The average effect among households whose covariates equal\(\mathbf{x}\). Where \(\tau(\mathbf{x})\) bends with \(\mathbf{x}\), the program helps some households more than others.

The single ATE is just \(E[\tau(\mathbf{X})]\) — the CATE averaged over the population.

Two assumptions do the causal work — the forest only fits the function

Unconfoundedness

\[y(1),y(0) \perp d \mid \mathbf{x}\]

No unmeasured confounders given the covariates

Justified here by a rich demographic vector

Overlap

\[0 < \Pr(d=1\mid \mathbf{x}) < 1\]

Every profile could be treated or not

37% / 63% split → comfortable overlap

Machine learning chooses controls flexibly; it cannot manufacture identification.

The lab: 9,913 households, eligibility → net financial assets

Outcome — net total financial assets ($), wildly right-skewed: mean $18,054, median just $1,499

assets3, the canonical Chernozhukov–Hansen excerpt shipped with Stata 19.

cate runs cross-fit lasso and a causal forest in one command

webuse assets3, clear* covariates driving the heterogeneity = nuisance controls hereglobal catecovars age educ i.incomecat i.pension i.married i.twoearn i.ira i.ownhomecate po (asset $catecovars) (e401k), rseed(12345671)

Lasso for the nuisance functions (cross-fitted), a generalized random forest for \(\tau(\mathbf{x})\), honest-tree bootstrap for the CIs — Stata 18 needed hand-rolled loops.

Two routes to the same object: PO is robust, AIPW is efficient

PO (partial-linear)

Residualize \(y\) and \(d\) on \(\mathbf{x}\), then regress

Transparent; robust when propensities near 0 or 1

ATE \(= \$7{,}937\)

AIPW (interactive)

Separate outcome models + propensity reweight

Doubly robust: only one nuisance model need be right

ATE \(= \$8{,}120\)

Both return a per-household effect function \(\hat\tau(\mathbf{x}_i)\) — they differ only in how they map nuisances into it.

Three estimators bracket the ATE within a $183 spread

$8,000

Parametric AIPW $8,019 · ML PO $7,937 · ML AIPW $8,120 — agreement across very different specifications

First, does the effect vary at all? The test says yes

Estimator

\(\chi^2(1)\)

\(p\)

Verdict

cate po

4.11

0.043

reject homogeneity

cate aipw

5.54

0.019

reject homogeneity

estat heterogeneity — \(H_0:\ \tau(\mathbf{x})\) is constant. Both reject at 5%, so the heterogeneity hunt is not chasing noise.

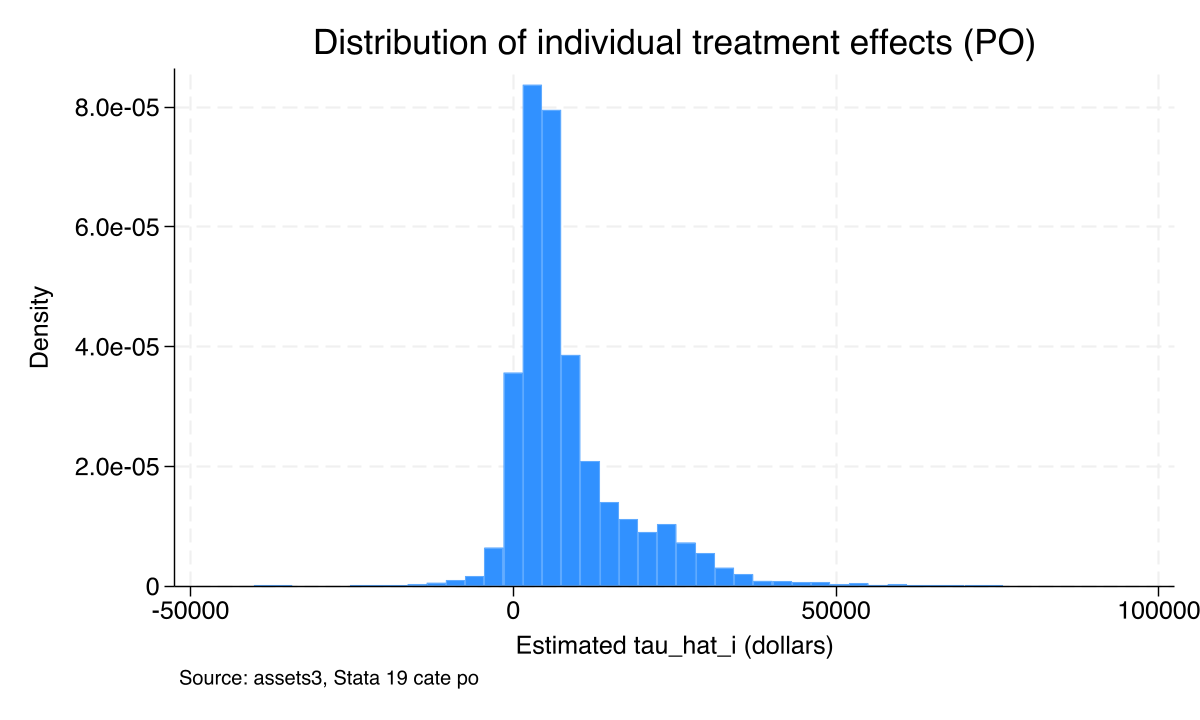

The average of $7,937 hides a long right tail of large effects

PO-estimated individual effects \(\hat\tau_i\) across 9,913 households: a tight mode near $5–10k, a tail past $80k, and a small mass near or below zero.

A linear projection of \(\hat\tau_i\) says income is the only strong signal

Covariate

Effect on \(\hat\tau_i\) ($)

\(p\)

Highest income category

+18,195

0.001

Homeowner

+3,163

0.058

Age (per year)

+205

0.082

Education (per year)

−442

0.365

estat projection: the only coefficient significant at 1% is the top income category. \(R^2=0.0045\) — most heterogeneity is nonlinear, captured by the forest, not the projection.

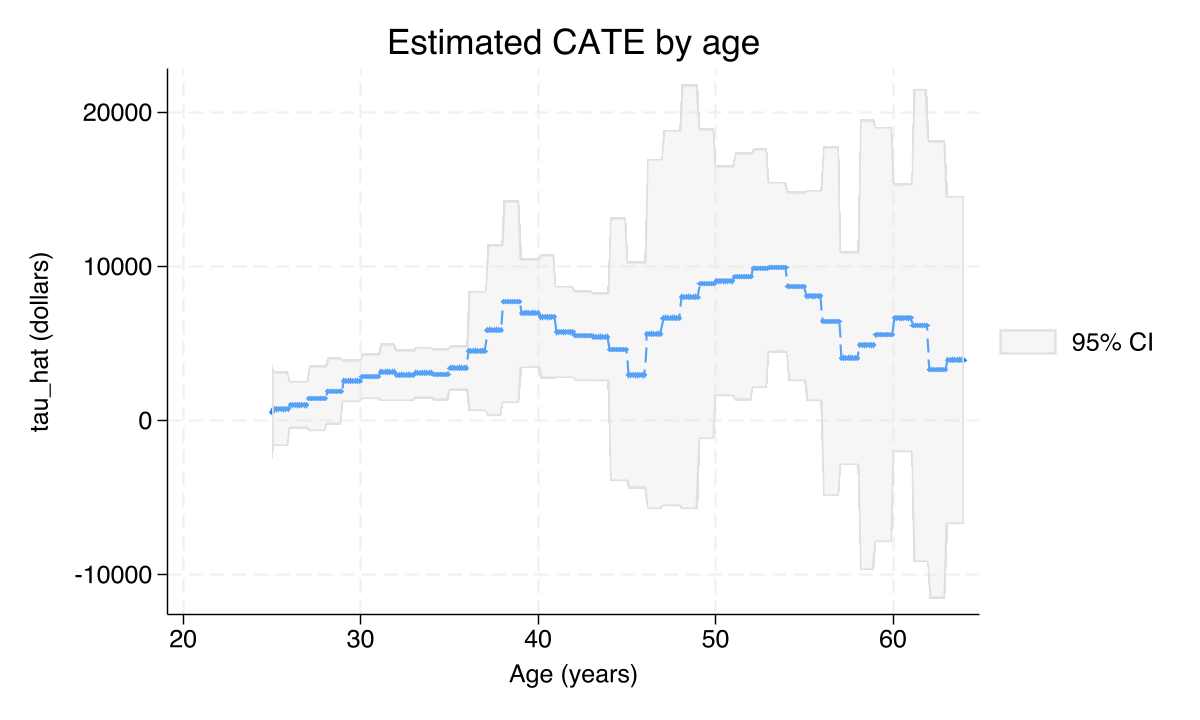

Effects climb with age; education barely moves them

PO-estimated CATE by age (others fixed at means): slightly negative in the mid-20s, clearly positive by 35–40, still rising through the 50s.

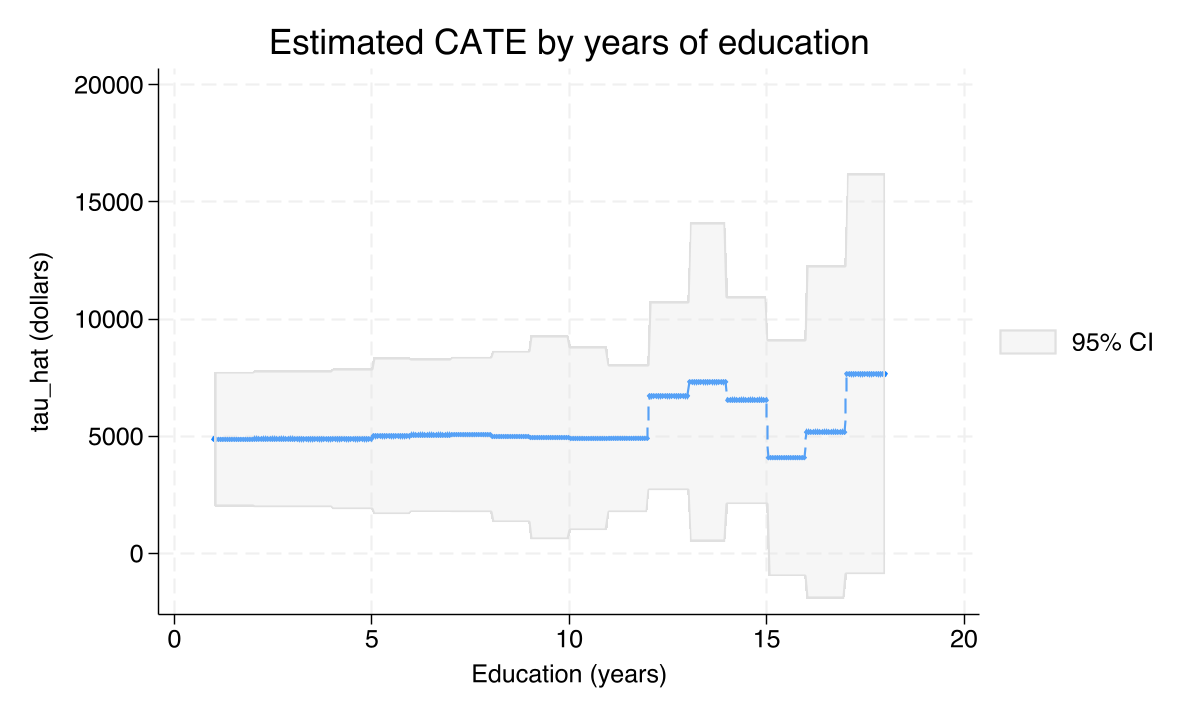

Education is a flat line — once you know income, it adds nothing

PO-estimated CATE by years of education: broadly flat around $1–3k from 8 to 18 years of schooling.

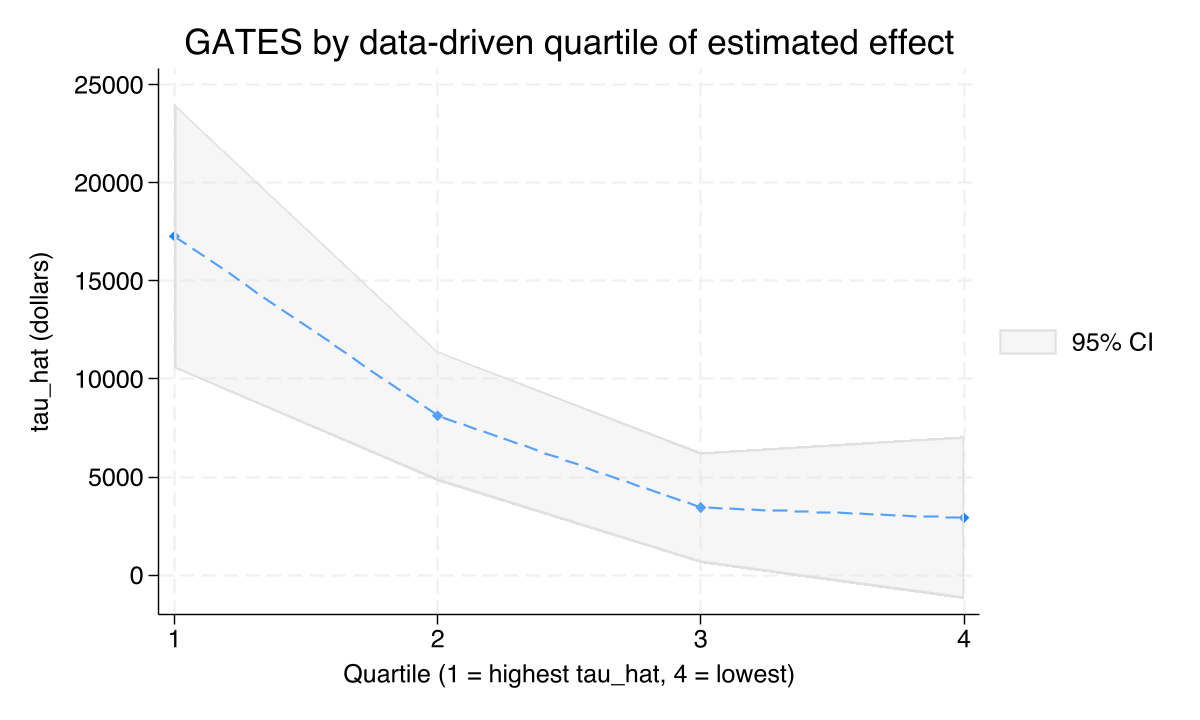

Let the data sort the households: the top quartile gains 5.9× the bottom

GATES by data-driven quartile of predicted effect: $17,279 → $8,121 → $3,444 → $2,919. A clean monotonic ladder; the bottom bin is not distinguishable from zero.

The high-effect quartile earns $35,878 more than the low-effect one

Covariate

Top quartile

Bottom quartile

Diff

\(t\)

Income ($)

62,739

26,861

35,878

56.2

Age (years)

45.2

35.0

10.2

35.7

Education (years)

14.0

12.7

1.4

18.6

estat classification: the data sorted itself; income is the dominant marker of who responds. All three gaps have \(t>18\).

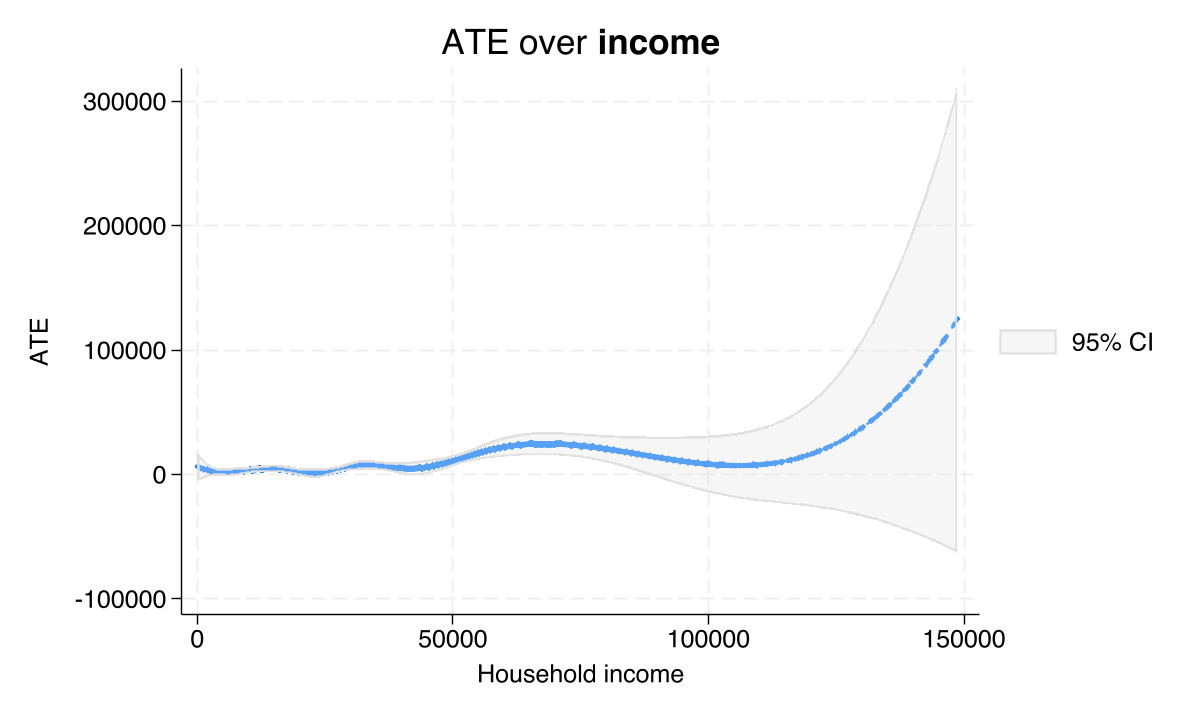

A smooth fit: each extra $1,000 of income adds ~$213 to the effect

Cubic B-spline of \(\hat\tau\) vs household income (income \(\le\) $150k): a smooth upward slope, steepest in the middle of the distribution.

The Resolution

Act III

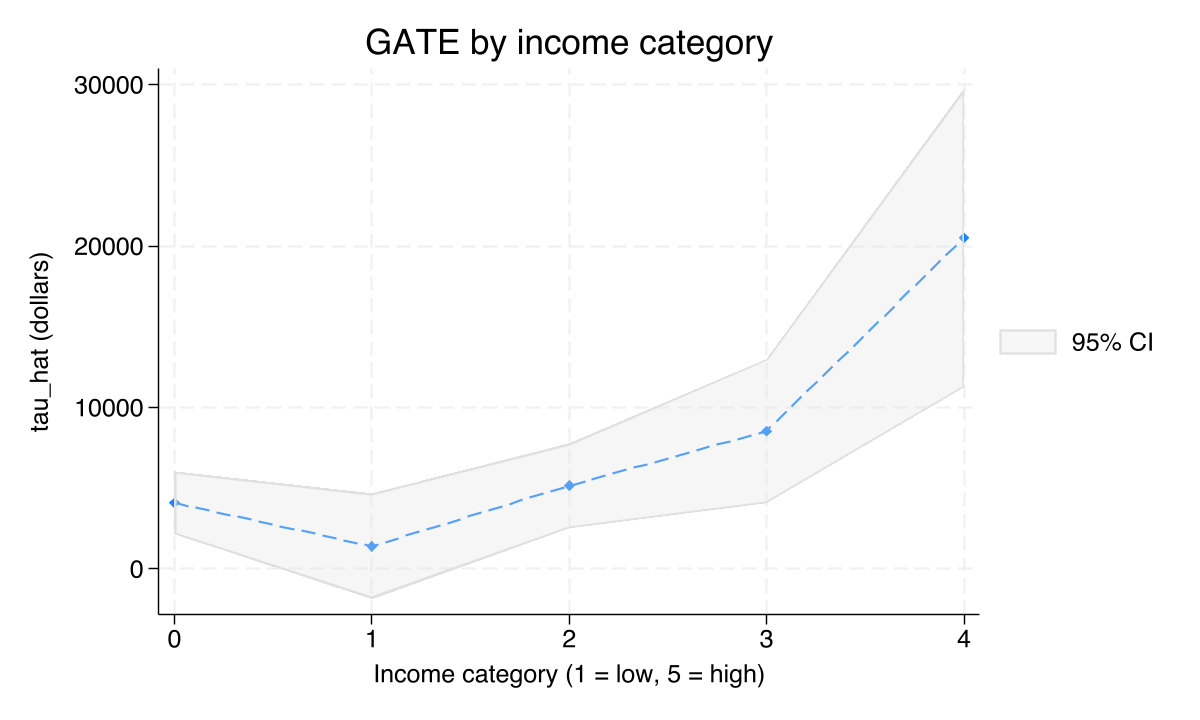

The top income group gains $20,511 — five times the average household

$20,511

GATE, highest income category (vs ~$4,000 at the bottom). Joint test of equality across groups: \(\chi^2(4)=18.44\), \(p=0.001\)

A quarter of households gain little or nothing — invisible in the ATE

The bottom GATES quartile is $2,919 with \(p=0.167\) — not statistically distinguishable from zero.

Combined with the small negative left tail of the histogram: roughly one in four households appears to gain close to nothing from eligibility.

Does the causal forest make this causal? No — the assumptions still carry it

Objection. A machine that flexibly selects controls surely earns us the causal interpretation.

Response. It does not. \(\tau(\mathbf{x})\) is identified only under unconfoundedness and overlap. The forest fits the function; it cannot rule out an unmeasured confounder.

The average is a press release; the CATE is the policy

ATE \(\approx \$8{,}000\) — agreed across three estimators within $183

But effects span $1,400 → $20,511 across income groups (\(p=0.001\))

Income is the moderator: +$213 per $1,000, +$18,195 at the top

One in four households gains essentially nothing

Estimate the CATE, not just the ATE — the average is hiding who your policy actually helps.