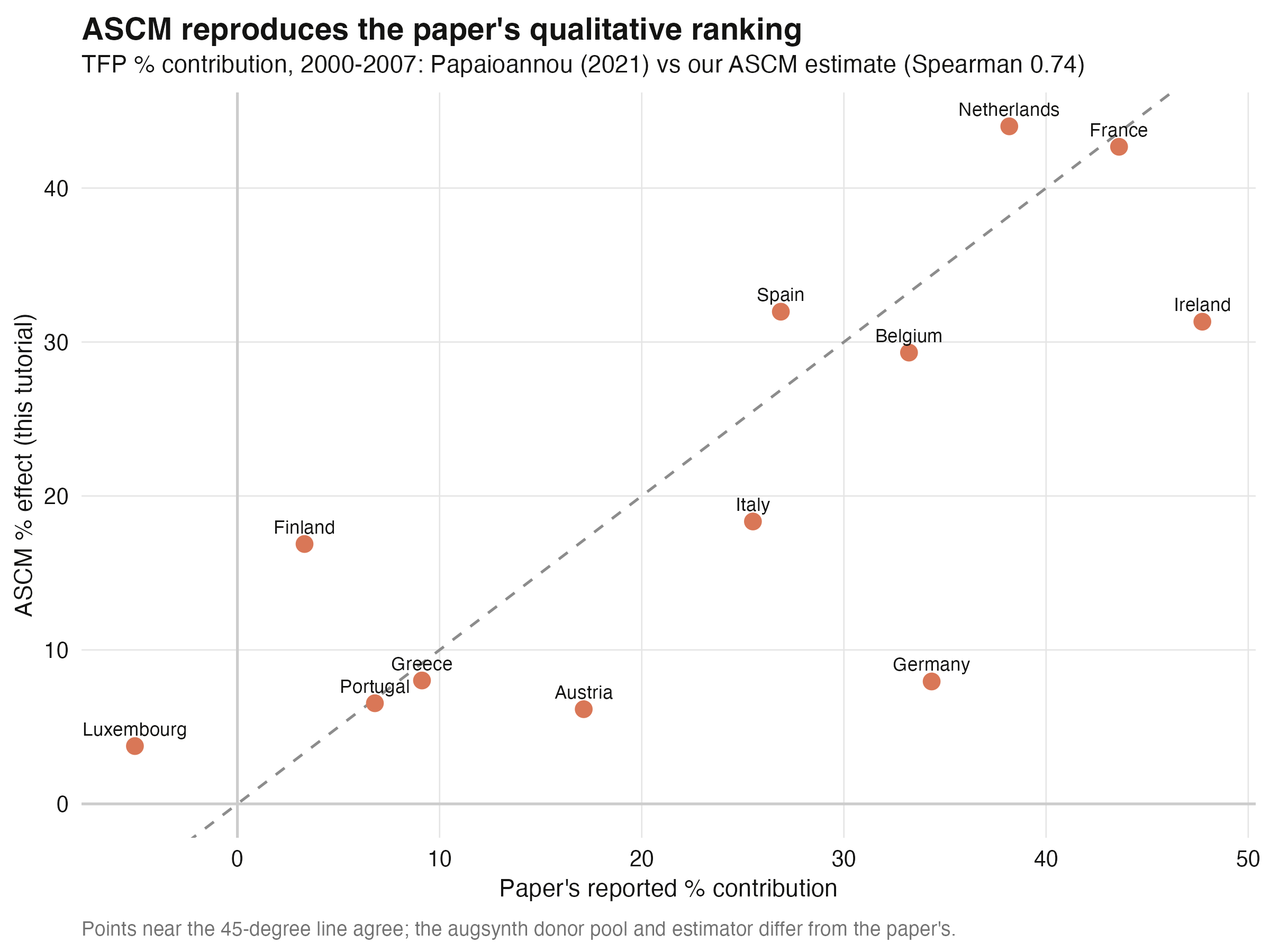

The numbers line up around the 45-degree line, not on top of it

ASCM vs Papaioannou (2021): per-member TFP % contributions cluster around the 45-degree line, Spearman 0.74.

We do not reproduce the paper’s numbers exactly — and should not. Same signs, same ranking, same dynamic story is the right bar.